Cyient Limited: Engineering Intelligence at Global Scale

SECTION I: Investment Thesis & Summary

This is a niche engineering and technology services company that’s been quietly building a serious moat in aerospace, defense, and digital engineering. The market’s been distracted by the large-cap IT noise, and this mid-cap gem is sitting at a price that doesn’t reflect where this business is heading. Simply put — the earnings are growing, the order book is filling up, and the stock hasn’t kept pace.

SECTION II: Business Model & Operations

Let’s talk about what this company actually does. They’re not your typical software services shop. Think engineering R&D, product design, and digital transformation — but for industries where getting it wrong means planes fall out of the sky or power grids go dark. Their clients are global OEMs and tier-1 suppliers in aerospace, communications, utilities, transportation, and mining.

The business runs on two primary legs. First, the services segment — which is the core engine — where they provide engineering design, embedded systems, digital transformation, and data analytics to global clients. This chunk is high-margin and sticky; once you’re embedded in a client’s product development cycle, switching you out is painful and expensive.

Second, their manufacturing arm — DLM (Design-Led Manufacturing) — takes the design work and translates it into physical, manufactured electronic systems. This is a newer business line but one with serious long-term optionality, especially as India’s defense and aerospace manufacturing push accelerates under government procurement policy changes.

Recently, they’ve been aggressively growing their aerospace and defense vertical, which now accounts for a meaningful share of revenue. They’ve also been expanding digital engineering capabilities — essentially helping legacy industrial clients modernize their products with IoT, AI, and data systems. That’s where the premium billing rates live, and that’s where they’re consciously pushing their revenue mix.

Youtube Link:

SECTION III: Historical Financial Review

The numbers here tell a solid story.

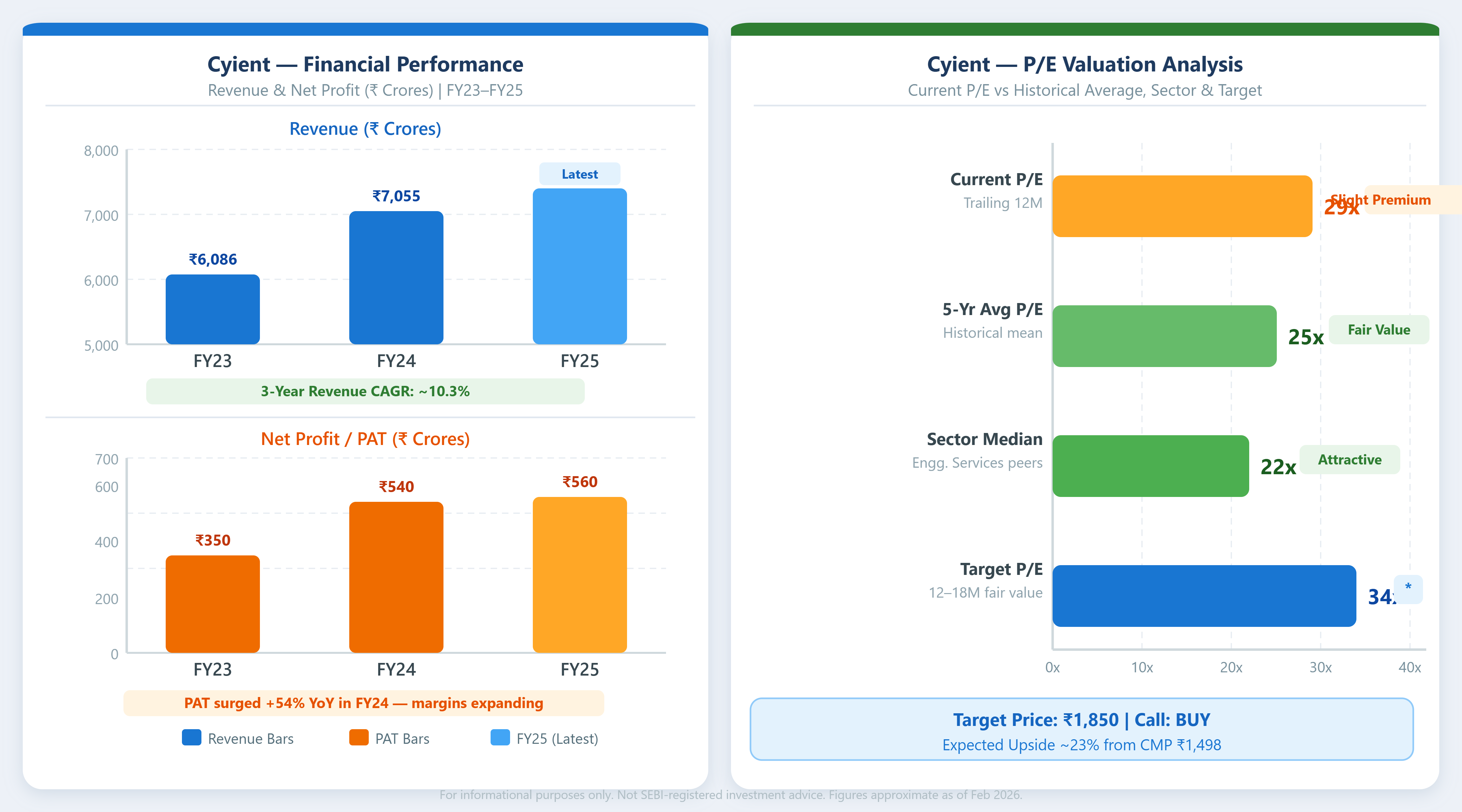

Revenue has grown from ₹6,086 Crores in FY23 to approximately ₹7,055 Crores in FY24, and early FY25 quarterly runs suggest the full-year number lands around ₹7,400 Crores. That’s roughly a 10–11% CAGR over three years — not explosive, but very consistent for a business that operates in long-cycle engineering contracts. These aren’t flashy one-quarter spikes; this is durable, sticky revenue.

Profitability tells an even better story. Net profit jumped from around ₹350 Crores in FY23 to approximately ₹540 Crores in FY24 — that’s a 54% jump in PAT in a single year. A big chunk of that came from margin improvement as they moved up the value chain and the services mix shifted toward higher-margin digital engineering work. LTM Diluted EPS sits around ₹49–51, and operating cash flow per share is healthy at approximately ₹60+, which means the earnings are real — cash is actually coming in the door, not just showing up on paper.

Debt?

Minimal. This business runs lean. The balance sheet carries negligible net debt, and the cash generation is strong enough to fund their capex and growth investments comfortably. Management hasn’t been reckless with the balance sheet — they’ve kept leverage tight while growing the business organically and through small, targeted acquisitions.

One thing worth noting: FY24 benefited from some DLM order execution acceleration and a strong recovery in the aerospace supply chain post-COVID normalization. That tailwind is partially structural and partially cyclical. The base is now higher, so FY25 growth looks more modest in percentage terms — but the absolute profitability trajectory is intact.

SECTION IV: Fundamental Valuation Metrics & Investment Call

Let’s look at the numbers plainly.

P/E Ratio — Around 29x on trailing earnings. Their own 5-year average P/E is closer to 24–26x. So the stock’s at a slight premium to its own history right now. But here’s the nuance — the business mix has genuinely improved, margins are structurally higher, and the addressable market in aerospace/defense engineering is expanding. A premium to historical P/E is arguably deserved. At 30–32x on FY26E EPS of ~₹55–58, you get to ₹1,650–1,850 easily.

P/B Ratio — Approximately 4.8x. Not cheap on an asset basis, but engineering services companies don’t need massive asset bases. What you’re paying for is IP, client relationships, and talent — and this company has all three in abundance.

ROE — ~16–17%. Decent. Not market-leading, but solid and improving. Three years ago this was 13–14%. The improvement is real and driven by better asset utilization and margin expansion, not financial engineering.

ROCE — ~18–19%. This is the cleaner metric here since debt is minimal. ROCE above 15% consistently means the business earns more than its cost of capital — that’s the definition of value creation.

EPS Growth — FY23 to FY24 was exceptional. FY25 and FY26 growth will be more normalized at 10–15% annually, but that’s perfectly fine at current valuations.

Dividend Yield — About 1.4–1.6%. Not a high-yield story. They pay a steady dividend but aren’t distributing large chunks of cash. Most of the excess cash gets reinvested — which is the right call given the growth opportunities ahead.

The call: At ₹1,498, you’re not getting a deep value bargain — but you’re buying a quality engineering services business with improving margins, strong order visibility, and a structural tailwind in aerospace and defense at a reasonable price. The risk/reward skews positive. Target of ₹1,850 over 12–18 months implies ~23% upside — that’s before dividends.

SECTION V: Long-Term Outlook & Risk Assessment

Over a 5–10 year horizon, this is one of the cleaner compounding stories in Indian mid-cap IT/engineering services.

Here’s why: Global aerospace is in a prolonged upcycle. Airbus and Boeing have backlogs stretching 8–10 years. Every new aircraft program needs massive engineering content — design, systems integration, embedded software. This company sits right in the middle of that supply chain, with deep relationships with tier-1 aerospace suppliers. That’s not going away.

The defense angle gets more interesting domestically. India’s push for Atmanirbhar Bharat in defense manufacturing is creating opportunities that didn’t exist five years ago. Their DLM segment is positioned to capture some of this, though execution risk here is real — government contracts have their own timelines.

On the digital engineering side, the transition of industrial clients toward smart, connected products is a decade-long wave. This company is well-positioned to ride it, especially in utilities and communications.

Management has been disciplined on capital allocation. Promoter holding sits around 23%, which is on the lower end — that’s a legitimate question mark and warrants monitoring for further dilution or block deals. Institutional investors have been building positions steadily, which provides some offset.

Expected returns: 12–15% CAGR over 5 years in a base case. In a bull case (margin expansion + DLM scale-up + aerospace supercycle), 18–20% CAGR is achievable. Over 10 years, if the business executes well, this has multi-bagger potential.

Risks — and let’s be honest about them:

The currency headwind is real. A significant portion of revenue is USD-denominated. If the rupee strengthens meaningfully, earnings take a hit.

Client concentration exists — top clients account for a disproportionate share of revenue. Losing even one major aerospace OEM relationship would hurt.

The DLM segment is still maturing. Manufacturing margins are lower than services, and scale-up has been slower than initially guided. If this drags, overall margin expansion gets capped.

Talent attrition in engineering services is always a risk. Losing senior technical leadership or domain experts to competitors or global MNCs can impair delivery quality.

Finally, macroeconomic slowdown in the US and Europe — their primary markets — would compress capex spending by OEM clients and delay discretionary engineering programs.

Bottom line: This is a quality business at a fair price with a long growth runway. It’s not a screaming buy, but for patient investors with a 3–5 year horizon, the risk/reward is compelling. The industry tailwinds are structural, the balance sheet is clean, and management has demonstrated consistent execution.