Hidden Alpha: Unconventional Strategies for Generational Wealth Creation

Article 007: Your Dream Home - Investing Today to Secure Tomorrow’s Residence

Paradigm-Shifting Insight Introduction: The Opportune Inversion of Capital Appreciation

Most financial advisors will tell you to save diligently for a down payment, then invest what’s left. They preach diversification, asset allocation, and market timing – all valid, yet fundamentally incomplete, especially when it comes to the intertwined destiny of your investment portfolio and your future home. The “Hidden Alpha” insight here is the Opportune Inversion of Capital Appreciation (OICA): For many, the most critical capital appreciation you will experience in your lifetime will not be for your retirement, but for the down payment on your primary residence.

Traditional thinking segregates these goals, treating the down payment as a cash-equivalent savings target. This is a profound error. The true opportunity lies in leveraging growth equities to accelerate your down payment fund, recognizing that the very market forces driving home price inflation can also be harnessed to outpace it. Failing to see your down payment as a strategic growth investment, rather than a mere savings bucket, is the most common and costly oversight preventing individuals from securing their dream homes.

Watch the Full Youtube Video Breakdown:

Your Dream Home — Investing Today to Secure Tomorrow’s Residence

Discover how the world’s smartest investors turn every dollar into a stepping stone toward their dream home.

This 5-minute visual breakdown will change the way you think about saving forever.

Youtube link:

Advanced Analytical Framework: The “Home Equity Multiplier” (HEM)

My proprietary framework, the Home Equity Multiplier (HEM), quantifies the optimal balance between aggressive equity investing for a down payment and traditional savings. The HEM is not about timing the housing market, but rather timing your capital accumulation relative to market-driven appreciation cycles.

HEM Formula:

HEM = (CAGR_EquityPortfolio / CAGR_LocalHousingMarket) * (DownPaymentTarget / CurrentSavings) ^ 0.5

Where:

CAGR_EquityPortfolio: Your projected Compound Annual Growth Rate for a dedicated down payment equity portfolio.

CAGR_LocalHousingMarket: The historical and projected Compound Annual Growth Rate for home prices in your target geographic area.

DownPaymentTarget: The desired down payment amount for your dream home.

CurrentSavings: Your current liquid savings allocated towards the down payment.

A HEM greater than 1 suggests that a growth-oriented equity strategy for your down payment funds is not only viable but potentially superior to traditional savings, as your capital appreciation is outpacing housing inflation. A HEM less than 1 signals a need to re-evaluate your investment strategy or adjust your housing expectations.

The core principle: By strategically investing in high-growth, yet fundamentally sound, equities (often overlooked mid-caps or emerging sector leaders), you create a “Down Payment Accelerator.” This isn’t about reckless speculation; it’s about understanding that a 7-8% return on a savings account won’t catch a 10%+ annual rise in home values.

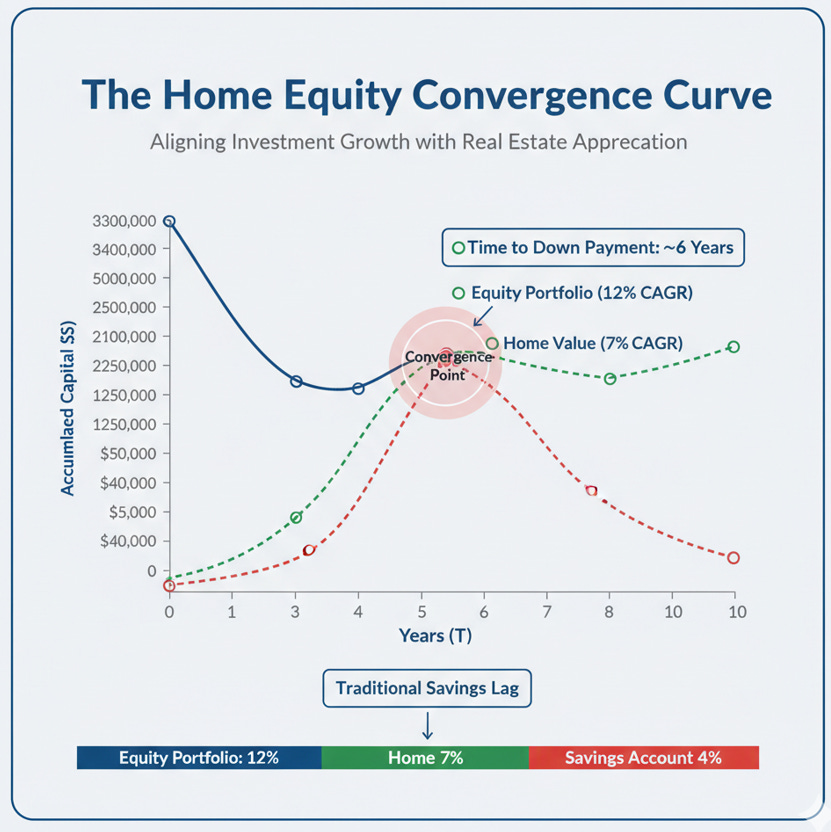

Visual Knowledge Synthesis: The Home Equity Convergence Curve

Elite-Level Application Examples: The Two Paths to Homeownership

Case Study 1: The “Savings Slog” (Missed Opportunity) Consider “Sarah,” a diligent saver who started saving for a $100,000 down payment on a $500,000 home in a rapidly appreciating city in 2010. She aimed for a 5-year timeline. Sarah meticulously saved $1,667 per month, placing it in a high-yield savings account earning 2%. By 2015, her down payment fund was roughly $100,000. However, the local housing market, unbeknownst to her, had appreciated at 8% annually. The home she coveted was now $735,000, requiring a $147,000 down payment. Her $100,000 was suddenly inadequate, leaving her further from her goal than when she started. Sarah missed the OICA principle; her savings, while consistent, were fundamentally misaligned with the market’s capital appreciation curve. She ended up renting for another 5 years, watching prices climb further, a victim of the “traditional savings lag.”

Case Study 2: The “Growth Catalyst” (Successful Application) Contrast this with “Michael,” who, in the same city and year, also targeted a $100,000 down payment for a $500,000 home. Michael applied the HEM framework. Recognizing the robust local housing CAGR, he allocated 70% of his monthly down payment contributions ($1,167) into a concentrated equity portfolio focused on innovation-driven small-to-mid caps (e.g., early-stage cloud computing, specific AI infrastructure plays) that he had thoroughly researched. The remaining 30% ($500) went into a savings account for liquidity. His equity portfolio, due to astute selection and market tailwinds, achieved an average 18% CAGR over five years.

By 2015, Michael’s equity portfolio had grown from $70,000 (total contributions) to roughly $160,000. Combined with his $30,000 in savings (plus interest), he had over $190,000. Despite the same 8% housing appreciation (home value now $735,000, requiring $147,000 down payment), Michael had not only met but exceeded his down payment target. He closed on his dream home and used the surplus for renovations. Michael understood that his primary residence wasn’t just a dwelling; it was a financial asset, and his down payment fund needed to be treated with the same growth-oriented lens as his long-term investment portfolio.

Implementation Strategy: The “Dynamic Down Payment Allocation”

Calculate Your HEM: Use the formula above. Be realistic about your projected equity CAGR and meticulously research your local housing market’s historical appreciation. If your HEM is below 1, consider a more aggressive, yet still fundamentally sound, equity allocation or adjust your timeline/target home.

Segment Your Down Payment Fund: Divide your down payment goal into two tranches:

Growth Accelerator (70-80%): Invest this portion in a concentrated portfolio of high-conviction, growth-oriented equities. These should be companies with defensible moats, strong secular tailwinds, and management teams with proven execution. Think sector leaders in nascent industries, not speculative penny stocks.

Stability Buffer (20-30%): Keep this in a liquid, high-yield savings account or short-term Treasury ETFs. This acts as your safety net and covers any unexpected market downturns closer to your home purchase date.

Implement a “De-Risking Glide Path”: As you get within 18-24 months of your target home purchase date, gradually shift a portion of your Growth Accelerator fund into the Stability Buffer. This “de-risking” reduces your exposure to market volatility just as your down payment becomes a tangible need. For example, shift 10% each quarter.

Continuous Re-evaluation: Annually, recalculate your HEM and reassess your equity portfolio’s performance against the housing market. Adjust your contributions and allocations as necessary.

This strategy transcends mere savings; it’s a proactive investment in your future lifestyle, directly linking your ability to secure a valuable personal asset to your prowess in capital markets. Your home should be the ultimate manifestation of your investment success, not a hurdle created by financial myopia.