High Energy Batteries: Powering Value Through Aerospace & Defence Pivot

May 12, 2025 — A deep dive into the fundamentals, growth trajectory, and investment potential of this mid-cap energy storage specialist.

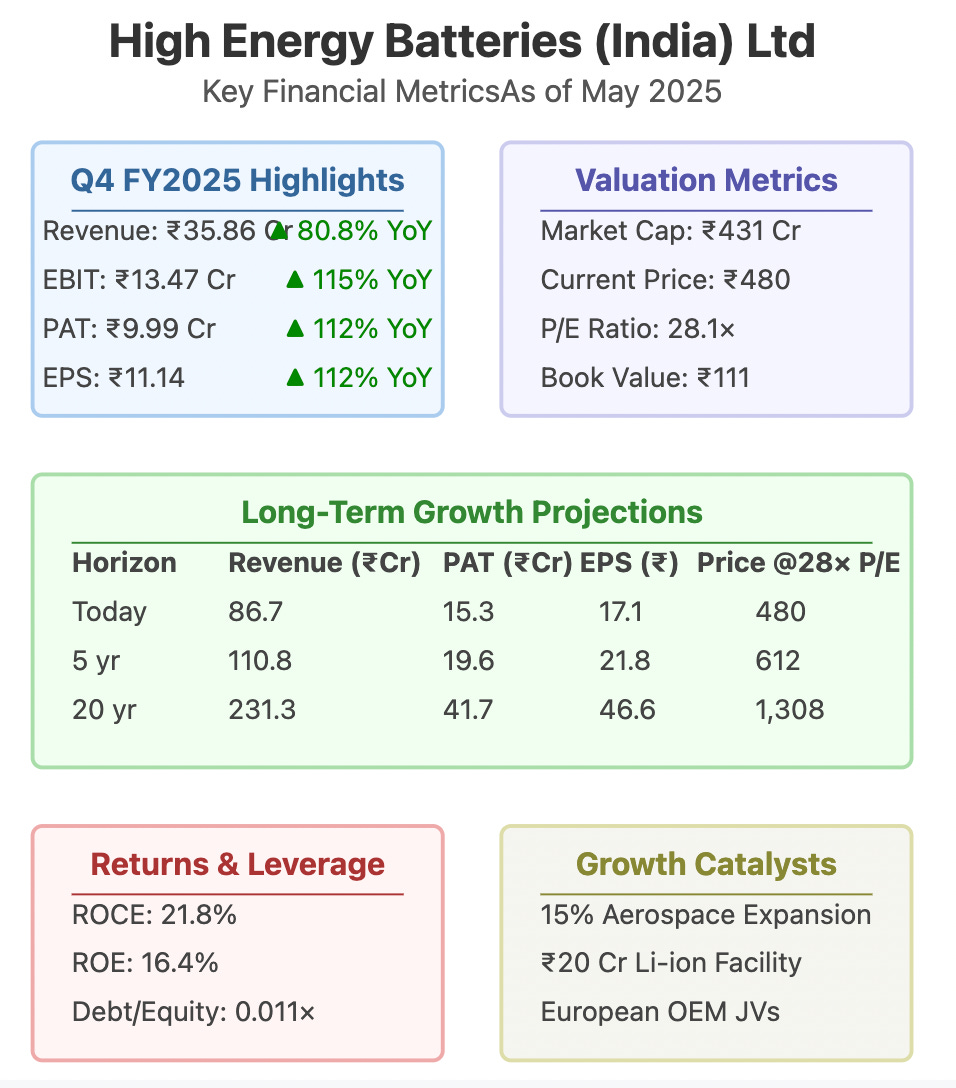

High Energy Batteries (India) Ltd has delivered impressive Q4 FY2025 results with revenue surging 80.8% year-over-year to ₹35.86 Cr. The company's strategic pivot toward high-margin aerospace and defence segments is beginning to yield tangible results, despite full-year profits showing some pressure due to rising input costs.

Stellar Q4 Performance Signals Turnaround

The company posted remarkable quarterly growth with:

80.8% YoY revenue growth

115% YoY EBIT growth to ₹13.47 Cr

112% YoY PAT growth to ₹9.99 Cr

This exceptional performance underscores management's successful execution in securing critical aerospace and power systems orders while optimizing raw material costs.

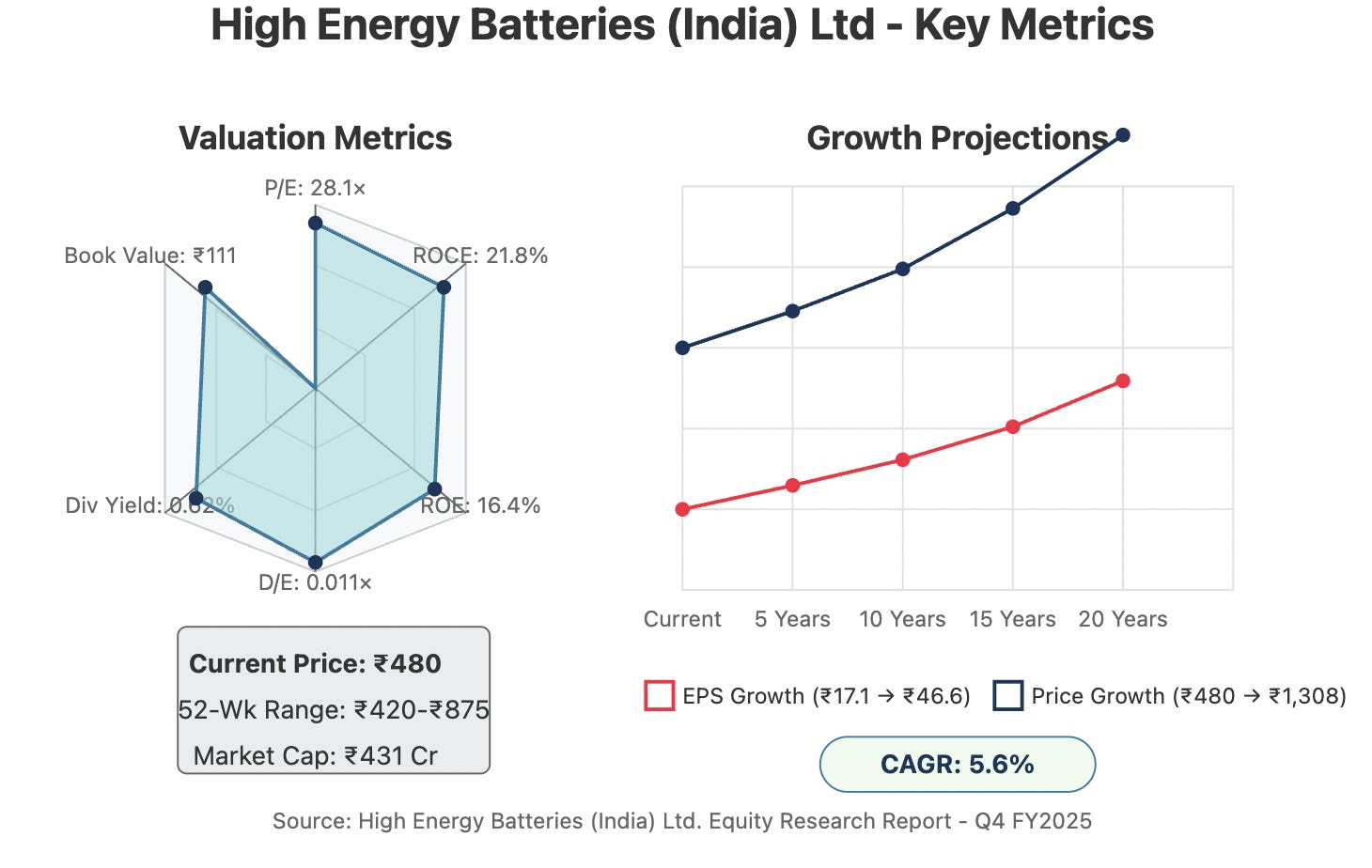

Valuation: Premium Justified by Quality

Trading at ₹480, the stock commands a P/E of 28.1× FY2025 earnings, representing a premium to mid-cap peers that typically trade at 18-22×. With ROCE exceeding 20% and negligible debt (D/E of just 0.011×), this premium appears justified if the company can accelerate growth from its historical flat trajectory to 10-12% annually.

Shareholder Returns & Financial Health

The company maintains strong financials with:

Recommended dividend of ₹3.00/share (0.62% yield)

150% dividend payout ratio

Book value of ₹111 per share

Negligible debt of ₹11.2 Cr against reserves of ₹97.8 Cr

This conservative financial approach provides ample flexibility for funding the company's ambitious growth plans.

Growth Catalyst: Li-ion & Defence Focus

High Energy Batteries is positioning for sustained long-term growth through:

15% capacity expansion in aerospace/naval batteries

₹20 Cr greenfield facility in Pudukkottai for Li-ion cells

R&D investment in lithium-ion systems for defence

Potential JVs with European OEMs for defence-grade energy systems

Long-Term Investment Case

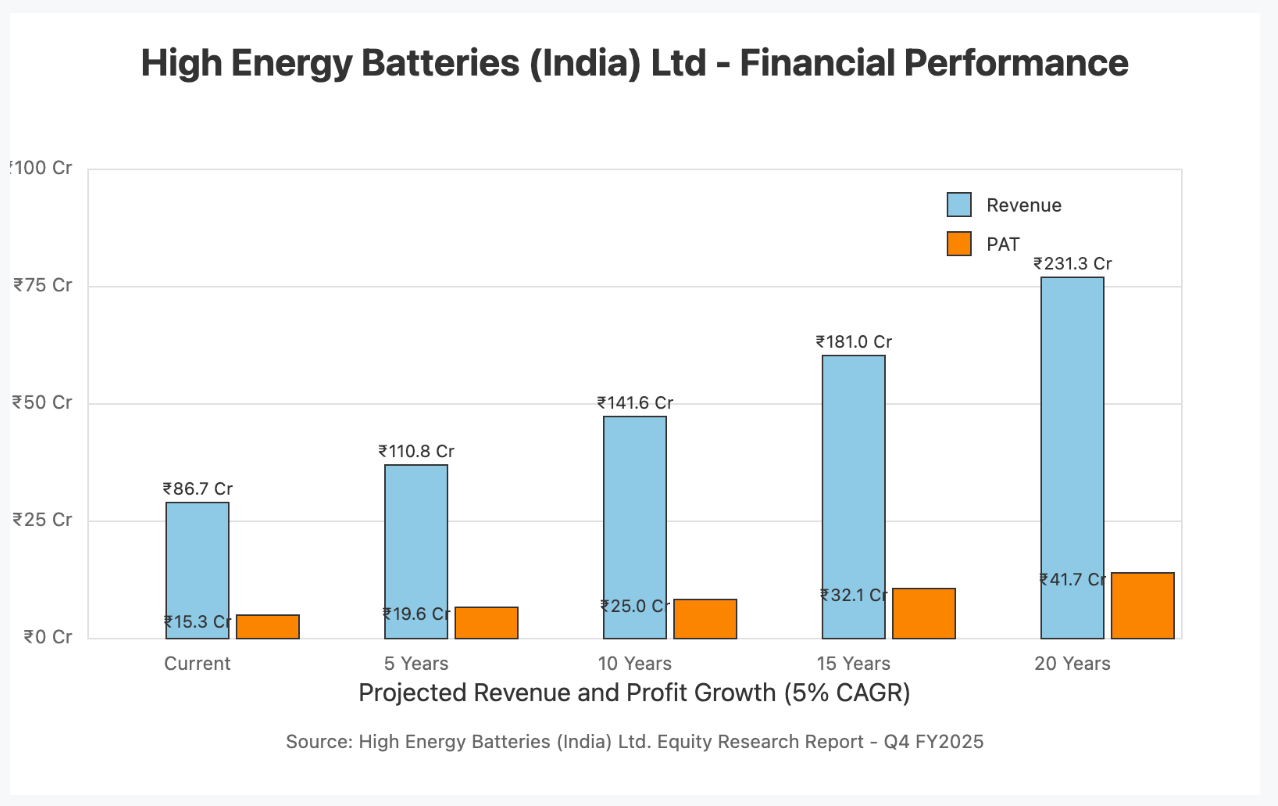

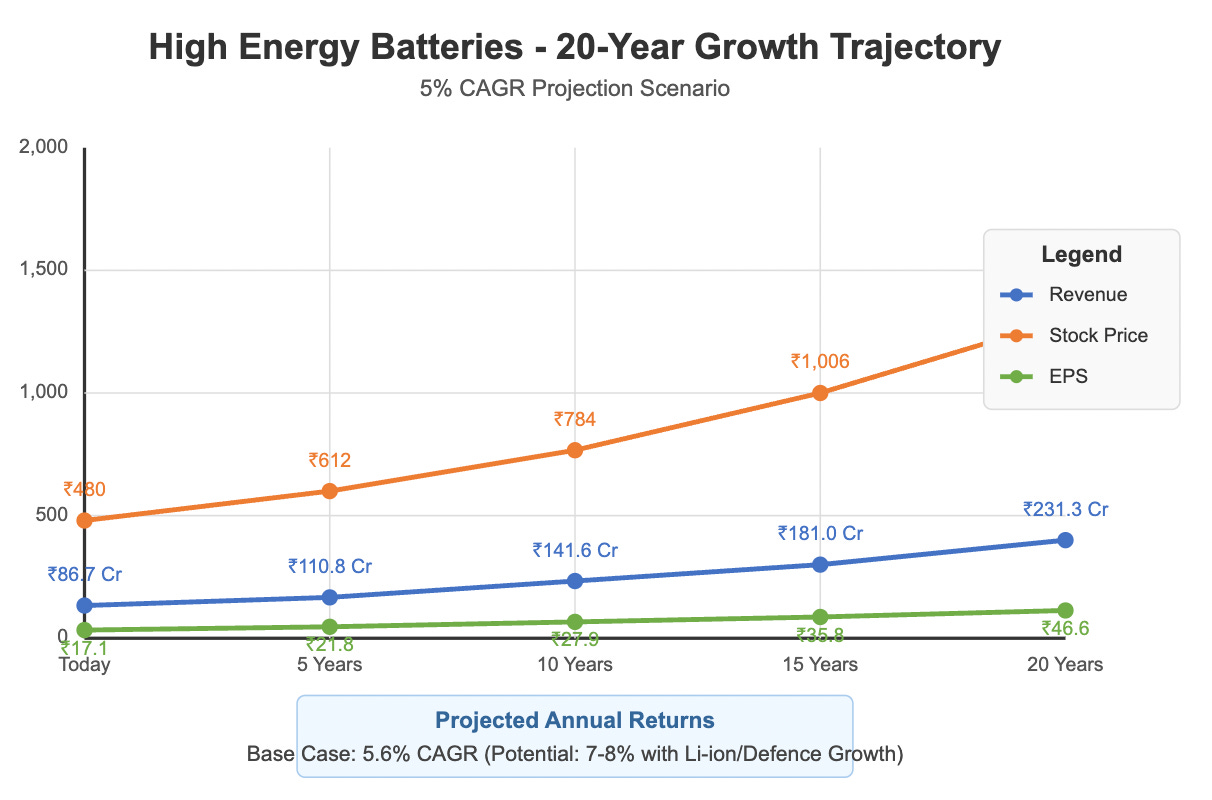

Based on a conservative 5% revenue CAGR and stable 20% operating margins, investors can expect:

5-year EPS growth to ₹21.8 (from current ₹17.1)

10-year EPS growth to ₹27.9

15-year EPS growth to ₹35.8

20-year EPS growth to ₹46.6

This translates to a base-case 5.6% price CAGR, with upside potential to 7-8% if higher-margin segments grow faster than projected.

Investment Conclusion

High Energy Batteries represents a compelling proposition for investors seeking quality, dividend income, and steady capital appreciation. The company's transition to higher-margin segments, debt-free status, and clear growth strategy position it well for the evolving energy storage landscape.

The current valuation demands patience, but for long-term investors focused on quality businesses with strong returns on capital, High Energy Batteries warrants serious consideration for portfolio inclusion.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors should perform their own due diligence or consult a financial adviser before making investment decisions.