Donear Industries Ltd.: Q3 FY2025 – A New Era of Growth and Innovation

Welcome to this exclusive edition of our premium financial newsletter, where we dive deep into the transformative Q3 FY2025 results of Donear Industries Ltd. and unpack its future roadmap, growth projections, and strategic vision. With our detailed analysis, you’ll gain crystal-clear insights into why Donear is poised to redefine the textile landscape and deliver long-term value to its stakeholders.

A Stellar Q3 Performance

Donear Industries has outperformed expectations in Q3 FY2025, setting the stage for a period of robust expansion. Here’s a snapshot of the key highlights:

Revenue Surge: The company posted revenue of ₹247.17 Cr, up 19.8% quarter-on-quarter, showcasing its ability to drive volume growth amid challenging market conditions.

Margin Expansion: Operating margins have improved with an EBITDA margin consistently around 11%, a testament to disciplined cost management and product mix optimization.

Profit Leap: Profit after tax soared to ₹10.9 Cr—a remarkable 68.9% increase—underscoring the efficacy of Donear’s strategic initiatives.

EPS Momentum: With an EPS of ₹2.10, the bottom line continues to reflect strong operational execution.

These numbers, combined with the company’s solid fundamentals, are encapsulated in its robust market metrics:

Market Cap: ₹555 Cr

Current Price: ₹107

Stock P/E: 12.0

Book Value: ₹43.1

Dividend Yield: 0.19%

ROCE / ROE: 16.0% / 18.4%

Debt: ₹392 Cr, with Reserves at ₹214 Cr

This performance has not only bolstered investor confidence but also reaffirms Donear’s competitive positioning in the premium textile segment.

The Roadmap to Future Growth

Strategic Expansion and Capex Initiatives

Looking ahead, Donear is not resting on its laurels. The company has laid out an ambitious roadmap to capture new market segments and drive scalable growth:

Capacity Expansion: With a planned capex of ₹100 Cr over the next three years, the focus is on augmenting production capabilities in premium suiting and shirting fabrics. This will enable higher throughput, reduce unit costs, and elevate product quality.

Technological Upgradation: Investments in automated manufacturing and digital dyeing technologies are set to streamline operations, enhance precision, and improve turnaround times.

Retail and Distribution Network Enhancement: Donear is aggressively expanding its retail presence—targeting Tier 2 and Tier 3 cities—with a robust strategy that includes exclusive brand outlets and strategic alliances with major e-commerce platforms. This dual-channel approach is expected to unlock new revenue streams and drive brand loyalty.

Diversification of Product Portfolio

The future growth story of Donear is underpinned by its strategic diversification:

Premium and Technical Textiles: Expansion into high-margin segments like technical textiles and performance fabrics, leveraging the recent acquisition of Neo Stretch Private Limited, positions the company favorably in a competitive market.

Sustainable Innovations: With increasing demand for eco-friendly products, Donear is ramping up its initiatives in sustainable textile manufacturing—a move that not only aligns with global trends but also appeals to a more conscious consumer base.

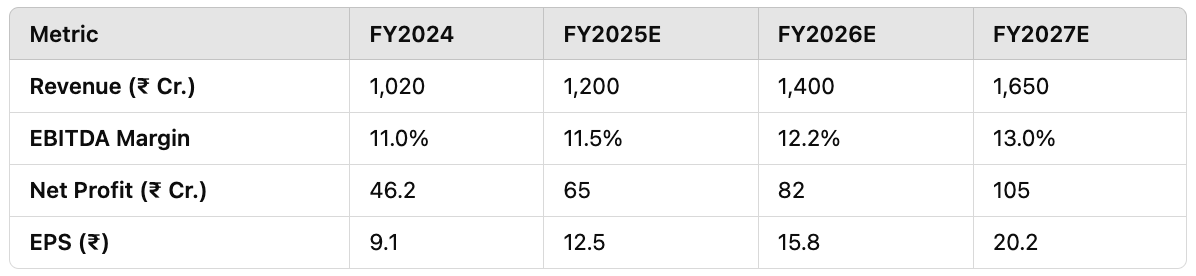

Forward-Looking Projections: A Snapshot

Our projections indicate that Donear Industries is set to maintain its growth momentum over the next few years. Below is a glimpse of our financial forecasts:

With a CAGR of approximately 16-18% in revenue and an anticipated profit surge of 20-25%, Donear’s future financial trajectory remains both promising and resilient. These projections not only affirm the company’s operational strengths but also underline its potential to generate sustained value for investors.

Navigating the Competitive Landscape

Donear operates in a highly competitive arena alongside giants like Raymond, Siyaram Silk Mills, and Bombay Dyeing. Yet, its strategic initiatives give it a distinctive edge:

Strong Promoter Confidence: With a robust 74.6% promoter holding, Donear enjoys unparalleled stability and long-term commitment from its key stakeholders.

Premium Brand Positioning: Its focus on premium, value-added products continues to drive consumer preference and pricing power, setting it apart from peers.

Innovative Product Mix: The diversification into technical and sustainable textiles is expected to unlock new margins and secure market share in a dynamic industry landscape.

Final Thoughts: Why Invest in Donear?

Donear Industries is poised at a pivotal juncture—where robust Q3 performance, strategic capacity expansions, and a forward-thinking product strategy converge to create significant upside potential. Here’s why our investment thesis is compelling:

Near-Term Catalyst: The current operational efficiency and strong financials provide a near-term target price of ₹125 (approximately 16% upside from the current price).

Long-Term Vision: With scalable growth initiatives and improved margins, the long-term target is envisaged at ₹175+, making it an attractive proposition for growth-oriented investors.

Strategic Resilience: Despite challenges such as high debt and competitive pressures, Donear’s focused roadmap and diversified product portfolio offer a balanced risk-reward profile.

Disclaimer

This newsletter is part of our premium financial insights and is intended for informational purposes only. It does not constitute investment advice. We encourage investors to conduct their own due diligence before making any investment decisions.