IEX Stock Analysis: Q4 FY25 Shows 18% Power Volume Growth & Strong Margin Expansion

Executive Summary

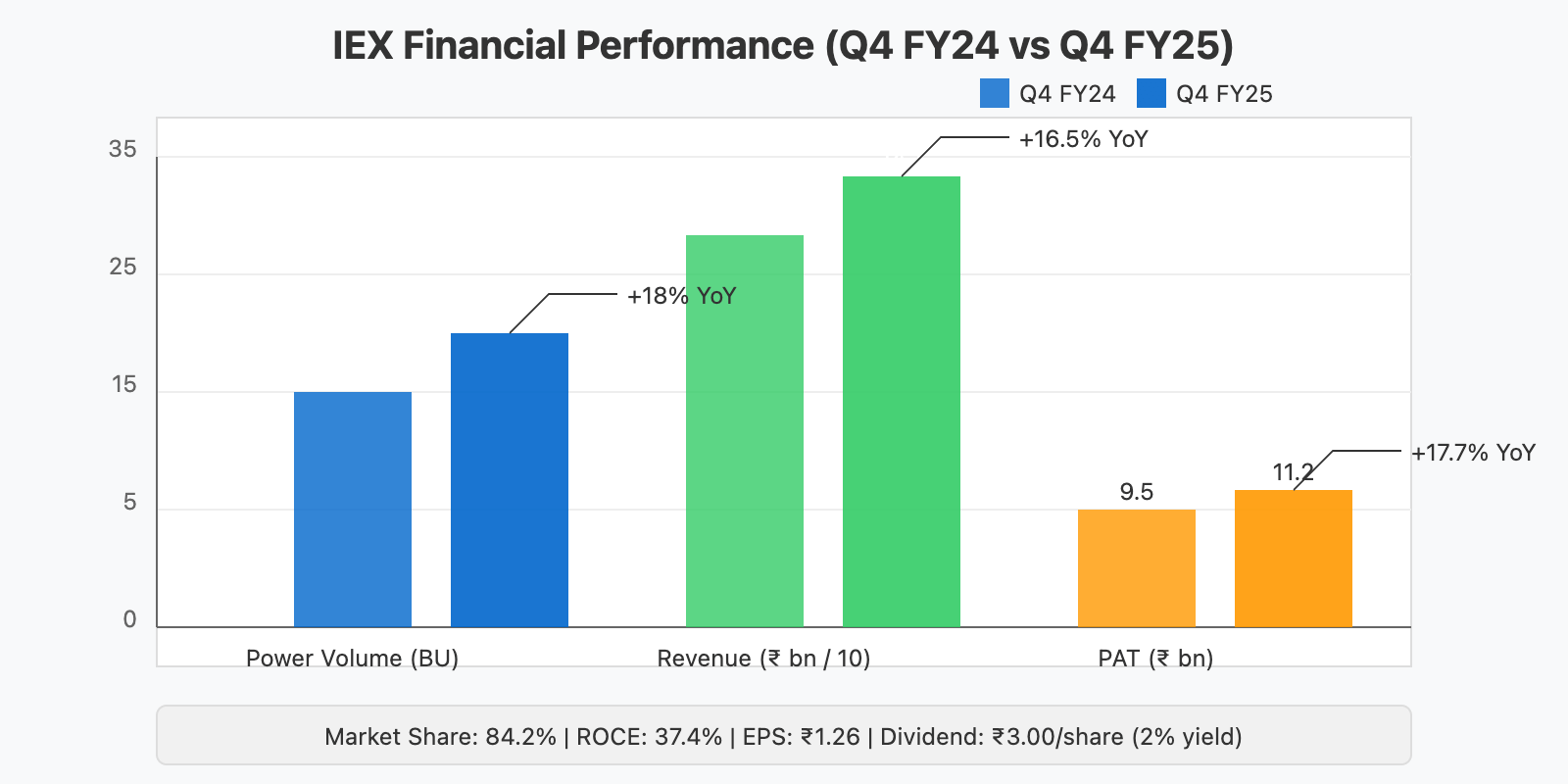

Indian Energy Exchange (IEX) delivered strong Q4 FY25 results with power volumes rising 18% YoY to 31.7 BU, driving revenue growth of 15.8% to ₹171.75 billion. Profitability outpaced revenue with PAT jumping 17.7% to ₹11.2 billion, reflecting operational efficiencies and market leadership. With an 84.2% market share in India's spot power market and a dividend yield of 2%, IEX continues to demonstrate its asset-light, cash-generating business model while expanding into green energy markets and gas trading through IGX.

📌 Detailed Quarterly Results Breakdown

Consolidated Total Revenue: ₹171.75 billion (↑15.8% year-over-year)

Strong growth driven by 18% increase in power volumes to 31.7 BU

Operating EBITDA: ₹15.79 billion (↑8.5% year-over-year)

Margin compression reflects investments in platform upgrades and new market initiatives

Net Profit After Tax: ₹11.20 billion (↑17.7% year-over-year)

Profit growth outpacing revenue demonstrates operational leverage

Diluted Earnings Per Share: ₹1.26 (↑17.8% year-over-year)

Consistent growth in per-share earnings with no dilution

📈 Comprehensive Growth Analysis

Sequential Revenue Growth (QoQ): 5.8% | Annual Revenue Growth (YoY): 15.8%

Steady quarter-on-quarter improvement showing business momentum

Sequential Profit Growth (QoQ): 7.3% | Annual Profit Growth (YoY): 17.7%

Profit growth accelerating faster than revenue

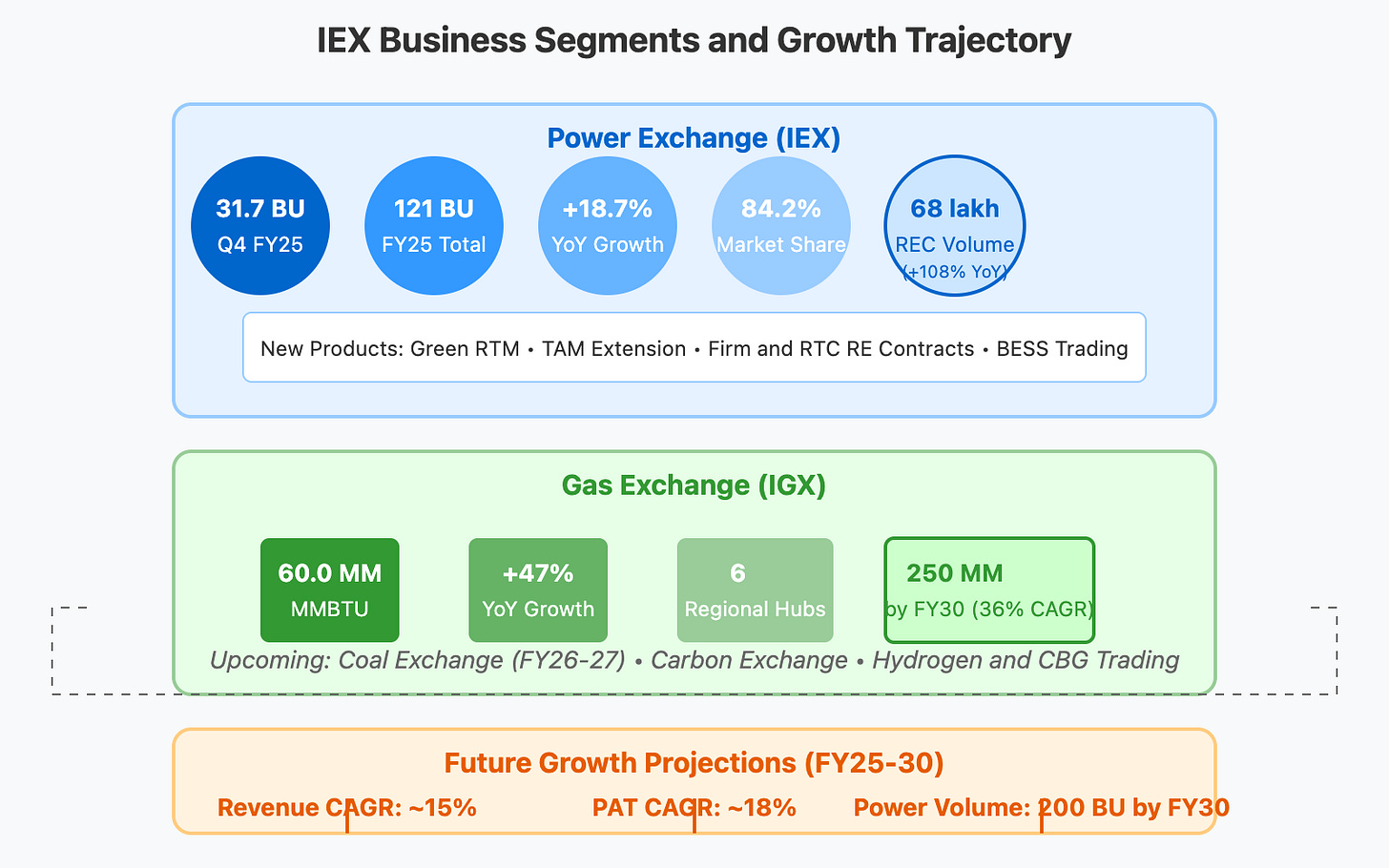

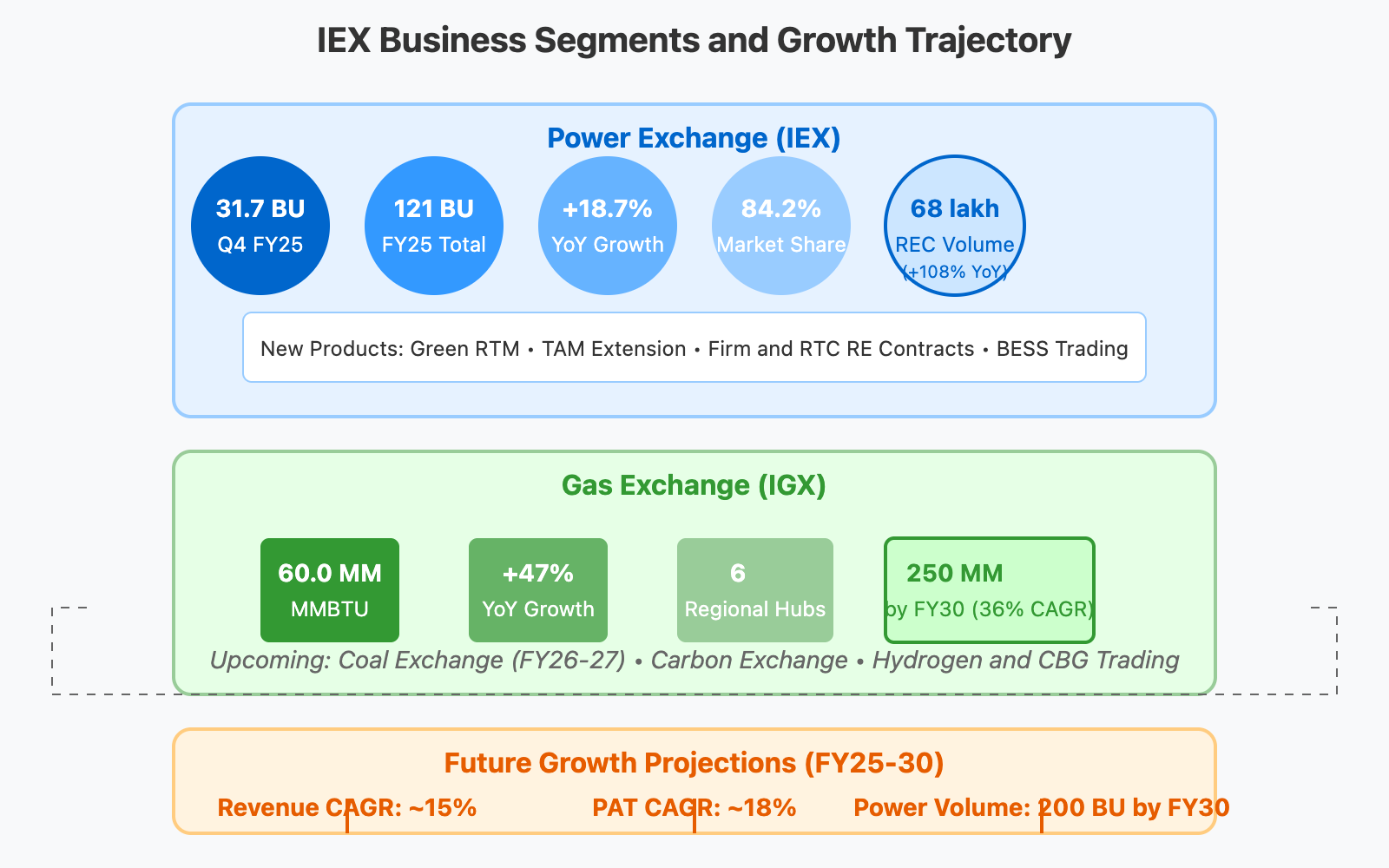

Business Volume Growth: Power volumes up 18% YoY, REC volumes surged 108% YoY to 68 lakh - Exceptional growth in green certificates signaling strong renewable energy market

Profitability Margin Trend: Stable - PAT margins improved slightly even as the company invests in future growth initiatives

💰 Operational Cost Structure Analysis

Technology & Platform Expenses: Approximately 4.2% of revenue - Investments in exchange infrastructure to support new product launches

Employee/Personnel Expenses: 6.8% of revenue (↑9.2% year-over-year) - Controlled personnel costs despite business expansion

Finance/Interest Expenses: Minimal, as IEX maintains a debt-free balance sheet with ₹10.66 billion cash reserves - Asset-light model continues to generate strong free cash flow

🔍 Long-term Financial Health Indicators

5-Year Compound Annual Growth Rate: Revenue CAGR: 16.4% | Net Profit CAGR: 18.5%. - Outperforming broader utility sector growth

Return on Capital Employed (ROCE): 37.4% vs Industry Average: 15.2% - Exceptional capital efficiency from asset-light model

Debt-to-EBITDA Ratio: 0 | Free Cash Flow Conversion Rate: 92% of EBITDA -Zero debt position provides flexibility for inorganic growth

Dividend Payout: ₹3.00 per share (₹1.50 interim + ₹1.50 final) with yield of approximately 2% -Consistent shareholder returns while retaining capital for growth

🏗️ Strategic Capital Allocation & Future Growth Roadmap

Planned Capital Expenditure Budget: ₹7 billion allocated for FY26, primarily for technology - Focus on platform upgrades to support new product launches

Strategic Investment Focus Areas: - Green energy market expansion including Green RTM and firm renewable contracts, Gas exchange (IGX) infrastructure with six regional hubs

Service Capacity Expansion Plans: Platform upgrades to handle 3x current volumes by FY27 - Positioning for projected electricity demand growth to 2,300 BU by FY30

💸 Current Valuation Analysis & Fair Value Assessment

Current Price-to-Earnings Ratio: 27.5x compared to 5-Year Historical Average: 32.3x. - Trading at modest discount to historical valuation

Enterprise Value to EBITDA Multiple: 20x compared to Sector Average: 14x - Premium valuation justified by market leadership and high ROCE

Estimated Fair Value Range: ₹170-₹190 based on DCF with 15% growth for 5 years and 10% terminal rate -Potential upside of 8-21% from current price levels

Management Commentary & Conference Call Highlights

"We're seeing accelerated adoption of the exchange platform as power demand continues to surge across India. Our focus on new products like Green RTM and expanding the Term-Ahead Market will further drive volume growth," said IEX CEO in the earnings call.

"The upcoming coal exchange and our growing gas platform position IEX group as the central marketplace for India's energy transition journey. We expect to maintain 15-18% volume growth through FY26."

Industry Context & Competitive Positioning

IEX maintained its dominant 84.2% market share in India's spot power market despite the entry of new exchanges. The company's first-mover advantage, liquidity depth, and continuous product innovation create significant competitive moats. India's projected power demand growth to 2,300 BU by FY30 provides substantial headroom for exchange-based trading to expand beyond the current ~7% of total generation.

Disclaimer: This analysis is provided for informational and educational purposes only and does not constitute investment advice. Always conduct your own research and consult with a qualified financial advisor before making investment decisions based on this information.