GOODYEAR INDIA LIMITED NSE: GOODYEAR 2026

I. Investment Thesis & Summary

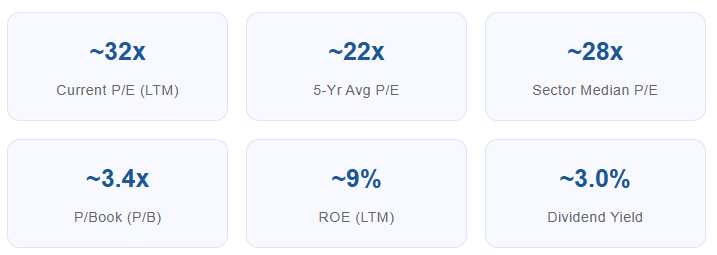

Let’s be direct about this one. You’re looking at a 60-plus-year-old tyre brand with American parentage, zero debt, and a stock that’s fallen roughly 25% from its 52-week peak of ₹1,071. Sounds interesting, right? The catch — earnings have been compressing hard. Net profit is down nearly 45% year-over-year in the latest quarter. Revenue isn’t growing. And yet, the stock isn’t dirt-cheap at around 32x trailing earnings.

This company sits on a clean balance sheet, pays decent dividends, and holds real leadership in the farm tyre segment — a market that’s directly tied to India’s rural economy recovery. The current pain is real, but the structural story isn’t broken. That’s why this is a Hold, not a Sell. If you own it, stay patient. If you’re looking to buy, wait for a better entry or clearer earnings recovery signals.

📌 The one-liner: The brand is solid, the balance sheet is clean, but the earnings are under pressure — the stock needs earnings to catch up before it becomes a compelling buy.

Youtube Link:

II. Business Model & Operations

The business is simple. This company makes and sells tyres, tubes, and flaps for cars, trucks, farms, and off-road applications under a globally recognized brand name. Two manufacturing plants — one in Ballabgarh (Haryana) and one in Aurangabad (Maharashtra) — handle production. The parent company, one of the world’s largest tyre manufacturers, holds a 74% stake and provides technology access and global brand heft.

The revenue mix is split across two key buckets: Farm Tyres (sold to OEMs and the replacement market) and Consumer Tyres (cars, SUVs, and increasingly EVs). Farm tyres are where this company punches hardest — it’s a market leader with strong OEM relationships. Consumer replacement is where management is actively repositioning toward the premium end, targeting luxury, SUV, and electric vehicle segments.

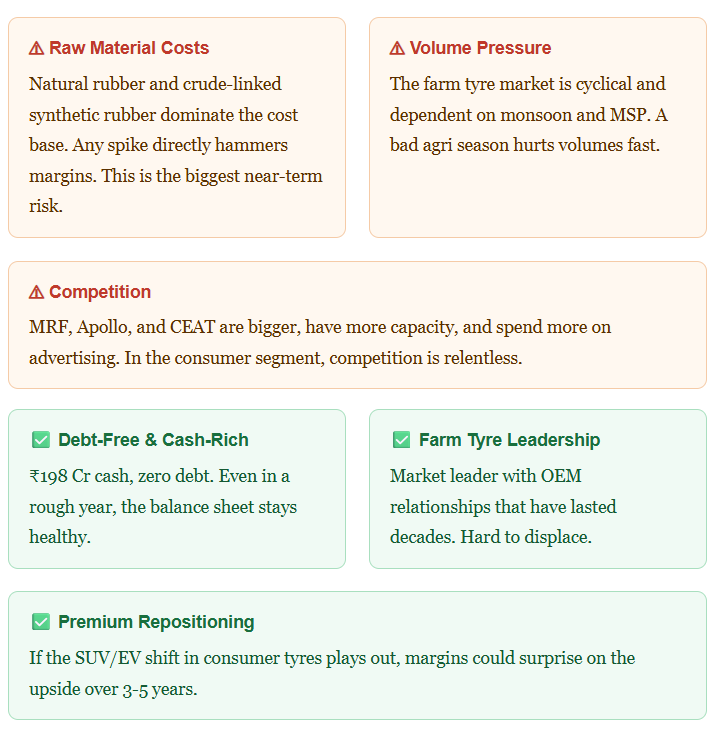

In the latest financial year, the company launched the Assurance Max Guard range of tyres for the passenger car segment — a push upmarket. The farm segment saw modest recovery after a demand downturn, aided by above-normal monsoons and higher Minimum Support Prices. Extended Producer Responsibility (EPR) rules for waste tyres introduced by the Environment Ministry created a one-time financial provision that hit profits in FY24 — that overhang is now largely behind us.

III. Historical Financial Review

The numbers tell a tough story. Revenue has declined roughly 8% per year over the last three years — an ugly 3-year CAGR of approximately -9%. FY23 was the peak year; since then, subdued demand, raw material cost swings, and volume pressures have eaten into both topline and margins. Operating profit margins have compressed from around 7.1% in FY23 to below 5% on a trailing basis. The latest reported quarter showed margins collapsing to just 4.3%.

Diluted EPS on a last-twelve-months basis sits at approximately ₹24.6 — well below FY23’s ₹53 and FY24’s ₹41. That’s a sharp contraction, and it explains why the stock is off its highs. The silver lining? The company is debt-free, held ₹198 Crore in cash as of September 2024, and generated positive operating cash flow even through the difficult period. Operating cash flow per share on a trailing basis is approximately ₹50-55, which is actually higher than reported EPS — that’s because working capital management has been decent and non-cash charges are elevated. Cash is healthy, even if accounting profits look weak.

Management paid ₹23.90 per share in dividends for FY25 — that’s real cash back to shareholders even during a tough year. Capex has been lean (about ₹40 Crore in FY24), reflecting a conservative approach while the market recovers.

IV. Fundamental Valuation & Investment Call

Let’s run through the numbers honestly.

At ₹802, the stock trades at roughly 32x trailing earnings — and that’s with compressed profits. That actually makes it more expensive than its historical average of around 22x. So no, this isn’t a screaming bargain on a P/E basis right now.

But wait — here’s where it gets nuanced. The earnings are cyclically depressed. If the company normalizes margins back to the FY23-FY24 range (say, 6-7% operating margins), you’d see EPS come back toward ₹35-40. At the historical average multiple of 22x, that implies a fair value of roughly ₹770-880. At a slightly more generous 25x (justified by brand, debt-free balance sheet, and parent support), fair value is around ₹875-1,000. Our 12-18 month target of ₹950 is based on normalized EPS of ~₹37 at 25-27x — achievable if farm demand stabilizes and consumer tyre volumes pick up.

ROE at 9% is underwhelming for a brand of this stature — it was 16-20% in better years. ROCE was 22.7% in FY24, now likely in the 12-15% range. Neither is alarming for a cyclical trough, but it confirms this isn’t a high-return business structurally. The 3% dividend yield provides some comfort while you wait.

V. Long-Term Outlook & Risk Assessment

Over a 5-10 year horizon, this stock can deliver 10-15% annualized returns — but it’s not a straight-line story. Here’s the bull case: India’s vehicle parc (total registered vehicles) keeps growing, rural farm mechanization trends are intact, and the company’s parent keeps investing in global product launches for Indian conditions. The EV segment is an emerging opportunity — Goodyear globally has EV-specific tyre lines, and the Indian arm stands to benefit from technology transfer as EV adoption accelerates.

Management has clearly articulated a premiumization play in consumer tyres — moving away from volume-competitive mid-market segments toward SUV, luxury, and EV. This is smart; margins are structurally better in premium. The farm segment OEM relationships are sticky — BEML, tractor OEMs, and agricultural equipment manufacturers depend on this company. That’s not easy to replace.

The promoter (the US parent) has held steady at 74% for years — they haven’t sold a single share. That’s a quiet but meaningful vote of confidence. And with ₹198 Crore in cash and zero debt, the company has the firepower to invest in capacity or return more cash to shareholders.

Simply put — this is a quality franchise going through an earnings trough. The stock isn’t cheap enough to be aggressive about, but the business fundamentals aren’t broken. Hold what you have, watch for margin recovery, and revisit this at the next set of quarterly results for signs of volume and margin improvement.

Expected 5-year return: 10–15% annualized (assuming earnings normalization from FY26 onward). Expected 10-year return: 12–18% annualized (if premiumization and EV tailwinds materialize meaningfully by early 2030s).

🙏🙏🙏🙏🙏🙏🙏🙏

❣️❣️❣️❣️❣️❣️❣️❣️

👍👍👍👍👍👍👍👍