India's Hidden Industrial Compounder: 24% Profit Growth Ignored

Investment Thesis & Summary

Here’s the thing - this stock’s trading at a fair price for what’s essentially a monopolistic player in India’s steel refractory space. The parent company in the UK owns 55.57%, so you’re getting a piece of global technology with Indian manufacturing costs. The real kicker? They’ve grown profits at 24% annually for five years while the stock’s barely moved in the last year. That gap won’t last.

Business Model & Operations

This company makes the specialized ceramic and refractory products that line steel furnaces and control molten metal flow. Think of them as the plumbers for steel mills - except their “pipes” handle 1600°C molten metal. They sell three main things: flow control systems (stoppers, nozzles, shrouds), refractory linings for furnaces, and monitoring equipment. Their customers? Tata Steel, JSW, SAIL - basically every major steel producer in India.

They’ve got four manufacturing plants across India - two in Visakhapatnam, one each in Kolkata and Mehsana. In 2024, they opened a new Basic Monolithic plant in Visakhapatnam and commissioned India’s first robotic tube change system at Tata Steel Kalinganagar. That’s not just expansion - it’s automation that cuts costs and makes them stickier with customers.

The business model is simple: steel companies can’t produce without refractories, and switching suppliers is risky because any failure means shutting down a ₹1,000 crore furnace. Once you’re in, you stay in. They’re making money from consumables (products that wear out every few months) plus long-term service contracts. Recurring revenue is the name of the game here.

Historical Financial Review

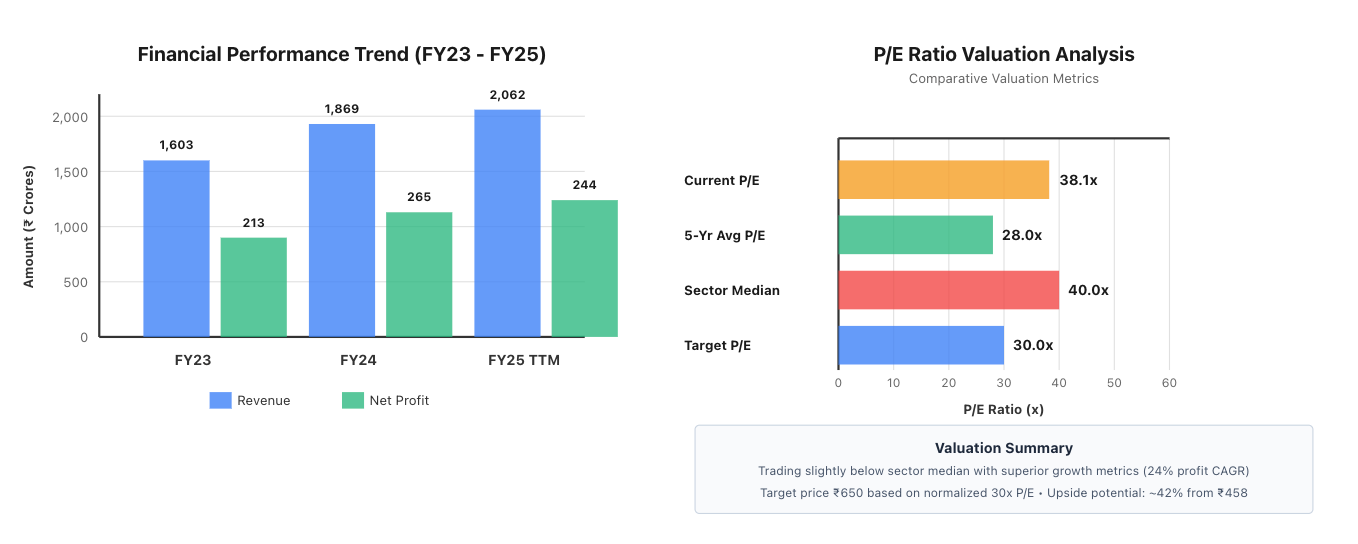

Revenue’s grown at 21% over the last three years, jumping from ₹1,343 crores in FY22 to ₹2,062 crores in the trailing twelve months. That’s solid growth for an industrial company. Net profit grew even faster - from ₹117 crores to ₹244 crores, a 55% CAGR over three years. The last twelve months saw earnings per share of ₹12.00, which is up from ₹5.75 just two years ago.

Here’s what’s actually happening: India’s steel production keeps growing, and this company’s got pricing power. Their operating margins expanded from 12% in 2022 to 17% now. That’s not inflation - that’s better product mix (they’re selling more high-value flow control products versus commodity refractories).

Cash flow tells the real story. In FY24, they generated ₹258 crores in operating cash flow - that’s clean, real money. They spent ₹233 crores on expansion (new plants in Visakhapatnam, solar installations, automation equipment). They’re debt-free except for ₹13 crores in lease obligations. The balance sheet’s pristine - ₹1,411 crores in reserves against ₹20 crores in equity.

The company paid out ₹14.50 per share as dividend in FY24 (that’s ₹145 pre-split, they did a 1:10 split in 2025). They’re returning cash to shareholders while still investing heavily. That’s confidence.

Fundamental Valuation Metrics & Investment Call

P/E Ratio: 38.1x - Yeah, it looks expensive at first glance. Their 5-year average P/E is around 28x, and sector median is closer to 40x. But here’s the context: they’ve consistently grown earnings at 24% annually. At that growth rate, you’re paying roughly 1.6x PEG ratio, which is reasonable for a quality industrial.

P/B Ratio: 6.5x - They’re trading at 6.5 times book value of ₹75 per share. For a capital-light business with 19% ROE, that’s justified. They don’t need massive fixed assets - most value is in patents, customer relationships, and technical know-how.

ROE: 19.3% and ROCE: 25.5% - These are excellent numbers. They’re earning ₹19.30 for every ₹100 of shareholder money, and ₹25.50 on total capital employed. Compare that to most industrials doing 12-15%. This screams competitive moat.

EPS Growth: From ₹5.75 (FY22) to ₹12.00 (TTM) in just over two years. That’s the kind of trajectory you want to see.

Dividend Yield: 0.32% - Low, yes. But that’s because they’re reinvesting aggressively. The payout ratio is only 11%, meaning they’re keeping 89% of profits for growth. Smart move at this stage.

The Call: At ₹458, you’re paying for quality but not overpaying. Fair value sits around ₹550-600 based on normalized 30x P/E on FY26 estimated earnings of ₹18-20. Target of ₹650 assumes they maintain current growth rates and the market gives them sector-average multiples. That’s 42% upside in 18-24 months.

Long-Term Outlook & Risk Assessment

5-15 Year Return Estimate: 18-22% CAGR

Here’s the math: India’s steel production should grow 7-8% annually through 2030. This company’s growing revenue at 2-3x that rate by taking market share and upselling premium products. If they maintain even 15-18% profit growth (half their current pace), and multiples stay flat, you’re looking at 15-18% stock returns. Add 2-4% from expanding valuations as the market recognizes quality, and you’re at 18-22% total.

Growth Drivers:

The parent company’s investing ₹400+ crores in new capacity through 2026. They’re expanding aluminum refractories (currently 10% of revenue, targeting 20%). The Visakhapatnam plants will hit full utilization by late 2026, adding ₹300-400 crores to annual revenue. They’re also increasing export intensity - currently around 15% of sales, targeting 25% as European steel mills seek low-cost suppliers.

Management’s spending smart. They put ₹150 crores into automation and digitization in FY24. Solar capacity now covers 19% of energy needs - that’s margin protection when power costs spike. The robotic systems at Tata Steel aren’t just cool tech; they lock in those contracts for 10+ years.

Capital Allocation:

Promoters hold steady at 55.57% - no selling. DIIs own 21%, FIIs are at 4.4% and rising (up from 1.5% a year ago). That foreign money sniffing around is a good sign. The company’s paying 11% of profits as dividends while reinvesting the rest. If growth slows in 3-5 years, expect dividend payout to jump to 30-40%.

Risks - Let’s Be Real:

Steel sector cyclicality - If India’s steel demand tanks, this company takes the hit. Steel production dropped in Q2 FY25, and their revenue growth slowed to 16% from 22%. That’s your canary in the coal mine.

Customer concentration - Top 5 customers probably account for 50%+ of revenue. Lose one big contract to a competitor, and earnings take a 10-15% hit.

Raw material costs - They buy alumina, magnesia, graphite. These commodities can spike 20-30% in a year. They pass costs through eventually, but there’s a 2-3 quarter lag that squeezes margins.

Import competition - Chinese refractories are 20-30% cheaper. If steel mills get desperate on costs, they’ll switch. The company’s defense is technical support and reliability, but price always matters.

Regulatory risk - Indian government keeps tweaking steel import duties and production-linked incentives. Any policy that hurts domestic steel production hits this company.

What’s Going Right:

India’s pushing 300 million tonnes of steel capacity by 2030 (from 140 million now). That requires ₹15,000-20,000 crores in refractory investments over the next 5-7 years. This company’s positioned to capture 35-40% of that. The PLI scheme for specialty steel means more high-value production, which needs better (read: more expensive) refractories. Green steel initiatives require new refractory technology - another margin opportunity.

The bottom line: You’re buying the #1 player in a growing market at a reasonable price. Growth is real, balance sheet is bulletproof, and management knows what they’re doing. The risks are manageable if you’re patient through steel cycles. If you’re looking for a boring industrial that compounds at 18-20% for a decade, this fits the bill.

Disclaimer:

This content is for educational purposes only and is not investment or financial advice. Stock markets are subject to risks. Do your own research and consult a qualified advisor before investing. The author is not responsible for any financial losses. Mentions of stocks/companies are not buy or sell recommendations.

To read ValuePicks Studies Take on this : Upgrade to paid membership