Godfrey Phillips India: Premium Growth & Strong Returns in a Regulated Sector

Despite operating in a highly regulated industry, Godfrey Phillips India (GPI) continues to deliver exceptional shareholder value through strategic premiumization and disciplined capital allocation. The tobacco major's Q4 FY2025 results reveal a company executing flawlessly against headwinds, with clear visibility for long-term investors.

Q4 Performance Highlights: Robust Growth

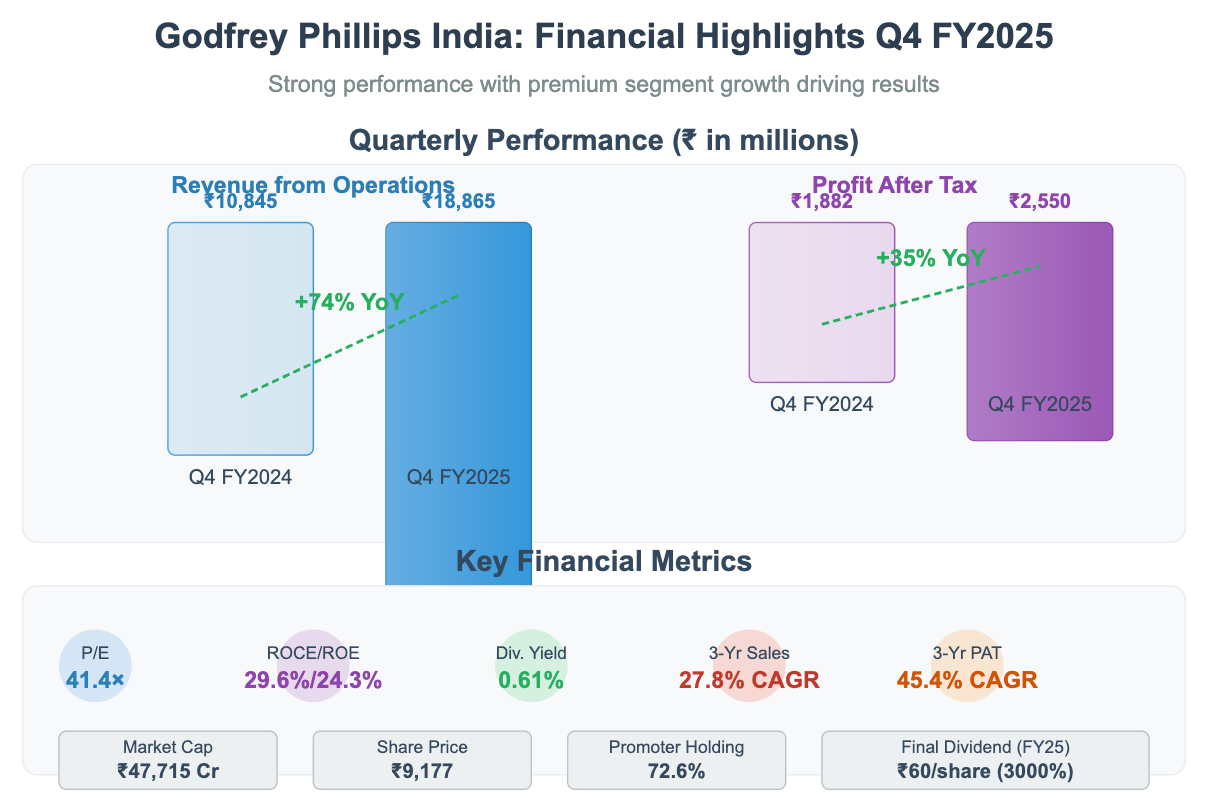

GPI delivered a stellar Q4 FY2025, with standalone revenue soaring 74% YoY to ₹18,865 million and profit after tax growing 35% YoY to ₹2,550 million. This performance stems from premium segment volume growth in the mid-teens, highlighting the company's successful premiumization strategy.

The company's operating profit margin remained robust at 21.0%, a slight decrease of 50 basis points compared to the same quarter last year. However, GPI's cost efficiency initiatives in raw material sourcing and operational leverage have helped contain costs despite excise duty inflation.

Valuation & Shareholder Returns

With a market capitalization of ₹47,715 crore and current share price of ₹9,177, GPI trades at a P/E multiple of 41.4×—a 15% premium to the domestic tobacco sector average. This premium valuation is justified by:

Superior ROIC of over 25% (vs. 18-20% for peers)

Consistent free cash flow generation of ₹15-18 billion annually

Robust balance sheet with marginal net debt of just ₹1.79 billion against reserves of ₹52.35 billion

Net-debt-to-EBITDA ratio below 0.1×

For FY2025, GPI has proposed a final dividend of ₹60 per share (3,000% on face value of ₹2), reflecting its strong cash generation capabilities. The company maintains a 30% payout ratio of PAT, with FY25 payout at approximately ₹13 billion including interim dividends.

Growth Strategy & Capital Allocation

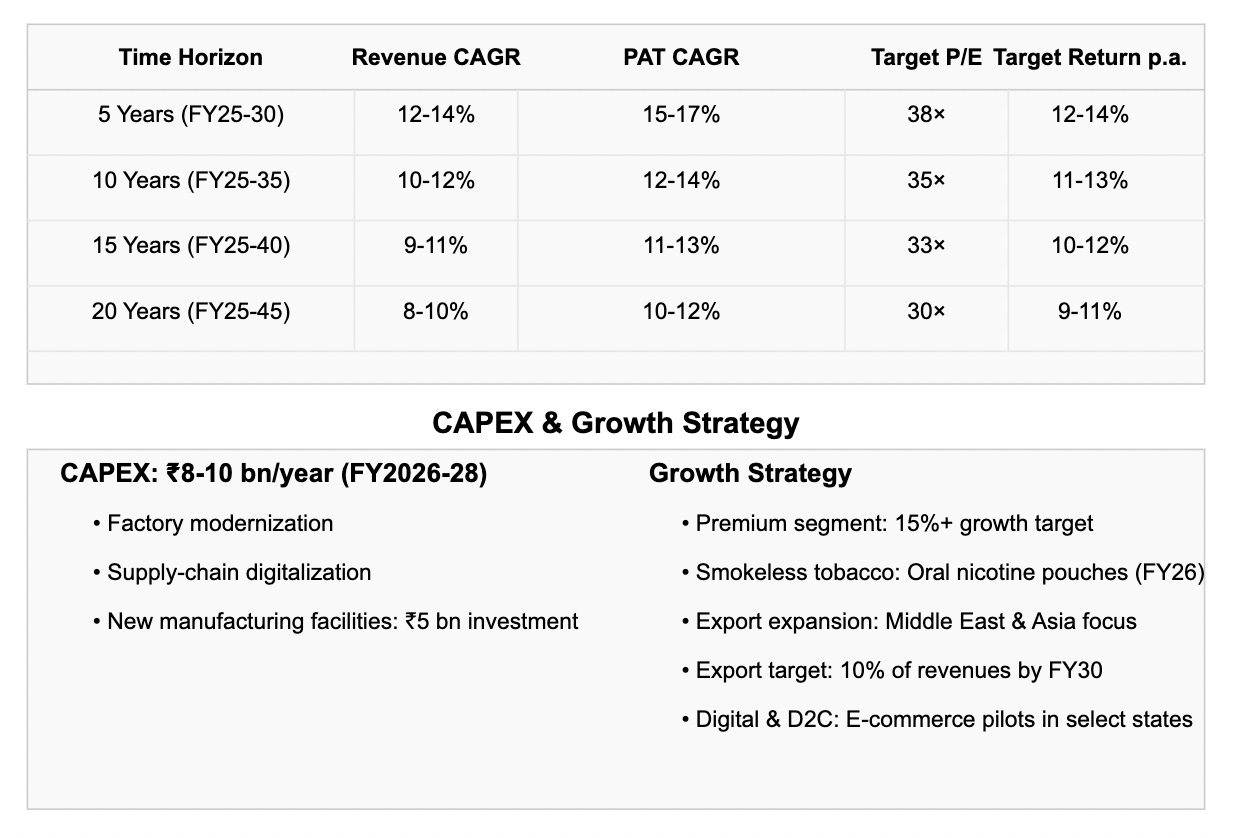

GPI plans CAPEX of ₹8-10 billion per year over FY2026-28, focusing on:

Factory modernization with emphasis on energy efficiency

Supply chain digitalization

New manufacturing facilities (₹5 billion allocated for greenfield sites in North and East India)

Product diversification into smokeless tobacco, including oral nicotine pouches launching in FY26

The company's strategic partnership with Philip Morris International provides access to global R&D capabilities and risk management practices, supporting its growth initiatives.

Long-Term Growth Projections

GPI has outlined ambitious yet achievable long-term growth targets:

5-year horizon (FY25-30): 12-14% revenue CAGR, 15-17% PAT CAGR, with target annual returns of 12-14%

10-year horizon (FY25-35): 10-12% revenue CAGR, 12-14% PAT CAGR, with target annual returns of 11-13%

20-year horizon (FY25-45): 8-10% revenue CAGR, 10-12% PAT CAGR, with target annual returns of 9-11%

These projections assume a stable regulatory environment and continued premiumization, with returns including dividend reinvestment.

Export Expansion & Digital Transformation

GPI is scaling up its Middle East exports through its DMCC hub, targeting 10% of group revenues from exports by FY30. Simultaneously, the company is piloting e-commerce for alternative products in select states, embracing digital transformation to reach consumers directly.

For investors seeking exposure to the consumer staples sector with defensive characteristics and growth potential, GPI offers a compelling investment case with its premium positioning, strong balance sheet, and clear roadmap for sustainable growth in a challenging industry landscape.