Equity Research Report: Britannia Industries Ltd (India)

Date: May 8, 2026

Rating: BUY. Target Price: 7050.00 INR (12-Month Horizon

Executive Summary

Britannia Industries Ltd. (BIL) is poised for sustained growth driven by robust brand equity, premiumization trends, and strategic diversification. Recent performance indicates strong revenue and profit resilience. Our BUY recommendation, supported by a target price of 7050.00 INR, reflects an attractive 27.5% implied upside. We anticipate continued market share gains and margin expansion, making BIL a core holding in the Indian consumer staples space.

1. Investment Thesis & Summary

Britannia Industries Ltd. is a dominant player in India’s fast-growing biscuits and bakery market, boasting an unparalleled brand portfolio and extensive distribution network. Our investment thesis is anchored in its ability to consistently leverage its strong brand recall for premiumization, capitalize on evolving consumer preferences towards healthier and value-added products, and expand its reach into adjacent categories and new geographies. The company’s ongoing focus on operational efficiency, prudent cost management, and innovation positions it favorably to navigate competitive pressures and deliver sustainable, profitable growth. We believe BIL’s management execution, coupled with favorable demographic and economic tailwinds in India, will drive superior shareholder returns.

2. Key Financial Highlights

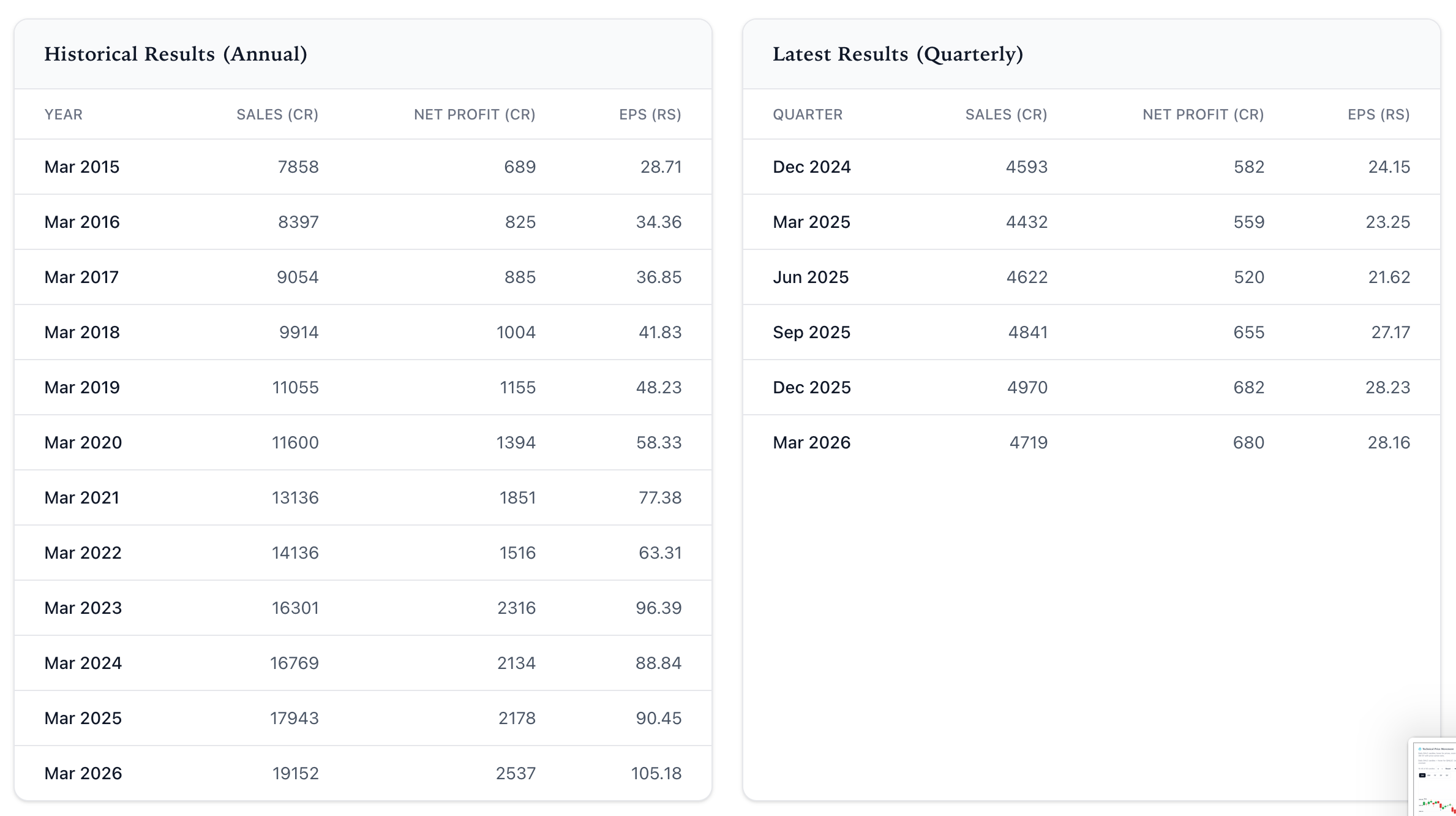

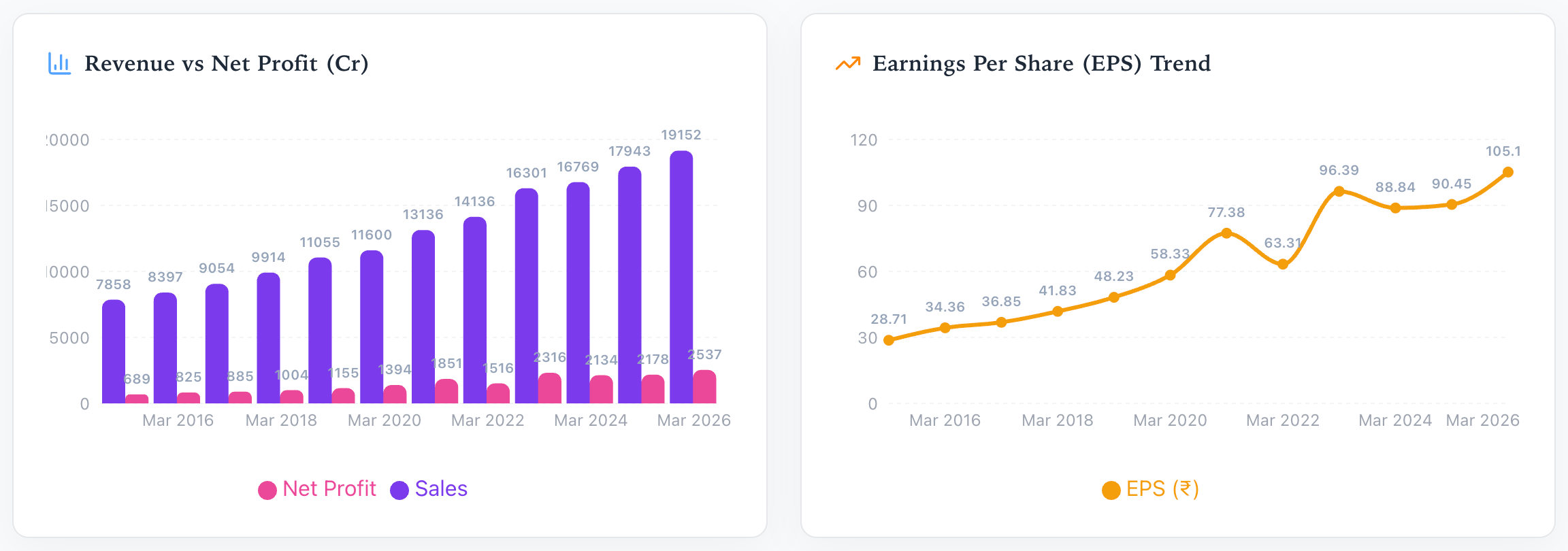

Britannia Industries has demonstrated a consistent upward trajectory in revenue and profitability over the past decade.

Annual Performance (INR Crores): Recent Quarterly Performance (Last 4 Quarters, INR Crores):

The latest annual results for FY26 show a healthy revenue growth of ~7.3% and a significant profit jump of ~16.4%, indicating improved operating leverage and margin expansion. The quarterly performance for FY26 remained robust, with consistent sales growth and strong net profit generation, particularly in Q2 and Q3 FY26. Q4 FY26, while showing a slight sequential dip in sales, maintained strong profitability, suggesting effective cost controls and stable pricing power.

3. Top 3 Catalysts

Premiumization and Portfolio Expansion: BIL’s ongoing shift towards higher-margin premium products, coupled with its expansion into dairy, cakes, and healthy snacks, is a significant growth driver. The company’s ability to capture discretionary spending through innovative product launches and refreshed branding will continue to boost Average Realization Value (ARV) and profitability.

Distribution Network Enhancement and Rural Penetration: Continued investment in deepening its distribution reach, especially in rural and semi-urban areas, will unlock access to a larger consumer base. Initiatives like expanding its direct distribution reach and leveraging modern trade channels will solidify its market dominance.

Operational Efficiencies and Cost Management: The company’s sustained focus on optimizing its supply chain, manufacturing processes, and procurement strategies is expected to yield margin expansion. This, combined with prudent price-hike strategies, will help mitigate inflationary pressures and enhance profitability.

4. Top 3 Risks

Intensifying Competition: The Indian biscuit and bakery market is highly competitive, with both organized and unorganized players vying for market share. Aggressive pricing strategies from competitors or the emergence of disruptive new entrants could impact BIL’s market share and pricing power.

Input Cost Volatility: Raw material prices, particularly for wheat, sugar, and palm oil, are subject to global and domestic market fluctuations. Adverse movements in these input costs can pressure margins if not effectively passed on to consumers.

Regulatory and Policy Changes: Any adverse changes in food safety regulations, taxation policies, or government incentives related to the FMCG sector could impact operational costs and profitability.

5. Valuation View

We value Britannia Industries Ltd. using a Discounted Cash Flow (DCF) approach and a P/E multiple.

Our DCF model projects revenue to grow at a CAGR of approximately 8% over the next five years, driven by market penetration and product innovation. We assume a gradual improvement in EBITDA margins to ~20% by FY31, supported by operating efficiencies and premiumization. Our terminal growth rate is set at 3.5%.

For a P/E multiple-based valuation, we consider a peer group average and historical multiples, factoring in BIL’s market leadership and growth prospects. Based on FY27 estimated EPS of INR 115.00 and a target P/E multiple of 61.3x (a slight premium reflecting sustained leadership and growth), we arrive at our 12-month target price.

Implied upside = ((7050.00 - 5530.00) / 5530.00) * 100 = 27.5%

6. Actionable Takeaway

Britannia Industries Ltd. presents a compelling investment opportunity with strong brand equity, a robust growth trajectory, and improving profitability. The company’s strategic initiatives are well-aligned with evolving consumer trends and market dynamics. The projected 27.5% upside to our 12-month target price of INR 7050.00, driven by sustained premiumization, operational efficiencies, and market expansion, supports a BUY recommendation. We believe BIL is positioned to deliver attractive risk-adjusted returns.