Data Patterns: Debt-Free Defence Stock With 32% Growth - But Is 62 P/E Too Steep?

SECTION I: Investment Thesis & Summary

Here’s a defence electronics play that’s been quietly building something special. Trading at ₹2,776 with a market cap of ₹15,541 Crores, this stock’s got a target price of ₹3,850 - that’s a solid 39% upside from here. BUY.

Why? The company’s sitting on an order book of ₹1,868 Crores (that’s 2.6 times their last year’s revenue), they’re completely debt-free, and they just reported their highest-ever quarterly revenue. Meanwhile, the stock’s trading at a P/E of 62 when they’re growing profits at 32% annually. The math works - the market’s underpricing their execution ability.

SECTION II: Business Model & Operations

This isn’t your typical defence contractor - they’re what’s called a vertically integrated electronics solutions provider. What does that mean? They design, develop, and manufacture the brains of India’s defence systems. Everything from radar electronics for fighter jets to missile guidance systems to satellite components. They’ve been at it for over 35 years.

Their products go into the LCA Tejas, BrahMos missiles, Light Utility Helicopters, and ISRO’s satellite programs. Think of them as the company that builds the electronic nervous system for India’s defence hardware.

Here’s what makes them different: most defence companies assemble imported components. These guys build everything in-house - from circuit boards to complete radar systems. That’s the “vertically integrated” part, and it gives them fat margins because they’re not paying middlemen.

The recent wins are telling. In the last nine months, they’ve pulled in ₹580 Crores in revenue - up 87% from the same period last year. They’re expanding capacity, hiring aggressively (they’ve added over 200 engineers in the last year), and moving from being a component supplier to a full systems integrator. That’s where the real money is.

Youtube Link:

SECTION III: Historical Financial Review

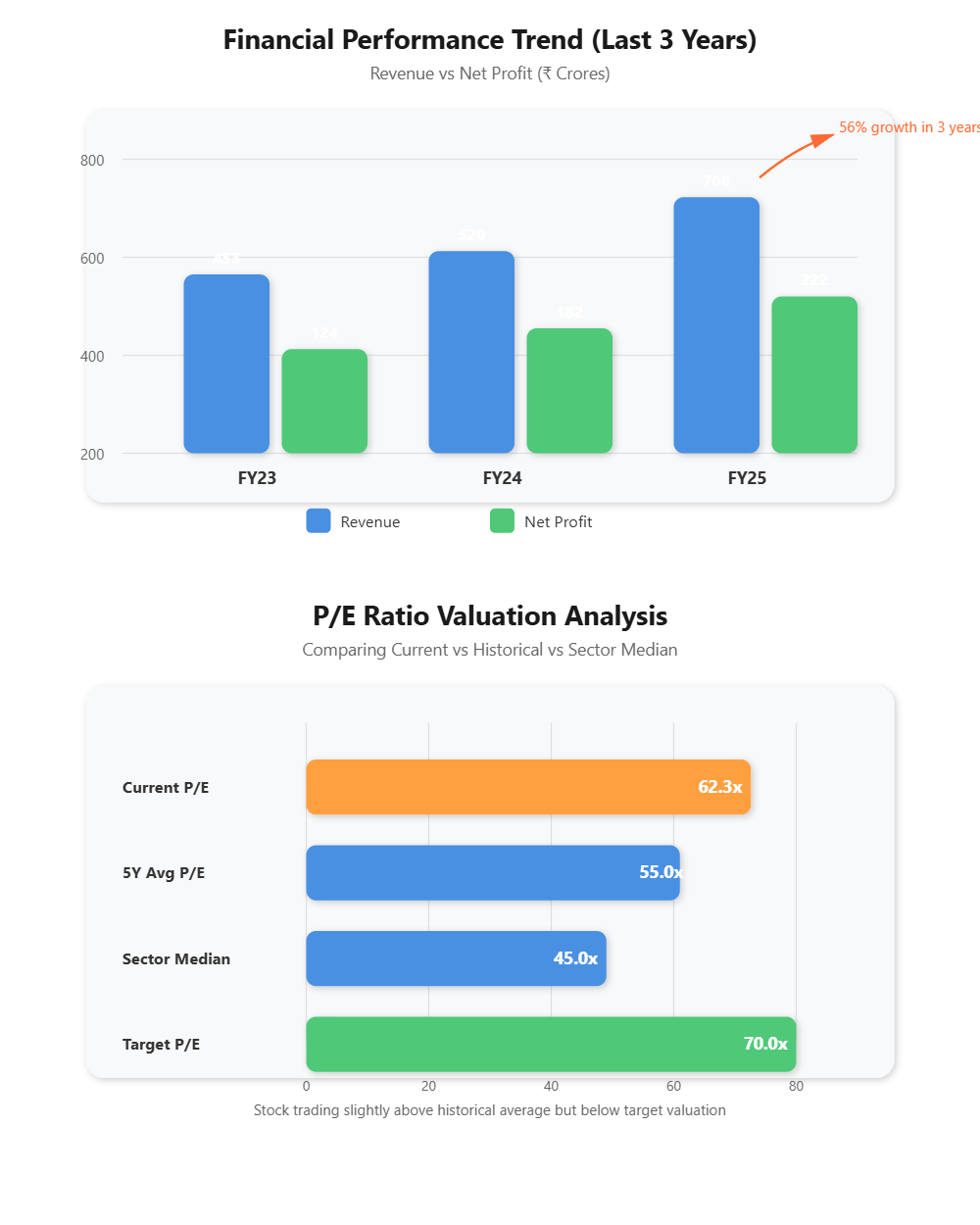

Let’s talk numbers. Over the last three years, revenue grew from ₹453 Crores to ₹708 Crores - that’s a 32% compound annual growth rate. Not bad, but here’s the kicker: net profit grew at the same 32% pace, from ₹124 Crores to ₹222 Crores. That means they’re growing without sacrificing profitability.

The latest twelve months? Revenue hit ₹976 Crores with net profit of ₹247 Crores. Earnings per share came in at ₹44.13, up from ₹22.15 three years ago. They’ve doubled their EPS while keeping margins healthy.

Cash flow tells the real story. The company generated ₹139 Crores in operating cash in FY24 before hitting some working capital issues in FY25 (₹90 Crores outflow - mostly because defence projects have lumpy payment cycles). But here’s the thing: they’re debt-free with ₹327 Crores sitting in investments. Zero financial stress.

The working capital situation needs watching. Debtor days are at 307 - that’s ten months of receivables sitting on the books. It’s not unusual for defence contractors (government payments are slow), but it ties up cash. Inventory days at 421 reflect the long project cycles. The complete cash conversion cycle runs 618 days. That’s the nature of the business, but it means they need deep pockets. Good thing they have them.

SECTION IV: Fundamental Valuation Metrics & Investment Call

The stock’s trading at 62.3 times earnings. Expensive? Let’s dig in.

Their five-year average P/E is around 55, so we’re slightly above historical norms. But consider this: revenue growth is accelerating (97% TTM growth), margins are expanding (from 38% OPM in FY23 to 39% in FY25), and the order book just hit an all-time high.

Price-to-book is 10.1 times - that’s rich by traditional standards, but ROE of 15.2% and ROCE of 21% justify some premium. They’re earning well above their cost of capital.

The dividend yield is tiny at 0.28% (₹7.90 per share), but they’re paying out 20% of profits consistently. Management’s reinvesting the rest into capacity expansion, which makes sense given their growth runway.

Here’s the valuation case: if they maintain 25% revenue growth (below their historical 32%) and keep EBITDA margins at 37%, they’ll hit ₹250 Crores in annual profit within two years. At a 40 P/E (sector median), that’s a ₹10,000 Crore market cap or ₹1,785 per share in incremental value. Add the current ₹2,776 and you’re looking at ₹4,000+ in 24 months.

Even at a conservative 35 P/E, the stock should trade at ₹3,500 today. Current price of ₹2,776 offers a 26% margin of safety.

SECTION V: Long-Term Outlook & Risk Assessment

Over the next 5-10 years, expect 15-20% annualized returns if everything goes right. Here’s why: India’s defence budget is growing at 9.5% annually (₹6.81 lakh Crores for FY26), and the government’s pushing “Make in India” hard. They’ve announced phased import bans on hundreds of defence items - that’s free demand creation for domestic players.

The company’s order book of ₹1,868 Crores gives visibility for the next 2.5 years. They’re targeting 20-25% revenue growth, which seems achievable. Management’s investing ₹200+ Crores in new manufacturing facilities and R&D. They’re also co-developing products with foreign defence majors for export markets - that’s a game-changer if they crack it.

Promoters hold 42.41% - stable for three years. No pledging, no selling. That’s confidence.

Now the risks - and there are real ones:

Revenue lumpiness: Defence projects don’t flow smoothly. They had ₹307 Crores revenue in Q2, then ₹173 Crores in Q3. It’ll bounce around quarter-to-quarter based on delivery milestones.

Margin pressure: The recent quarters showed margins compressing from 46% to 45% (Q3). That’s because they took on some lower-margin contracts to build relationships. If this becomes a trend, watch out.

Execution risk: They’re transforming from a niche electronics maker to a systems integrator. That requires different skills, more capital, and bigger projects. Can they pull it off? The jury’s still out.

Customer concentration: They’re heavily dependent on government defence programs. If budget allocations shift or programs get delayed (happens often in defence), revenue takes a hit.

Valuation risk: At 62 P/E, there’s no room for error. One bad quarter and the stock could crack 20-30%.

The India defence story is strong - geopolitical tensions, border security needs, import substitution, and a government committed to building indigenous capability. This sector’s got a 10-year tailwind.

This specific company is riding that wave well. They’ve got the technology, the order book, and the balance sheet. The valuation’s stretched, but not insane given the growth. If they execute on their ₹1,868 Crore order book and keep winning new contracts, this stock works at current levels.

The play here: buy on dips below ₹2,500, hold for 3-5 years, and watch for any margin compression or order book growth slowing down. Those are your exit signals.

[COMPANY NAME DISCLOSURE MARKER]

Data Patterns (India) Ltd - NSE: DATAPATTNS | BSE: 543428