IndiaMART's Strategic Inflection: Decoding the Marketplace Evolution

IndiaMART InterMESH Ltd presents a fascinating case study of market leadership under siege. While superficial metrics showcase robust profitability and commanding market presence, a deeper examination of regulatory filings and operational data unveils a company navigating fundamental structural shifts in India's B2B commerce landscape.

The company's Q3 FY25 performance demonstrates this complexity perfectly. Strong headline numbers—48% profit growth and ₹2,606 crores cash reserves—coexist with concerning operational signals that suggest the traditional marketplace model faces unprecedented pressure. The emergence of paying subscriber churn, particularly in cost-sensitive segments, indicates that IndiaMART's dominance may be more fragile than market perception suggests.

This analysis synthesizes regulatory disclosures, competitive intelligence, and industry dynamics to reveal why IndiaMART's transformation from pure marketplace to comprehensive SME ecosystem represents both strategic necessity and significant execution risk.

Revenue Model Transformation Signals Structural Pressures

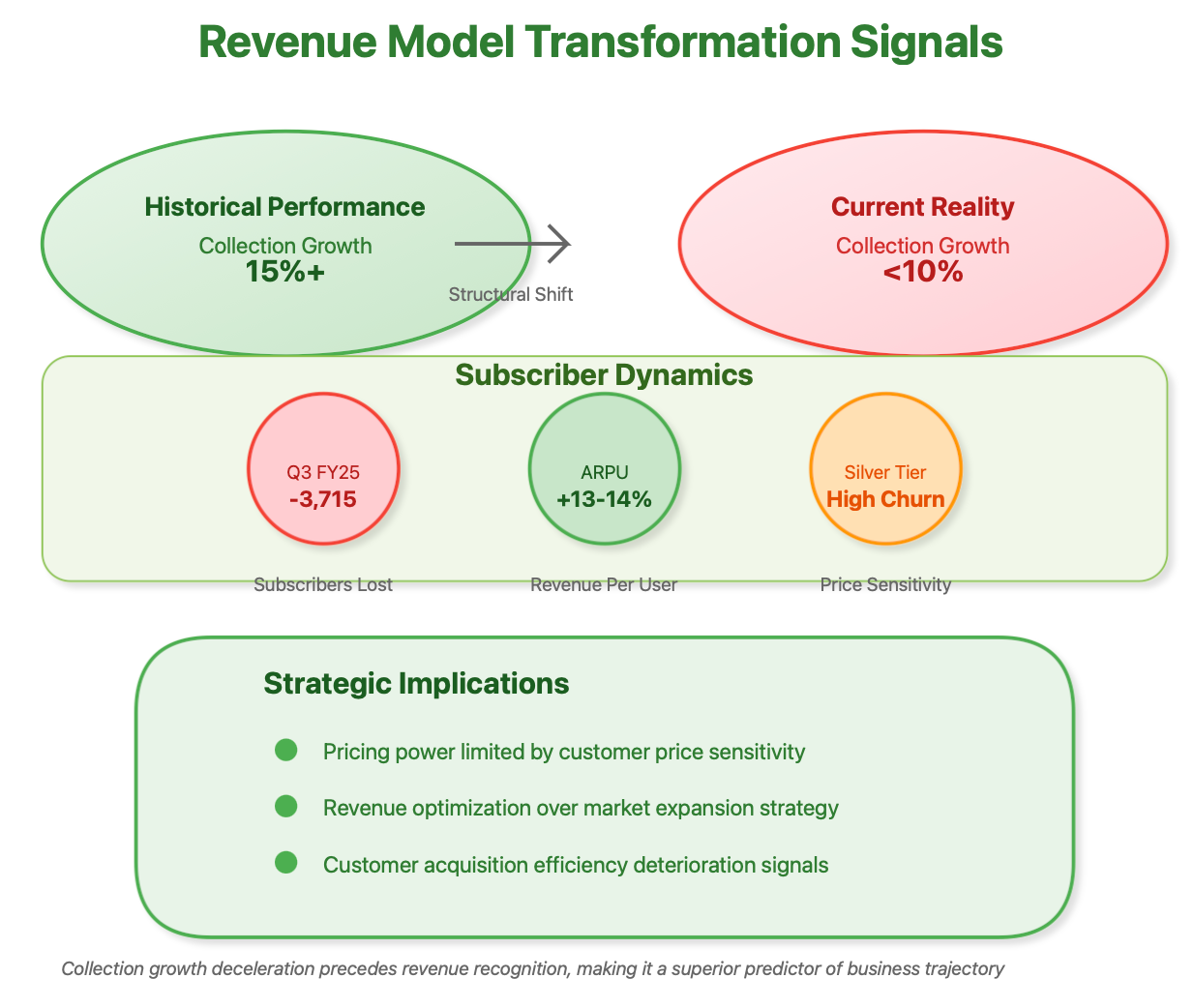

The most revealing indicator of IndiaMART's strategic position emerges from collection growth patterns rather than reported revenues. Collection metrics, representing actual cash inflows from subscribers, have contracted from historical 15%+ growth rates to projected single-digit expansion in FY25. This deceleration precedes revenue recognition by quarters, making it a superior predictor of business trajectory.

SEBI filings document the first quarterly subscriber decline since COVID-19 disruption—3,715 paying suppliers exited the platform in Q3 FY25. Management frames this as "quality optimization," but granular analysis reveals disproportionate churn in the Silver subscription tier, exposing price elasticity concerns among smaller businesses that form IndiaMART's customer base foundation.

The ARPU improvement of 13-14% appears impressive until contextualized against subscriber loss patterns. Rather than reflecting genuine pricing power, these increases suggest a strategic trade-off where IndiaMART prioritizes revenue per customer over customer base expansion. This approach may optimize short-term profitability but potentially constrains long-term market penetration in a rapidly digitalizing economy.

Cross-referencing customer acquisition costs with lifetime value metrics reveals another concerning trend. While IndiaMART doesn't disclose detailed customer economics, the combination of slowing collection growth and rising ARPU suggests customer acquisition efficiency has deteriorated, forcing the company to extract more value from existing relationships rather than expanding its addressable market.

Competitive Landscape Restructuring Accelerates

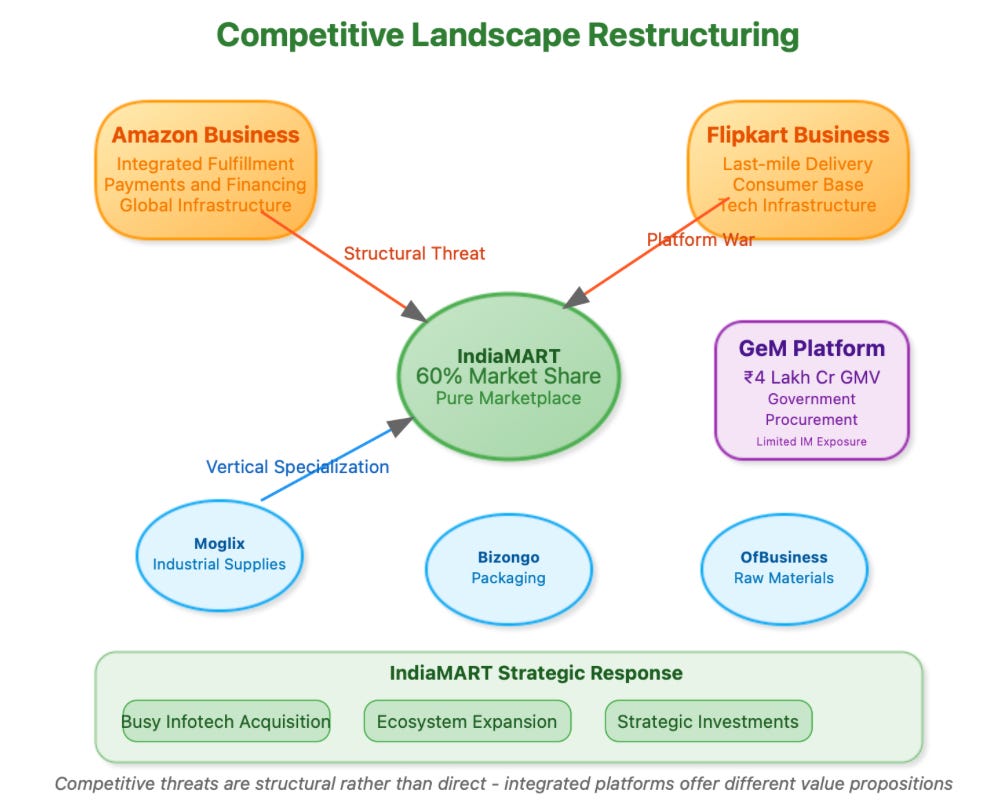

IndiaMART's market position faces challenges from multiple vectors that traditional competitive analysis underestimates. Amazon Business and Flipkart Business represent structural threats rather than direct competitors—their integrated fulfillment, payments, and financing capabilities create entirely different value propositions that pure marketplace models cannot replicate.

The emergence of specialized vertical players compounds this challenge. Companies like Moglix in industrial supplies, Bizongo in packaging, and OfBusiness in raw materials demonstrate that deep industry expertise can successfully challenge horizontal platforms. These specialized competitors offer industry-specific workflows, credit solutions, and supply chain integration that generalist platforms struggle to match.

Government e-Marketplace (GeM) achieving ₹4 lakh crore GMV in FY24 illustrates the scale of opportunity IndiaMART has partially missed. The company's limited government procurement exposure, while reducing regulatory complexity, also means foregoing the fastest-growing B2B segment where digital adoption is mandatory rather than discretionary.

The competitive response has been acquisition-heavy rather than organic innovation. IndiaMART's investments in Busy Infotech, its portfolio through Tradezeal Online, and minority stakes in B2B adjacencies suggest management recognizes the limitations of the core marketplace model. However, acquisition integration in technology platforms presents substantial execution risks that financial metrics don't capture.

Technology Investment Narrative Versus Operational Reality

IndiaMART's AI and machine learning initiatives receive significant management attention, with claims of processing 4 crore monthly business enquiries through advanced algorithms. However, technology spending as a percentage of revenue remains relatively constant, questioning whether these capabilities represent genuine competitive advantages or marketing positioning.

The platform's multilingual capabilities and intelligent cataloguing systems address real market needs in India's diverse business environment. Yet the disconnect between technological investment narratives and subscriber retention outcomes suggests either implementation challenges or misaligned innovation priorities. Technology investments that don't translate into customer stickiness represent sunk costs rather than competitive moats.

Conversational commerce generating 44.6 crore annual platform interactions creates valuable behavioral data, but this data advantage hasn't prevented subscriber churn in key segments. The failure to convert interaction volume into retention improvements indicates that IndiaMART's technology initiatives may not address the fundamental value propositions that drive customer loyalty.

The broader challenge lies in technology commoditization. As AI tools become more accessible, IndiaMART's current advantages in matching algorithms and search capabilities may erode unless continuously enhanced. The company's technology strategy requires constant innovation to maintain differentiation rather than one-time implementation.

Financial Fortress Provides Strategic Options

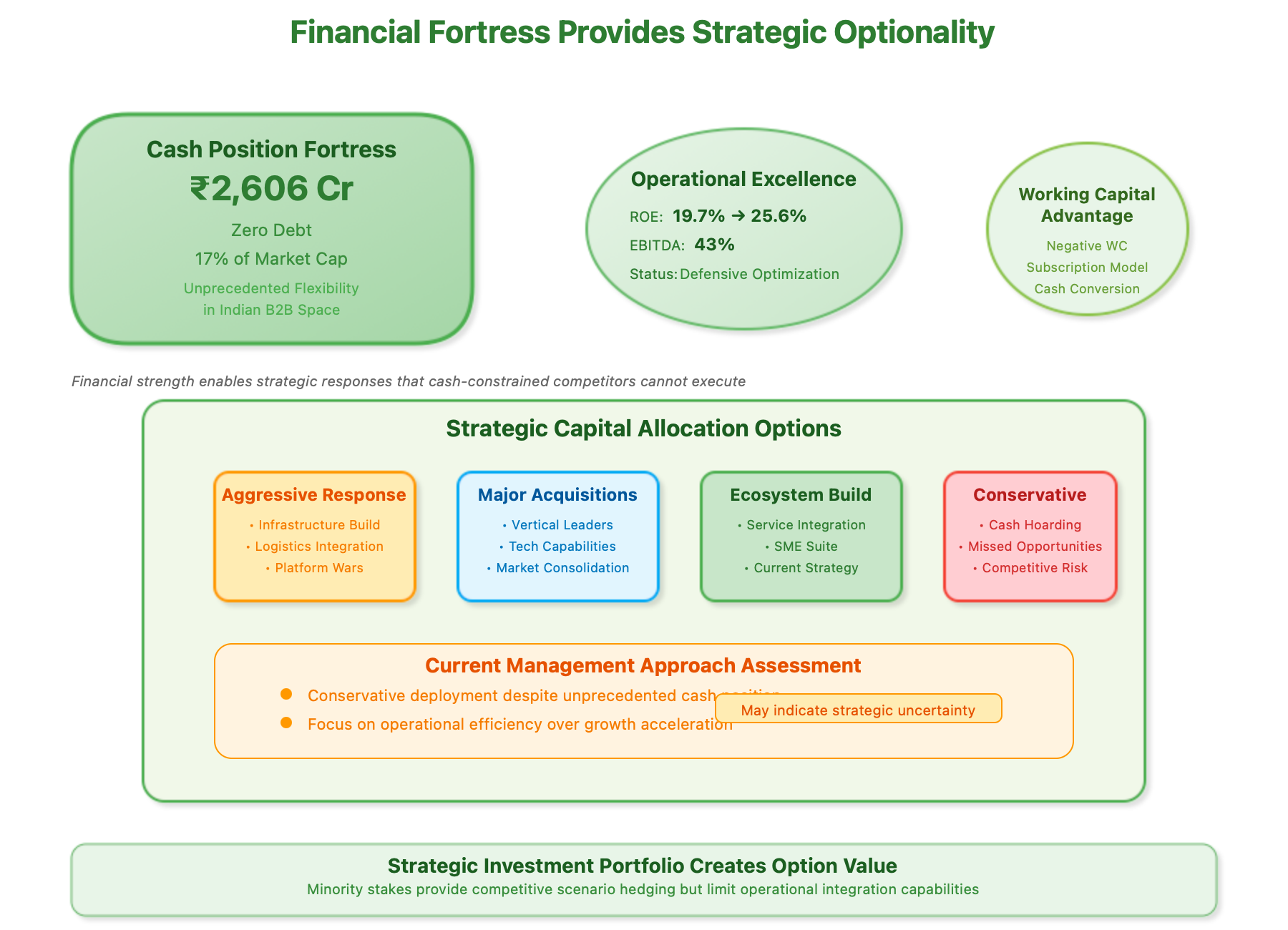

IndiaMART's balance sheet strength—zero debt and ₹2,606 crores cash—creates unprecedented strategic flexibility in the Indian B2B space. This financial position, representing 17% of market capitalization, enables aggressive competitive responses or transformative acquisitions that cash-constrained competitors cannot contemplate.

The operational metrics demonstrate exceptional profitability despite growth headwinds. Return on equity expansion from 19.7% to 25.6% and EBITDA margins reaching 43% showcase management's ability to optimize existing operations. However, these improvements partly reflect defensive cost management rather than growth-driven efficiency gains.

Working capital management deserves particular attention. IndiaMART's subscription model creates negative working capital characteristics as customers pay in advance for services delivered over time. This cash conversion advantage becomes more valuable during economic uncertainty when many businesses face liquidity constraints.

The investment portfolio through Tradezeal Online reveals strategic thinking about ecosystem expansion beyond organic capabilities. Stakes in Industry Buying, SuperProcure, and other B2B-focused companies create option value on various competitive scenarios. However, minority investments without operational control limit IndiaMART's ability to integrate these capabilities into coherent competitive responses.

Regulatory Environment Creates Opportunities and Constraints

India's regulatory framework for B2B e-commerce remains supportive with 100% FDI permitted and government digitization initiatives providing sector tailwinds. The Open Network for Digital Commerce (ONDC) represents both opportunity and threat—democratizing access to digital commerce while potentially commoditizing platform advantages.

GST and TDS digitization requirements benefit established platforms like IndiaMART by creating compliance barriers for informal competitors. However, these same regulations increase operational complexity and costs, particularly affecting smaller subscribers who generate the highest churn rates.

Data localization requirements and privacy regulations create competitive advantages for domestic platforms over international alternatives. IndiaMART's local presence and compliance infrastructure provide sustainable advantages that financial metrics don't fully capture.

The government's increasing focus on digital procurement through GeM creates a massive addressable market where IndiaMART's current exposure remains limited. Strategic positioning for government business could unlock significant growth vectors currently underutilized.

Ecosystem Transformation Strategy Assessment

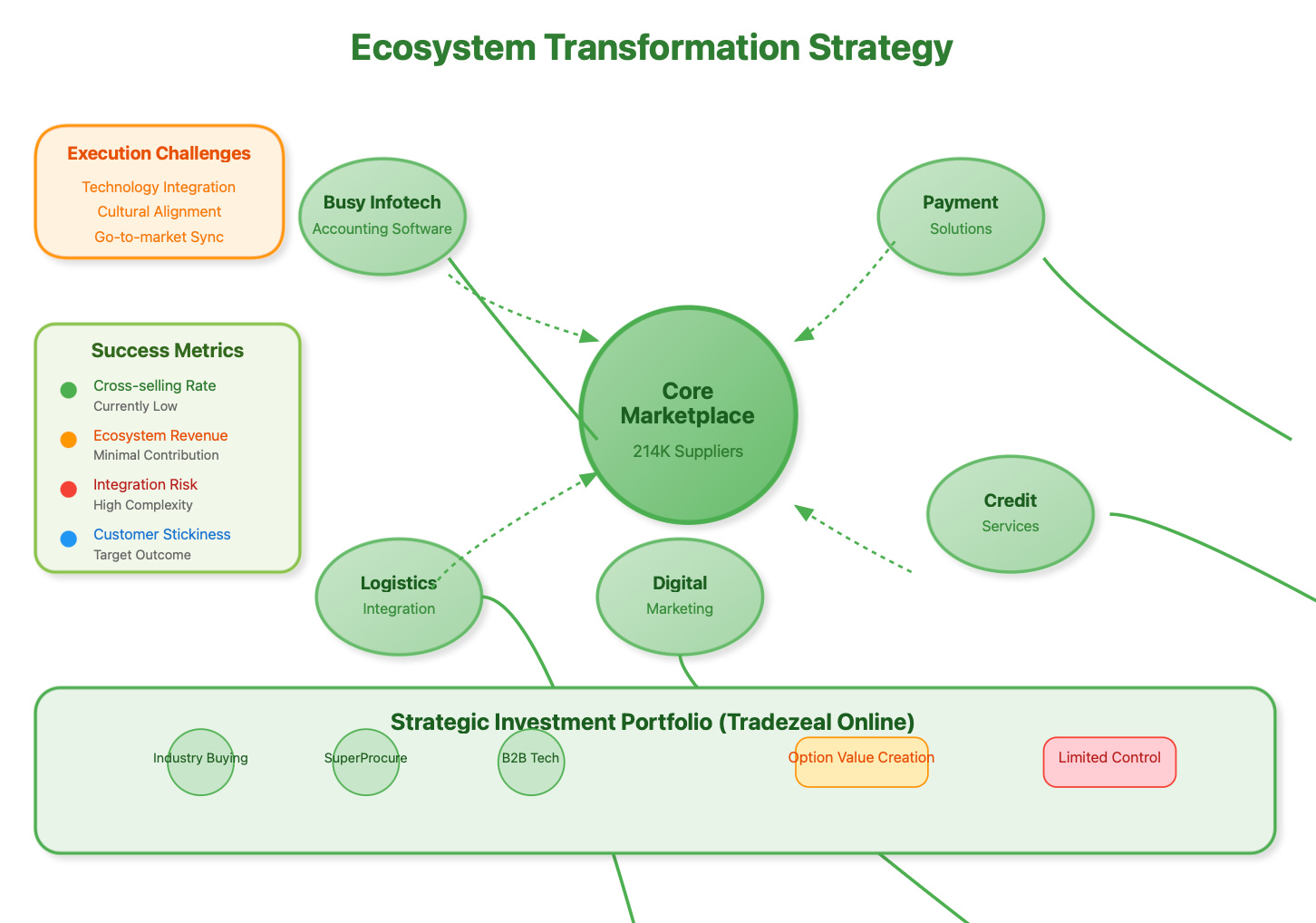

IndiaMART's strategic pivot toward comprehensive SME services through acquisitions and partnerships represents acknowledgment that pure marketplace models face structural limitations. The integration of Busy Infotech's accounting software with marketplace services creates cross-selling opportunities and increased customer stickiness.

However, ecosystem expansion presents substantial execution challenges. Different software categories require distinct customer success approaches, technical architectures, and go-to-market strategies that marketplace expertise doesn't necessarily translate into.

The subsidiary consolidation plan, involving amalgamation of wholly-owned entities, signals management focus on operational efficiency over growth acceleration. While this streamlines reporting and reduces compliance costs, it may also indicate a defensive posture that constrains aggressive competitive responses.

Revenue contribution from ecosystem services remains minimal compared to core marketplace subscriptions. The success of IndiaMART's transformation strategy depends on achieving meaningful cross-revenue generation from integrated services rather than standalone product offerings.

Institutional Investor Perspective Divergence

Recent institutional activity reflects growing skepticism about IndiaMART's growth trajectory despite strong current profitability. Nomura's downgrade from "Buy" to "Neutral" with target reduction from ₹3,150 to ₹1,900 specifically cited subscriber retention concerns that management discussions minimize.

Foreign institutional investor holdings increased by 0.77% recently, but this modest increment contrasts with significant target price revisions by research analysts. The divergence between management optimism in earnings calls and institutional skepticism in research reports suggests deeper due diligence reveals concerns that public disclosures don't fully address.

Mutual fund holdings patterns indicate tactical positioning rather than long-term conviction. Several growth-focused funds have reduced positions while value-oriented investors have maintained exposure, reflecting the transition from growth story to value realization opportunity.

The institutional perspective emphasizes execution metrics over narrative positioning. Investor focus has shifted from subscriber growth rates to retention quality, ecosystem revenue contribution, and strategic investment returns rather than traditional marketplace expansion indicators.

Valuation Framework Recalibration Requirements

IndiaMART's current 26.5x P/E multiple appears attractive relative to high-growth peers but may not reflect the company's evolving risk profile. Traditional SaaS and marketplace valuation methodologies become less applicable as the business model transitions toward integrated ecosystem services.

The market's challenge lies in assessing ecosystem transformation success metrics. Revenue diversification, cross-selling effectiveness, and integrated service adoption rates become more relevant than pure marketplace growth indicators.

Enterprise value relative to cash generation capabilities suggests reasonable downside protection. However, the opportunity cost of conservative capital allocation may not generate returns commensurate with the competitive advantages that aggressive strategic investments could create.

Comparable company analysis becomes complex as IndiaMART evolves beyond pure marketplace positioning. Valuation frameworks must incorporate both marketplace cash generation and ecosystem expansion optionality to reflect the company's dual strategic positioning.

Strategic Risk Assessment Framework

The primary execution risk lies in ecosystem integration complexity. IndiaMART's acquisition strategy requires seamless technology integration, cultural alignment, and coordinated go-to-market execution across diverse software categories.

Customer migration from marketplace-only to integrated ecosystem services presents operational challenges. Different service categories require distinct customer success methodologies and technical support capabilities that marketplace operations don't necessarily provide.

Competitive response risks intensify as established players recognize the threat from ecosystem strategies. Amazon Business and Flipkart Business possess deeper financial resources and integration capabilities that could neutralize IndiaMART's ecosystem advantages.

Technology obsolescence represents an ongoing risk requiring continuous innovation investment. The company's technology advantages in matching algorithms and search capabilities require constant enhancement to maintain differentiation in rapidly evolving competitive landscapes.

Investment Thesis Evolution

IndiaMART's investment opportunity has fundamentally shifted from growth story to transformation thesis. Success metrics should emphasize ecosystem revenue contribution, customer lifetime value improvement, and strategic investment returns rather than traditional subscriber growth indicators.

The company's dominant market position and substantial cash resources provide the foundation for successful strategic pivoting that smaller competitors cannot execute. However, transformation success depends on execution effectiveness rather than financial capability alone.

For sophisticated investors, IndiaMART represents a complex strategic transformation play rather than straightforward growth investment. The regulatory disclosures provide clearer insights into operational challenges than management presentations suggest, requiring careful analysis of execution progress against stated strategic objectives.

Forward-Looking Implications

IndiaMART's strategic evolution reflects broader trends in B2B commerce where pure marketplace models face structural challenges from integrated service providers. The company's response through ecosystem expansion and strategic investments represents both acknowledgment of these challenges and potential solution pathways.

The success of IndiaMART's transformation strategy will influence competitive dynamics across India's B2B commerce landscape. Other marketplace operators face similar structural pressures, making IndiaMART's execution a bellwether for the entire sector's evolution.

Investment decision-making should focus on transformation execution metrics rather than traditional growth indicators. Regulatory filings and operational disclosures provide more reliable insights into strategic progress than earnings call narratives, making detailed analysis essential for accurate assessment.

The opportunity lies in successful ecosystem expansion that leverages IndiaMART's market leadership and financial strength to create integrated competitive advantages that pure marketplace models cannot replicate. Success will be measured by ecosystem revenue contribution and customer value expansion rather than subscriber count growth alone.

You have gone after Indiamart that all share holders should cash out and abandon the company. Could you build such a firm whom customers like, shareholders finds value, technology wonks don't pull their hair out in spite of being a technology and market leader.

Great flow of networks, thanks for the writeup