HCL Technologies Ltd - Financial Analysis & Growth Outlook (April 2025)

Analyst: Top-Tier Equity Research (April, 2025)

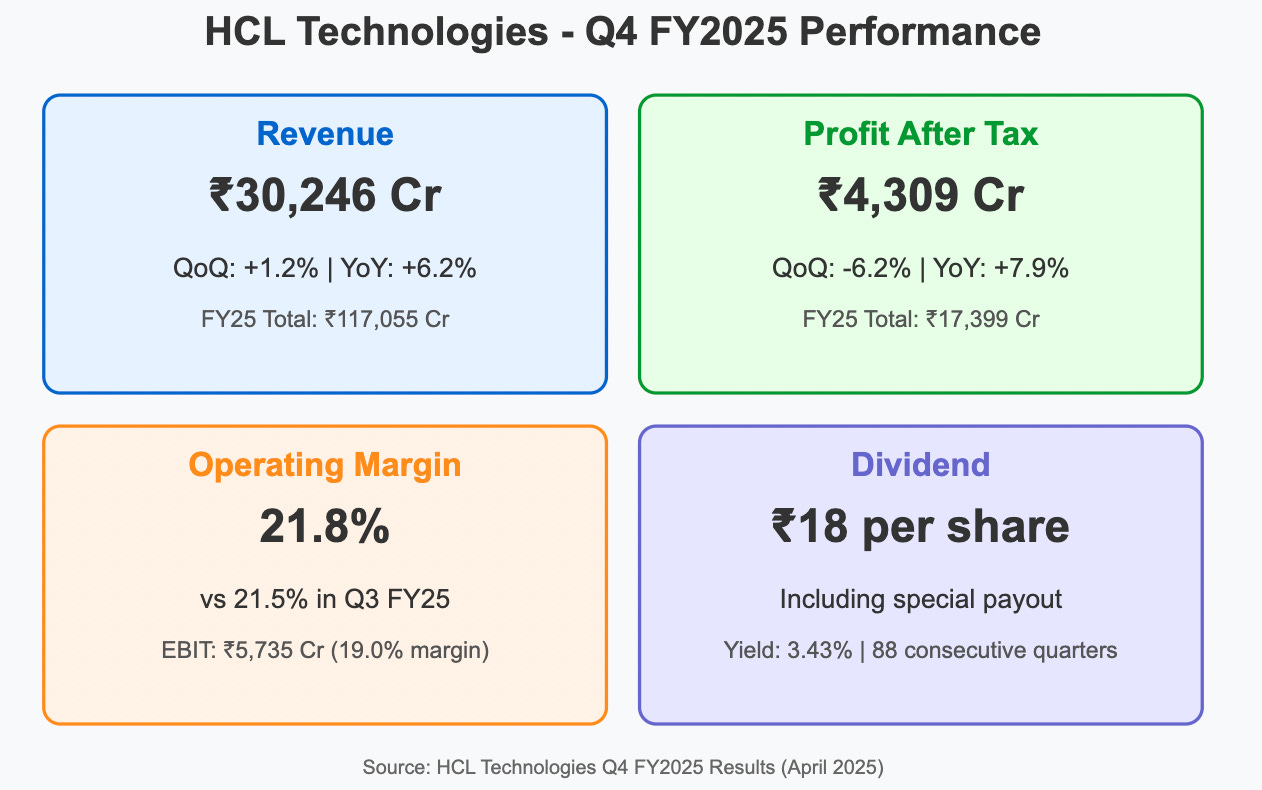

HCL Technologies reported its Q4 FY2025 results, with key performance drivers including robust services growth and strong operating margins at 21.8%. The company delivered solid revenue of ₹30,246 Crore (+1.2% QoQ, +6.2% YoY) and profit after tax of ₹4,309 Crore (+7.9% YoY).

The company's future growth plans are centered on AI investments through their "AI Force" platform and strategic partnerships with hyperscalers. Planned expansions include new development centers in Eastern Europe and Latin America, along with innovation labs in Germany, New Jersey, and Noida.

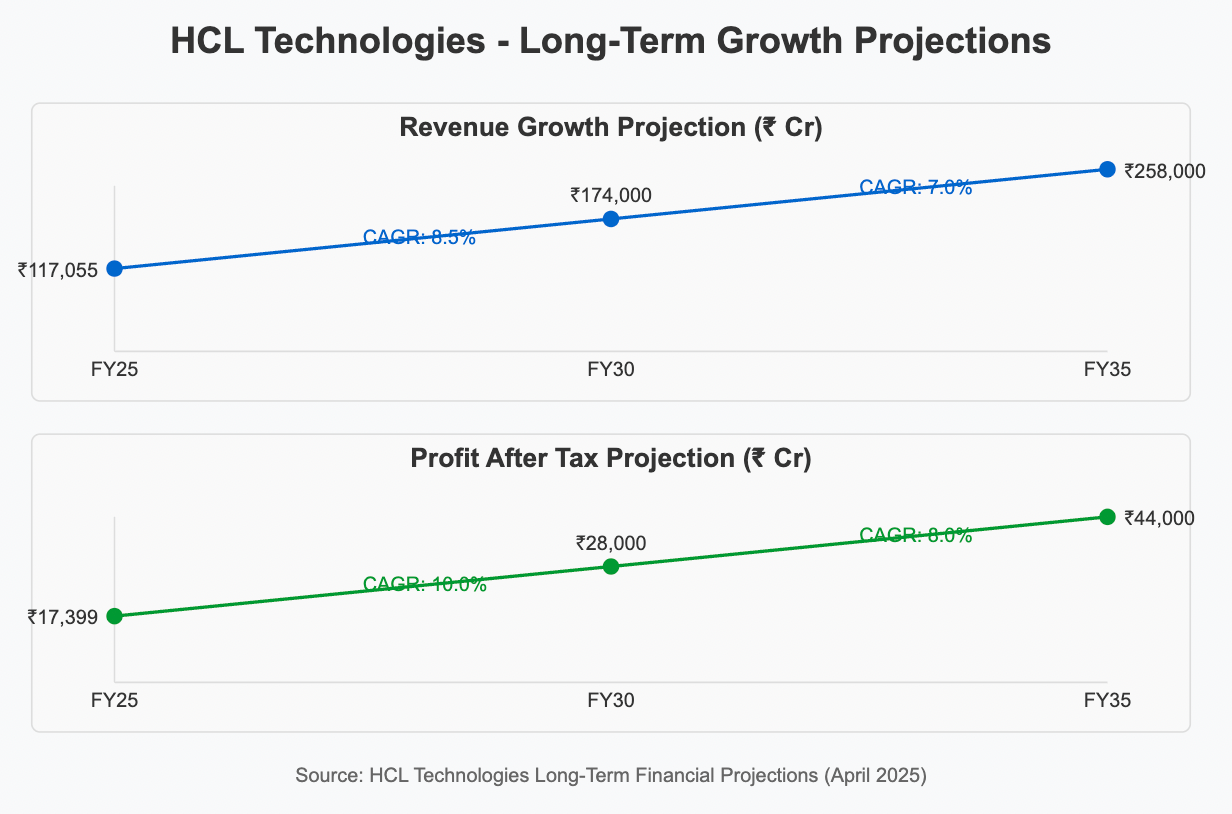

Future financial projections suggest steady growth trajectories with revenue CAGR of 8.5% until FY2030 and 7.0% until FY2035. Potential returns over the next 5, 10, 15, and 20 years indicate promising annualized growth of approximately 15%, 12%, 10%, and 9% respectively, including dividends.

Latest Results Highlights: EBIT margin improved to 19.0% with operating cash flow of ₹22,261 Cr for FY25. The Board declared an interim dividend of ₹18 per share (including special payout), marking 88 consecutive quarters of dividend distribution.

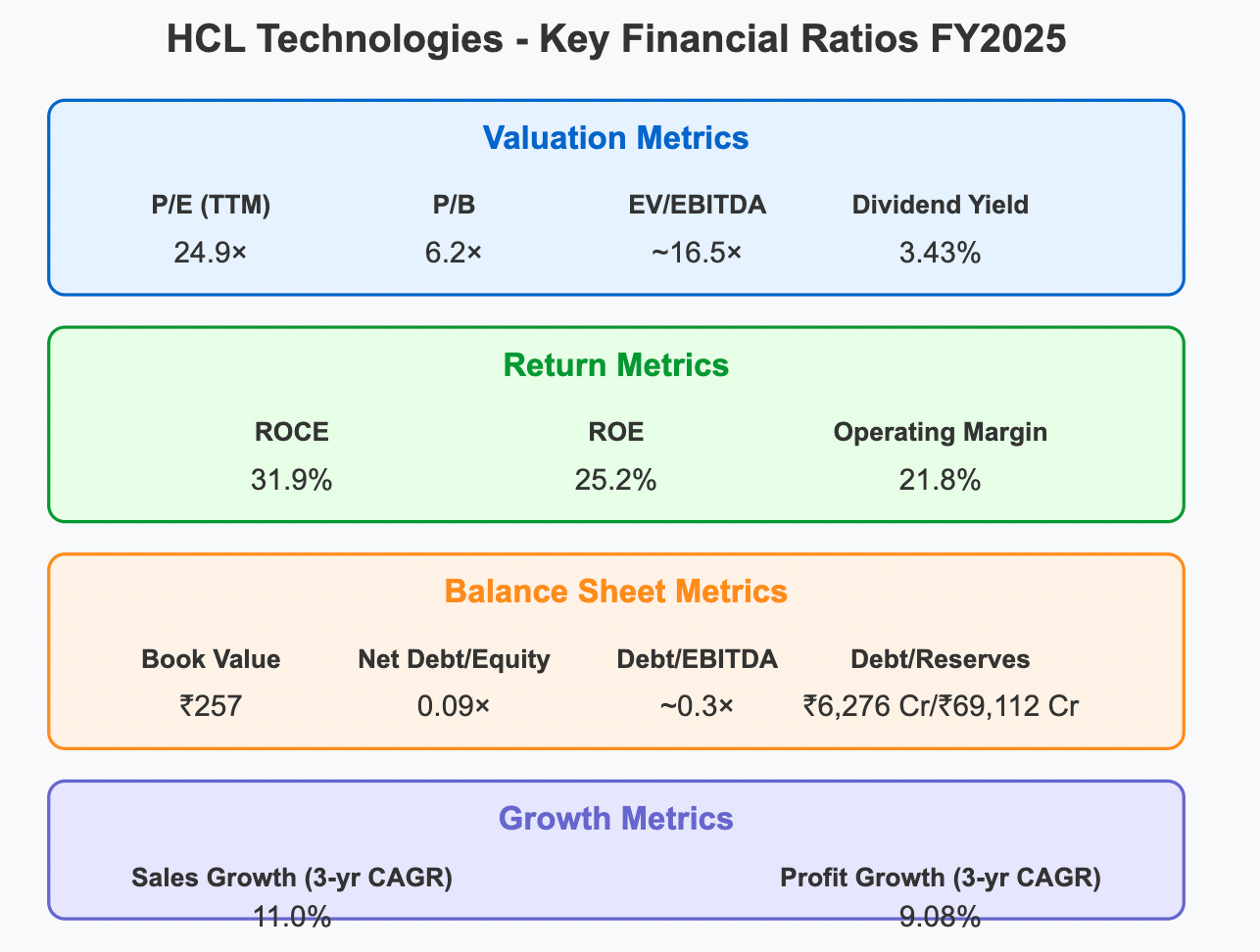

Key Metrics: Focus on P/E ratio (24.9×), ROCE (31.9%), and ROE (25.2%) demonstrates premium valuation compared to large-cap IT peers. Current dividend yield stands at 3.43%, supporting income investors.

CAPEX & Growth Strategy: The company invested ₹1,108 Cr in digital infrastructure, AI labs, and campus expansions, aligning with their strategy to strengthen digital and AI capabilities while diversifying talent pools globally.

Management Updates: Leadership continues to prioritize AI-driven solutions with the completion of HPE CTG asset acquisition to enhance edge-to-cloud engineering capabilities, particularly in Telecom and Media sectors.

Long-Term Projections: The company projects revenue to grow from ₹117,055 Cr in FY25 to ₹174,000 Cr by FY30 and ₹258,000 Cr by FY35. Profit after tax is expected to increase from ₹17,399 Cr to ₹28,000 Cr by FY30 and ₹44,000 Cr by FY35, driven by AI adoption and digital transformation services.

HCL Technologies Long-Term Growth Projections

Valuation: Currently trading at 24.9× P/E versus large-cap IT peer average of ~23-24×. The premium valuation is justified by superior ROCE (31.9%), robust cash flows, and promising growth pipeline in AI services.

Credit Agency Rating Changes: No rating changes were announced in FY25, with rating agencies continuing to assign "AA"/"AA-" long-term ratings, reflecting a stable credit profile.

Conclusion: HCLTech's Q4 FY25 performance demonstrates resilient growth, healthy margins, and world-class cash generation capabilities. With strategic AI investments, key acquisitions, and strong financial fundamentals, the stock presents an attractive mix of growth potential and dividend yield at current valuation levels.

Disclaimer: This report is for informational purposes only and does not constitute investment advice. Investment decisions should be based on individual risk tolerance and a thorough understanding of the company and market conditions.