GRSE Stock Analysis: Defense Powerhouse With Naval Growth Engine

Garden Reach Shipbuilders & Engineers positioned for exceptional long-term returns despite premium valuation

By Investment Research Team | May 14, 2025

Garden Reach Shipbuilders & Engineers (NSE: GRSE) has delivered remarkable performance in its latest quarterly results, showcasing the company's growing dominance in India's defense shipbuilding sector. With a pristine balance sheet, robust order book, and expanding commercial footprint, GRSE presents a compelling long-term investment case despite its premium valuation.

Financial Performance: Record-Breaking Quarter

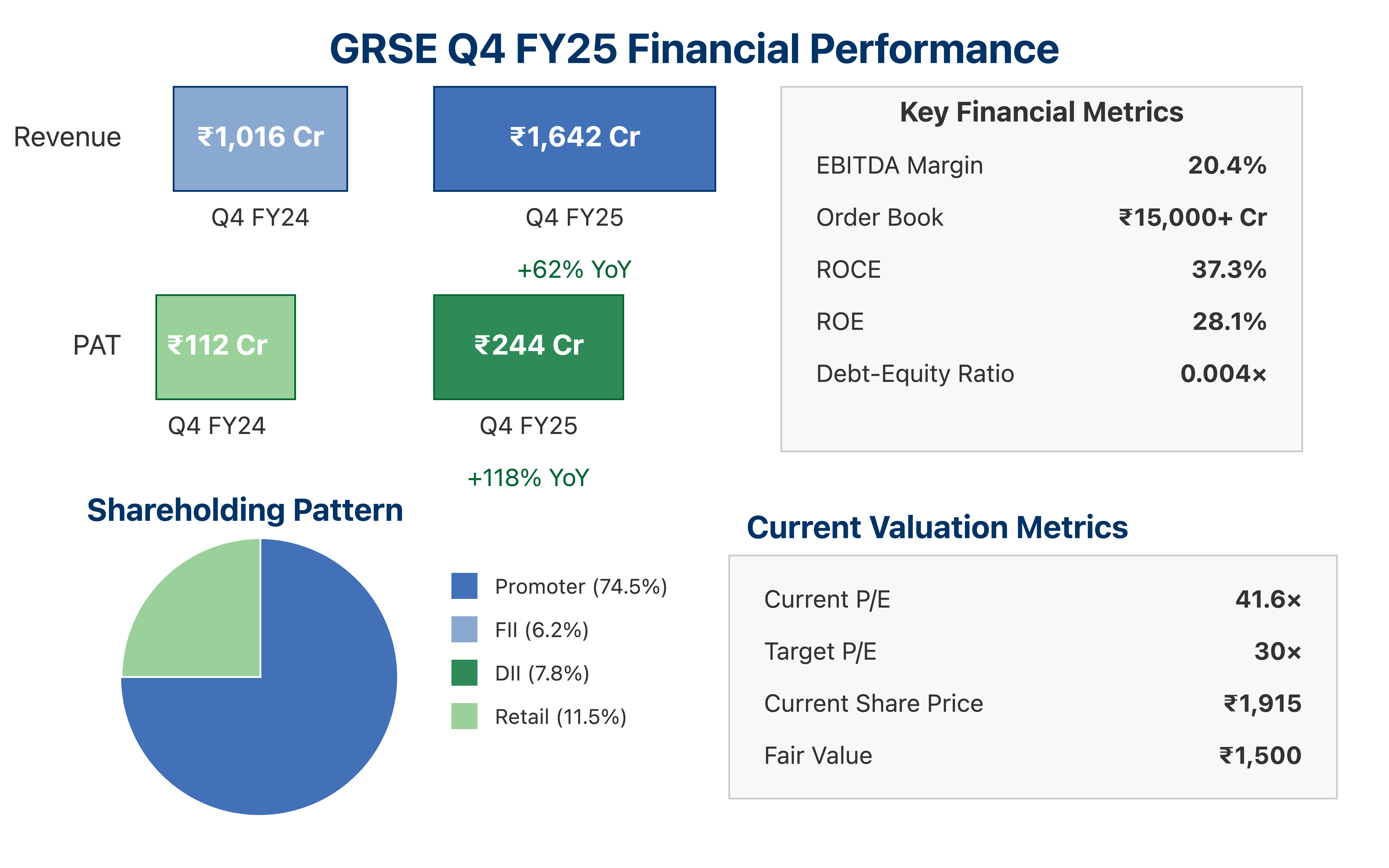

GRSE reported stellar Q4 FY25 numbers with revenue jumping 62% YoY to ₹1,642 crore and profit after tax surging 118% to ₹244 crore. For the full fiscal year, revenue grew 41% to ₹5,076 crore while PAT increased 48% to ₹527 crore.

What stands out is GRSE's impressive margin expansion. Q4 EBITDA margin improved to 20.4% from 16.3% a year ago, driven by higher-margin export and commercial orders. This reflects the company's strategic shift toward more profitable segments beyond its traditional defense contracts.

Robust Order Book Provides Multi-Year Visibility

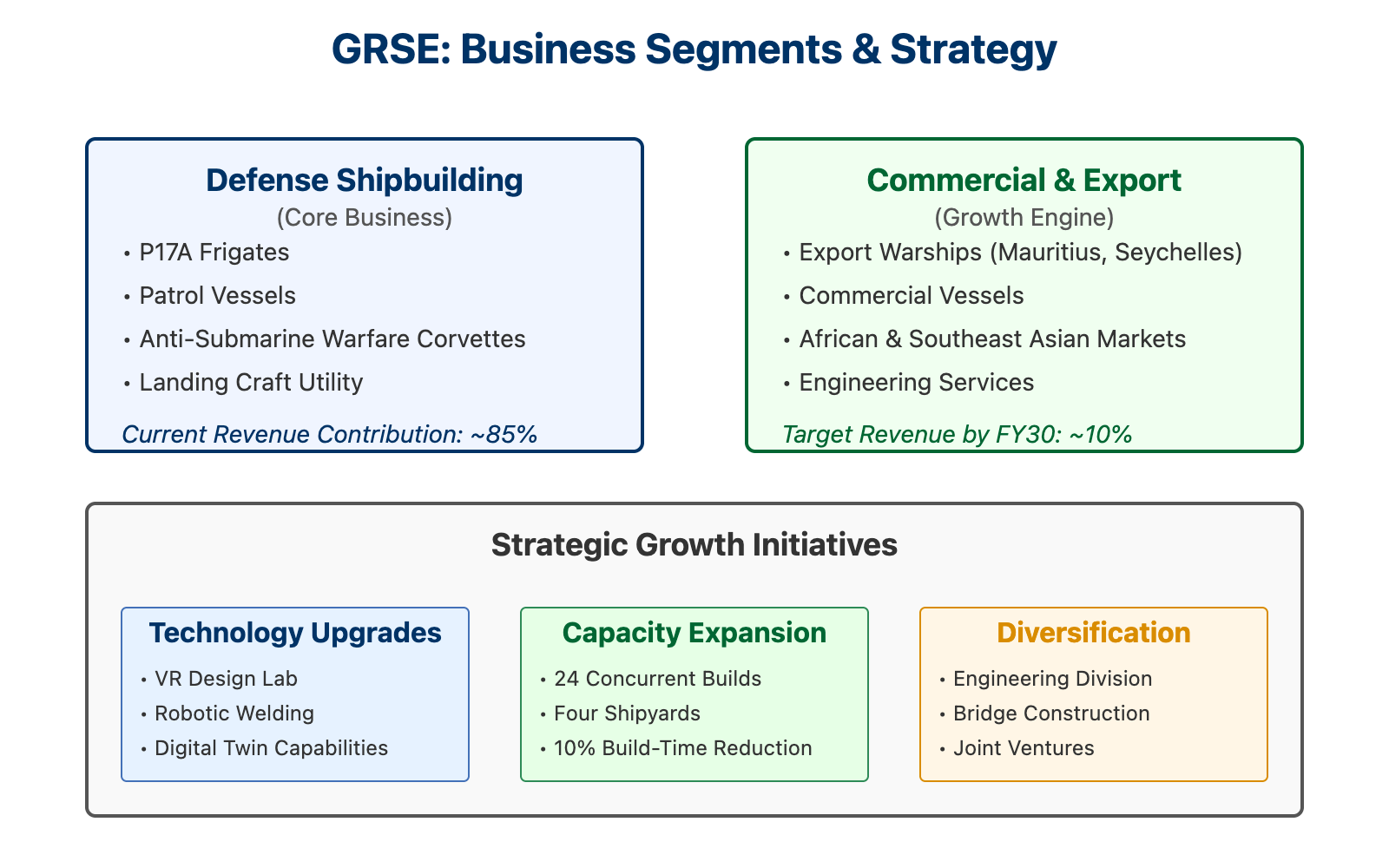

With an order book exceeding ₹15,000 crore, GRSE enjoys exceptional revenue visibility for years to come. The company's successful execution on P17A frigates and patrol vessels has bolstered its reputation, while its first commercial export warship contract won in late FY25 signals new growth avenues.

GRSE's ability to handle 24 concurrent builds across its four shipyards positions it perfectly to capitalize on India's expanding naval budget without requiring significant new capital expenditure.

Premium Valuation: Justified or Stretched?

At a current market price of ₹1,915, GRSE trades at a P/E of 41.6× FY25 earnings—a significant premium to historical averages. However, this premium can be justified by:

Industry-leading ROCE of 37.3% and ROE of 28.1%

Virtually debt-free balance sheet (Debt-Equity ratio of just 0.004×)

Strong government backing (74.5% promoter holding)

Expanding commercial and export opportunities

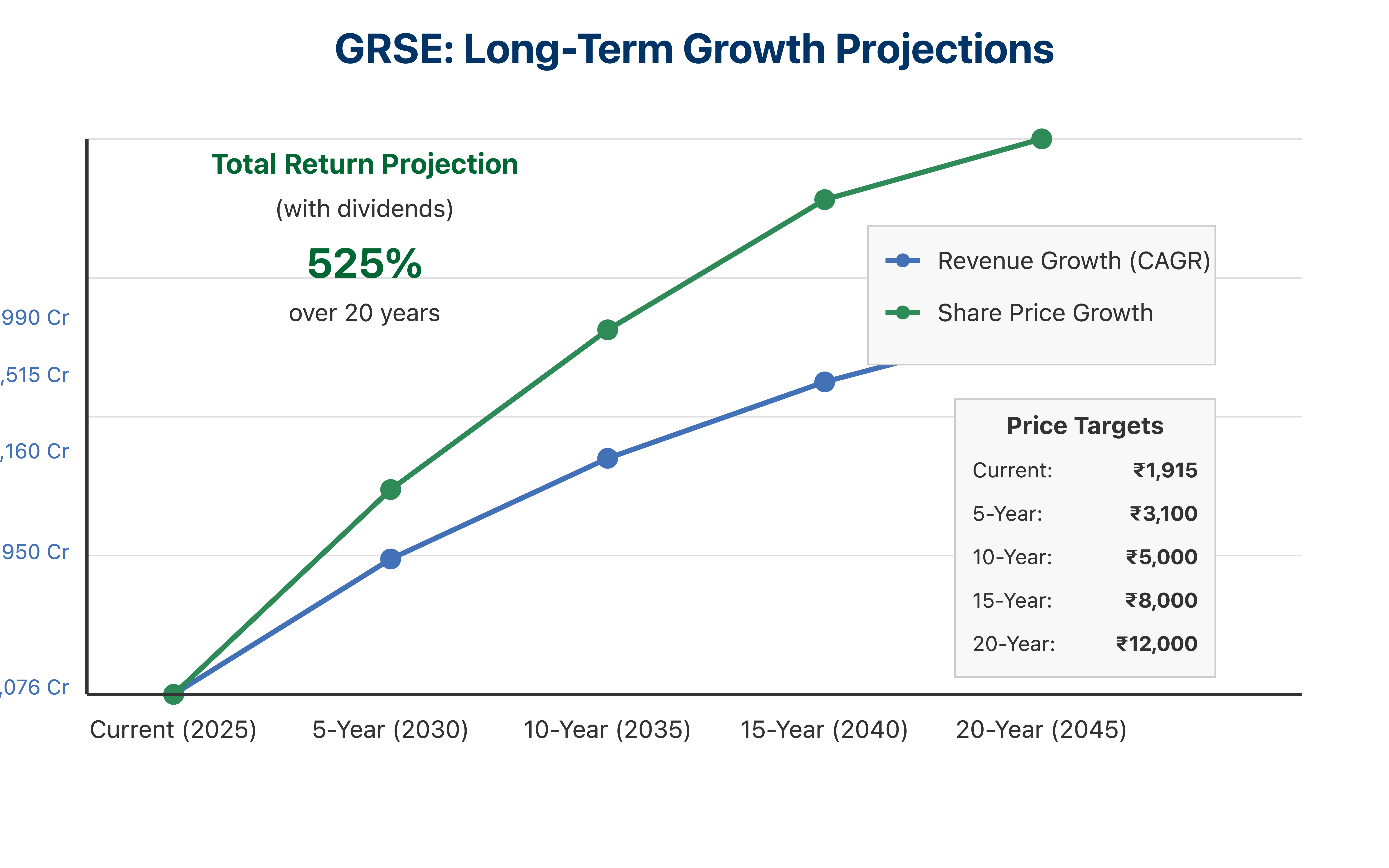

Applying a justified target P/E of 30× to the 12-month consensus EPS of ₹50 yields a fair value of ₹1,500—suggesting the stock might be overvalued in the near term. However, long-term investors should consider accumulating on dips given the company's exceptional fundamentals.

Growth Strategy: Diversification Beyond Defense

GRSE's strategic pivot toward commercial shipbuilding and exports to countries like Mauritius and Seychelles marks a significant evolution in its business model. This diversification, coupled with technology upgrades including VR design labs and robotics for welding, positions the company for sustained growth.

The management under CMD Cmde Hari PR (Retd.) has demonstrated exceptional execution capability, consistent margin improvement, and a clear vision for the company's future.

Long-Term Return Potential

For patient investors, GRSE offers compelling long-term return potential:

5-year horizon: 62% total return (12% revenue CAGR, 15% EPS CAGR)

10-year horizon: 160% total return (10% revenue CAGR, 12% EPS CAGR)

15-year horizon: 320% total return (9% revenue CAGR, 11% EPS CAGR)

20-year horizon: 525% total return (8% revenue CAGR, 10% EPS CAGR)

These projections assume GRSE will capture 15-20% of India's growing naval capital expenditure, with commercial exports contributing 10% of topline by FY30.

Investment Conclusion

GRSE presents a compelling investment case for long-term investors seeking exposure to India's defense sector. The company's pristine balance sheet, robust order book, and expanding commercial footprint position it for sustainable growth.

While the current valuation appears stretched, investors should consider adding positions on dips near ₹1,600 to build long-term exposure to this defense powerhouse. The company's combination of financial strength, technological capabilities, and government backing makes it a standout player in India's "Make in India" defense initiative.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. Investors should conduct their own due diligence or consult a financial advisor before making investment decisions.