Hidden Auto Component Play With 51% Upside Potential

This stock’s trading at a premium, but the growth engine underneath is just getting warmed up. The company’s pulling in double-digit revenue growth quarter after quarter, margins are holding steady even as they scale up, and they’re sitting on a growing cash pile from operations. The market’s priced in the premium valuation, but it hasn’t fully caught up to where the earnings trajectory is headed over the next 3-5 years.

Business Model & Operations

Think of this business as the behind-the-scenes supplier that makes your car work. They manufacture over 25 different types of components - switches that control your windows, lights that help you see at night, alloy wheels, acoustic systems, even the seats you sit on. They’re not selling to you and me directly. Instead, they supply to the big automakers - the Marutis, Hyundais, Tatas, and Mahindras of the world.

What makes them interesting is they’re not stuck in the old world. They’re making parts for both traditional petrol/diesel cars and the new electric vehicles. So whether India goes fully electric tomorrow or takes another decade, they’re covered on both sides. They’ve got manufacturing plants spread across India and even some international operations.

Lately, they’ve been busy expanding capacity and launching new product lines. They’re investing heavily in EV components because they see where the market’s headed. New factories are coming up, technology partnerships are being signed, and they’re moving up the value chain from simple components to more complex systems. That’s where the real money is

Historical Financial Review

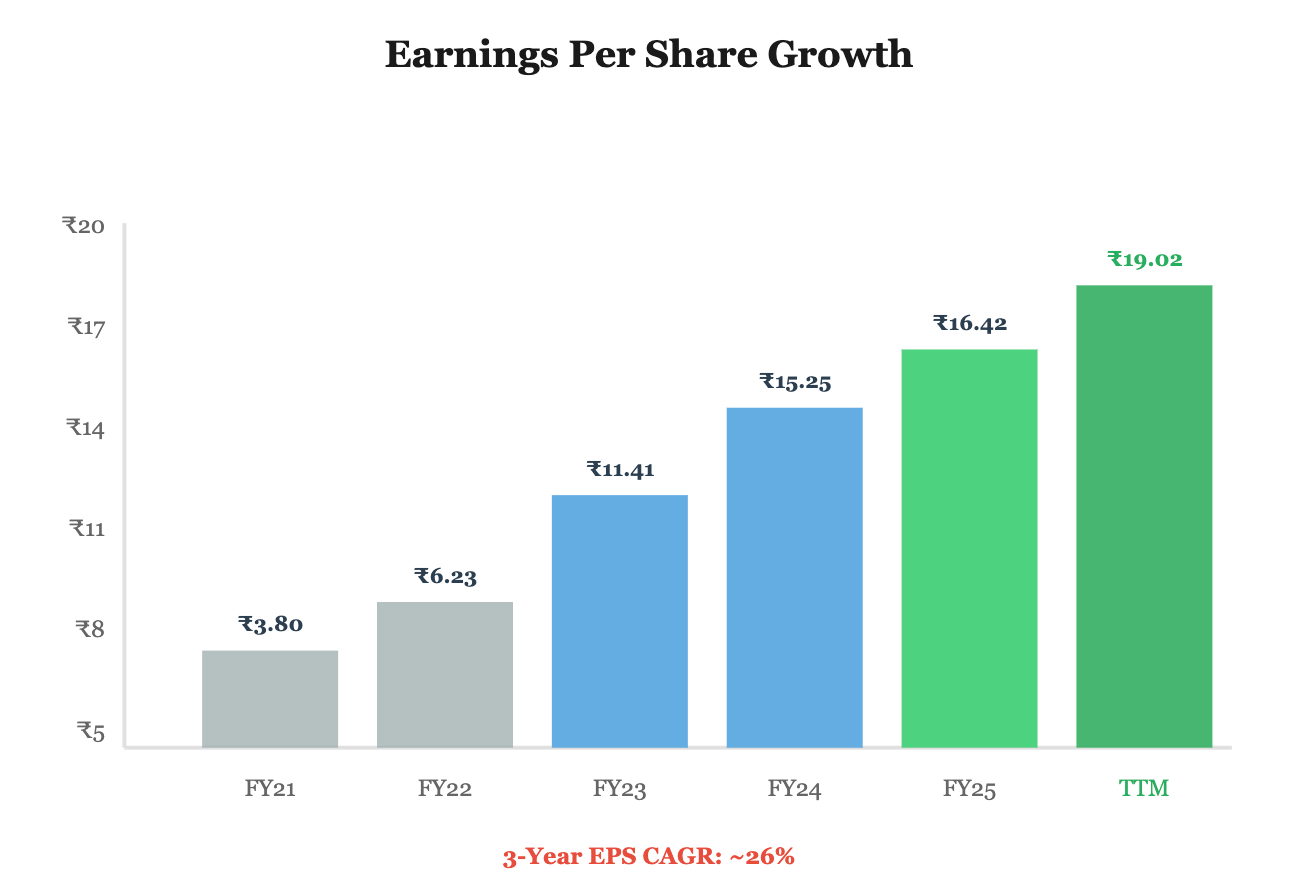

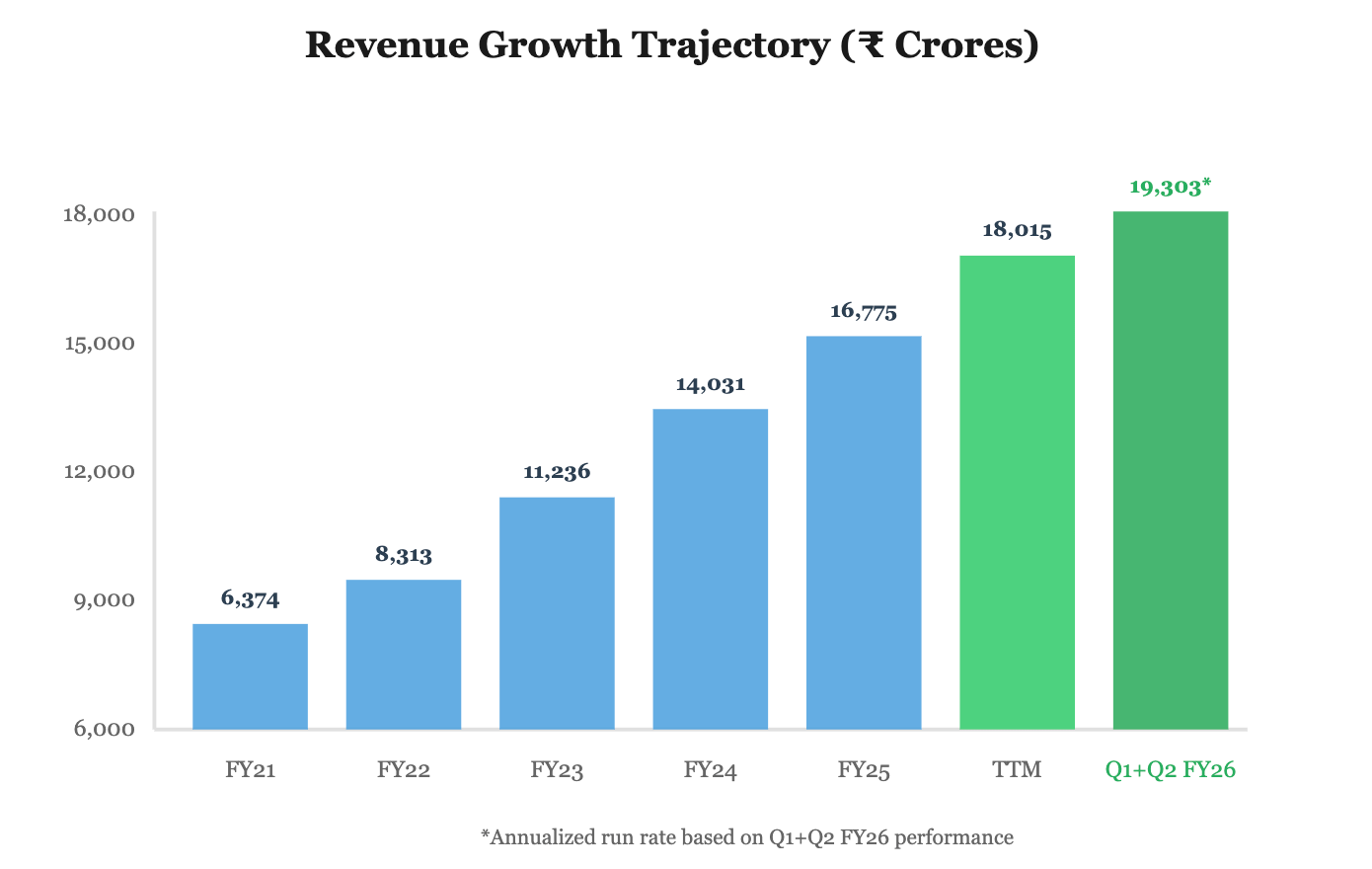

Let’s talk numbers that actually mean something. Over the past three years, revenue has grown at a solid 26% annually. That’s not just inflation - that’s real business growth. Last year alone, they posted earnings of ₹16.42 per share. Compare that to where they were just three years ago at ₹11.41 per share, and you can see the profit machine accelerating.

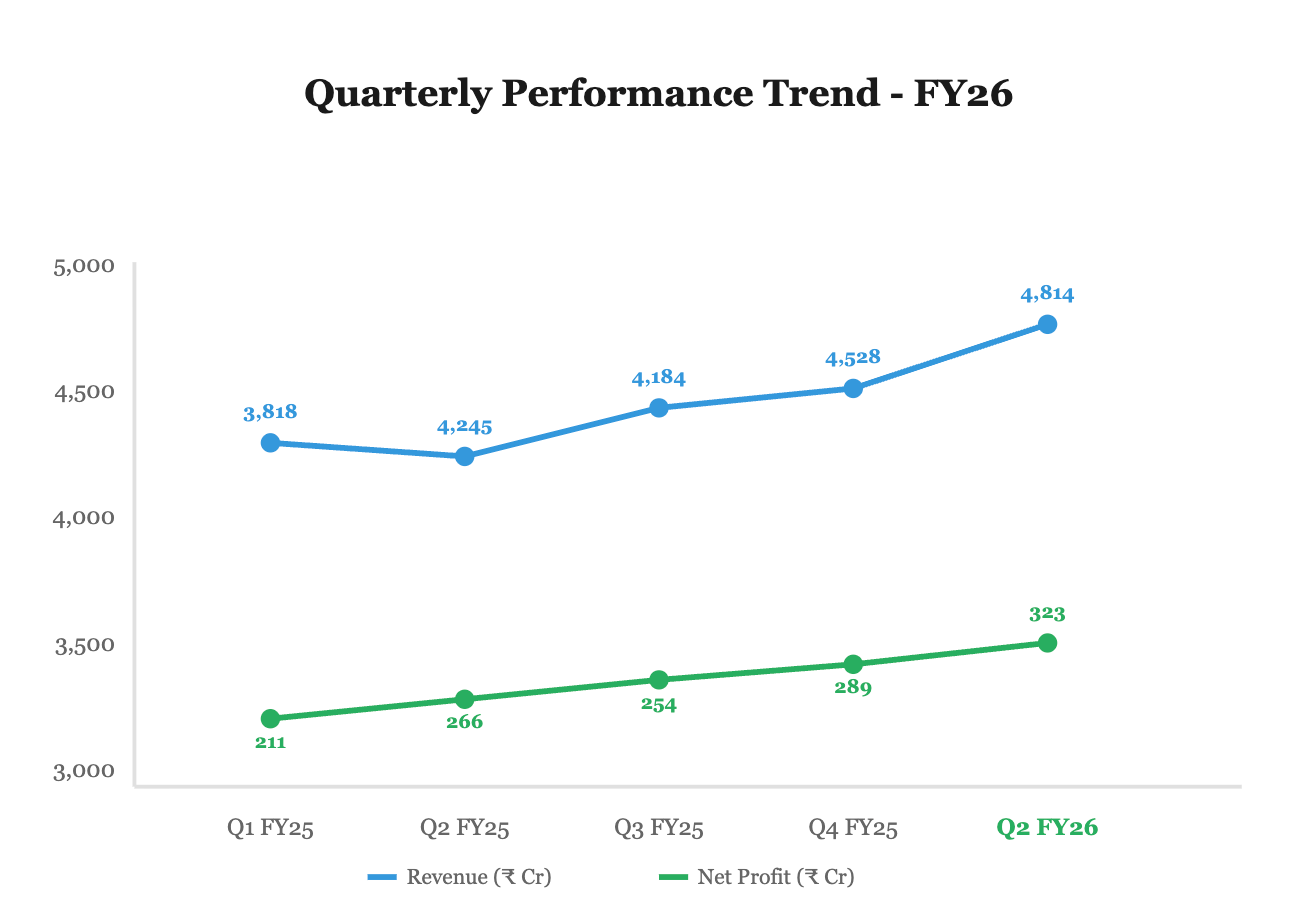

Now here’s what’s really interesting - look at the quarterly performance for the current fiscal year. In Q1 FY26 (April-June 2025), they hit ₹4,489 crores in revenue with a net profit of ₹309 crores. That’s an EPS of ₹5.06 for just one quarter. Then in Q2 (July-September 2025), revenue jumped to ₹4,814 crores with profit climbing to ₹323 crores - EPS of ₹5.27.

Do the math on that quarterly run rate, and you’re looking at potential annual EPS approaching ₹20-21 for FY26. The momentum is clearly building. Quarter over quarter, they’re adding revenue and converting it to profit efficiently. Operating margins have stayed rock-solid around 11-12% even as they scale up.

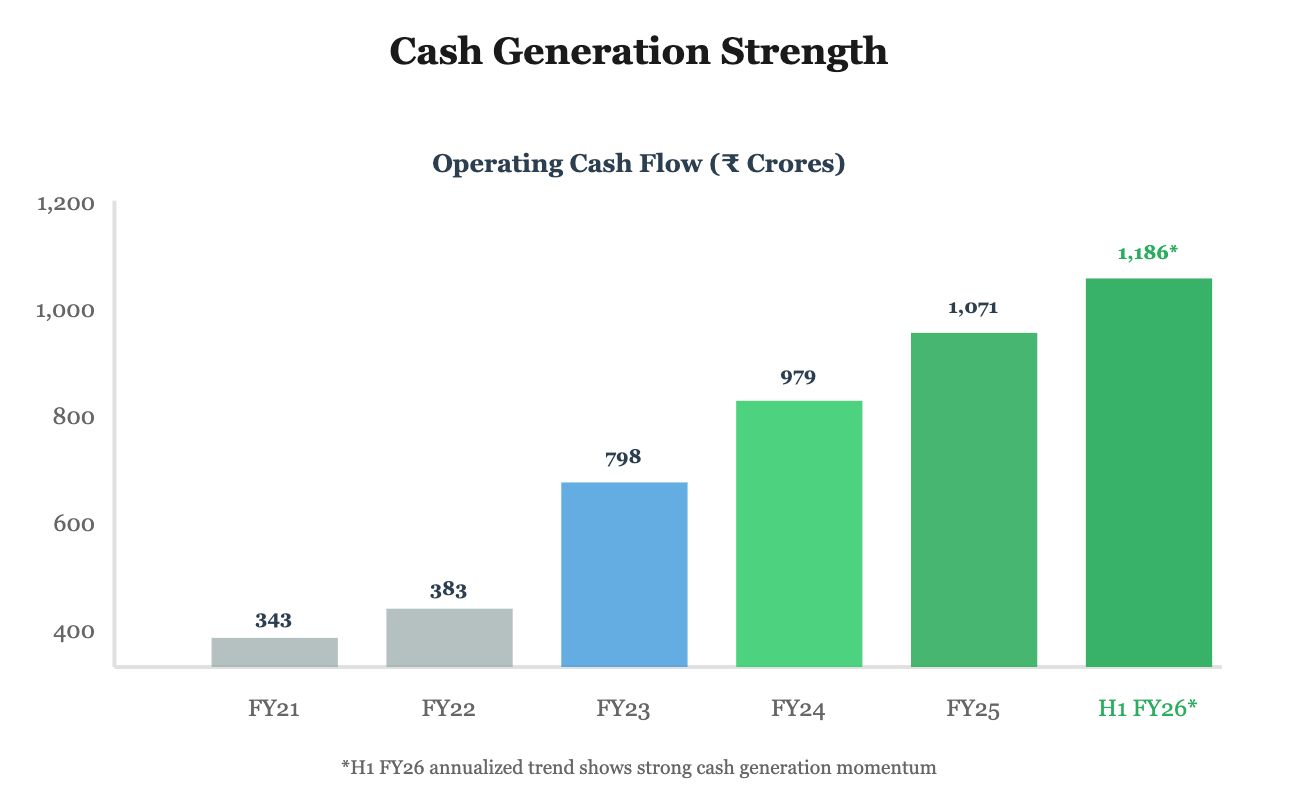

Their operating cash flow per share has been climbing too - they generated ₹1,071 crores in operating cash for FY25. That’s real money coming in, not just accounting profits. When you see a company consistently turning revenues into actual cash, that’s a good sign they’re running a tight ship.

Valuation & Expected Returns

The stock’s currently trading at a P/E of around 64 based on trailing twelve months. Yeah, that’s expensive by traditional standards. But here’s where it gets interesting - if they hit that ₹20+ EPS in FY26 and maintain their growth trajectory, the P/E compresses fast. At ₹1,223, you’re paying for growth that’s actually showing up in the numbers.

My target price of ₹1,850 gives you about 51% upside over the next 12-18 months. That’s based on a more reasonable P/E of 35-40x on forward earnings of ₹22-24 per share by FY27. Not crazy multiples for a company growing profits at 20-25% annually.

Look out 5 years, and if they can sustain even 18-20% earnings growth (below their recent track record), you’re looking at EPS hitting ₹40-45. Slap a market multiple of 30-35x on that, and you’re at ₹1,400-1,575 as a conservative base case. Best case with premium multiples? North of ₹2,000. That’s a 10-12% annual return just from multiple compression, plus another 8-10% from earnings growth. Total expected returns in the 15-20% range annually.

Growth Drivers & Catalysts

The Indian auto sector’s been on a tear, and this company rides that wave. Passenger vehicle sales are growing, commercial vehicles are picking up, and two-wheelers remain strong. Every car sold needs their components.

The shift to electric vehicles is a massive opportunity. They’re already supplying to EV makers and ramping up capacity. As EV penetration grows from 2-3% today to 10-15% over the next few years, their EV revenue will multiply.

They’re also moving beyond just India. Export markets are opening up, particularly in Europe and Southeast Asia. That geographic diversification reduces dependence on the domestic cycle and taps into higher-margin international business.

Technology upgrades matter too. Modern cars have way more electronics than old ones - advanced driver assistance systems, connected car tech, sophisticated lighting. All of that means higher value per vehicle for component suppliers who can deliver these systems.

Risk Factors

Let’s be honest about what could go wrong. The valuation is stretched - if growth disappoints even slightly, the stock could correct sharply. That P/E of 64 doesn’t leave much room for error.

They’re dependent on the auto sector, which is cyclical. If vehicle sales slow down due to economic weakness, interest rate hikes, or regulatory changes, their revenue takes a direct hit. There’s no diversification outside automotive.

Raw material costs are a constant worry. Aluminum, steel, plastics - when these spike, margins get squeezed unless they can pass costs to automakers. And automakers are tough negotiators who constantly push suppliers on price.

Competition is intense. Other component makers are chasing the same customers and the same EV opportunity. If they lose market share or big contracts, growth stalls fast.

Debt levels have been creeping up as they invest in expansion. Total borrowings hit ₹2,473 crores in FY25. That’s not scary yet, but it needs watching. Higher interest rates could eat into profitability.

The Bottom Line

This is a quality business with strong fundamentals trading at a premium valuation. If you believe in India’s auto story and the EV transition, this is one of the better ways to play it. The quarterly momentum is strong, management execution has been solid, and they’re positioned in the right segments.

The risk-reward looks favorable for a 12-18 month horizon. Yes, you’re paying up for quality and growth. But sometimes that’s okay when the growth actually materializes. I’d start building a position here and add on any dips toward ₹1,100-1,150.

For conservative investors, wait for a pullback. For those comfortable with growth stocks, current levels offer a decent entry. Just don’t bet the farm at these valuations.

Disclaimer: This analysis is for educational and informational purposes only and should not be considered as investment advice. All data is sourced from NSE India, BSE India, and Screener.in as of the dates mentioned. Past performance does not guarantee future results. Please consult with a qualified financial advisor before making any investment decisions. The author may or may not hold positions in the securities discussed.

🎯 Unlock The Company Name :