Consolidated Finvest & Holdings Ltd (NSE: CONSOFINVT | BSE: 500226)

Current Price: ₹159 (as of Dec 11, 2025)

Market Cap: ₹514 Crores

Here’s the thing - this stock is dirt cheap on paper but there’s a catch. The company’s trading at just 7.7 times earnings and half its book value. That’s the kind of discount that makes you look twice. They’re sitting on massive unrealized gains from their investments, which is why profits jump around like crazy year to year.

Business Model & Operations

Consolidated Finvest is an NBFC, but not your typical one. They don’t do consumer lending or microfinance. Instead, they’re a Core Investment Company - basically a holding company that invests in shares, bonds, mutual funds and gives loans to group companies. Think of them as the investment arm of the B.C. Jindal Group.

The business is simple: They buy stakes in companies, earn dividends, make money on stock appreciation, and charge interest on loans they give out. About 75% of their shares are held by the promoters (Concatenate Advest Advisory Pvt Ltd), so this is essentially a family-controlled investment vehicle.

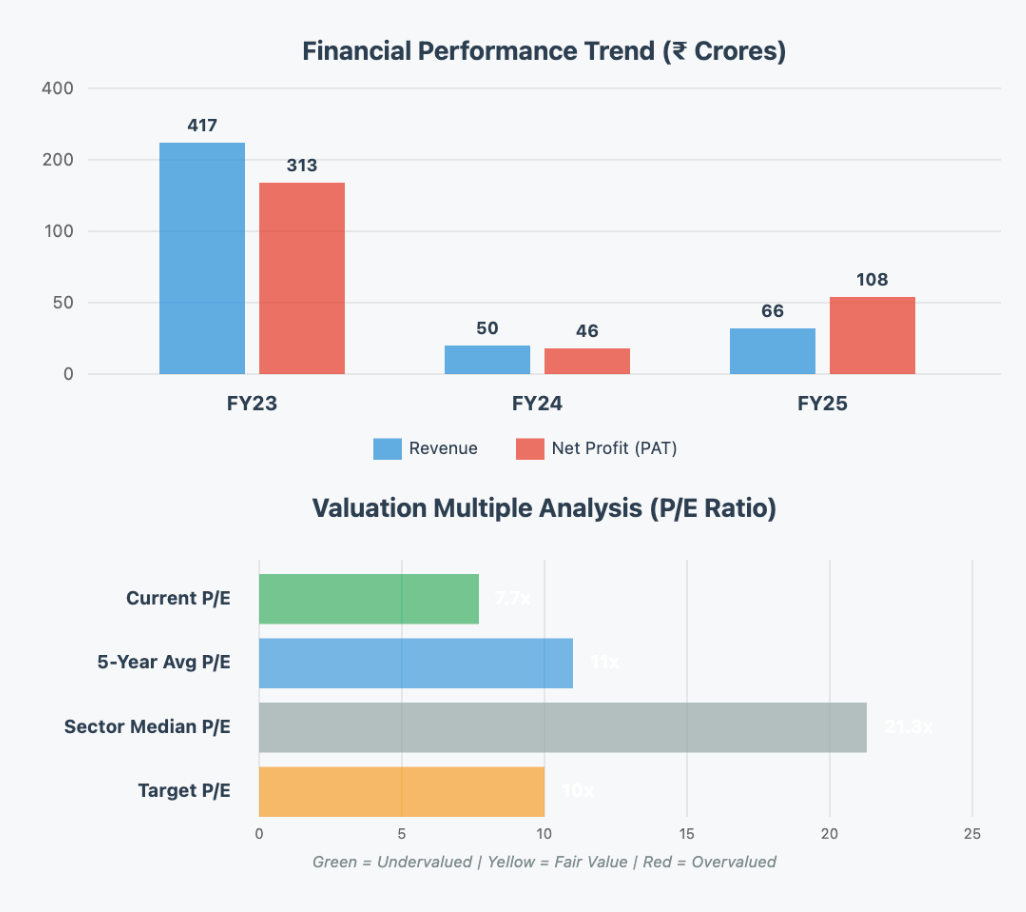

Their revenue model is unusual for an NBFC. Most of their income comes from dividend income and realized gains when they sell investments, not from traditional lending. This year they earned ₹66 crores in revenue with ₹108 crores in profit - yes, you read that right, profit is way higher than revenue because of how they book investment gains.

Historical Financial Review

Let’s talk numbers. Over the last three years, revenue grew at a whopping 75% CAGR. Sounds amazing, right? But here’s where you need to understand what’s happening - this isn’t steady operational growth. In FY23, they had a massive one-time jump because they booked huge gains from selling investments (₹313 crores profit that year).

In FY25, they made ₹108 crores profit on just ₹66 crores revenue. Their EPS shot up to ₹33.45 from ₹14.35 the year before. The company is debt-free - not a single rupee of borrowings. They’re sitting on ₹1,124 crores in total assets, with ₹1,119 crores invested in stocks and securities.

The quarterly numbers are all over the place. Some quarters they make ₹47 crores profit, other quarters it’s ₹13 crores. This volatility comes from when they decide to book gains by selling investments. Their operating cash flow is decent at around ₹10-14 crores annually, but the real action is in their investment portfolio.

Fundamental Valuation Metrics & Investment Call

Now for the valuation part. At ₹159, the stock trades at:

P/E Ratio: 7.7x (compared to 5-year average around 10-12x)

P/B Ratio: 0.49x (you’re paying 49 paise for every rupee of book value)

ROE: 11.8% (decent but not spectacular)

ROCE: 7.7% (fairly low for an investment company)

Dividend Yield: 0.71% (₹1.13 per share dividend)

The low P/B is the headline grabber here. Book value is ₹321 per share, and the stock trades at ₹159. That’s a 50% discount. But before you get too excited, understand why - the market doesn’t trust that book value will convert to cash anytime soon. These are holdings in group companies, not liquid assets.

The P/E of 7.7x looks cheap, but profits bounce around depending on when they sell investments. Last year’s EPS of ₹33 might be ₹15 next year or ₹40 - you just don’t know. That uncertainty keeps the multiple low.

My call is HOLD. If you own it, there’s no reason to panic sell - the downside is limited with the company trading below book value and being debt-free. But if you’re thinking of buying, wait for either a clearer catalyst or a better entry point around ₹140-145. The upside to ₹220-240 (fair value based on 0.7x P/B) exists, but it could take 2-3 years to play out.

Long-Term Outlook & Risk Assessment

Looking out 5-15 years, I’d estimate returns of 8-12% CAGR. That’s not going to make you rich, but it’s reasonable for a debt-free investment company trading below book.

What could go right:

The Indian equity market continues its bull run, lifting their portfolio values

They monetize some holdings at good valuations

The group companies they’ve invested in perform well and pay regular dividends

The discount to book value narrows as the market recognizes value

What could go wrong:

Liquidity trap: Their investments are mostly in unlisted or low-liquidity group companies. Converting those to cash could be tough

Related party concentration: About 75% held by promoters, investments mostly in group cos - classic risk if the group faces trouble

No growth catalyst: They’re not building new businesses or expanding operations. This is a passive holding company

Market correlation: If markets crash, their portfolio takes a direct hit

Tax rate volatility: Notice their tax rates jump all over (some quarters negative). This happens with investment companies based on how gains are classified

The promoter holding stayed steady at 74.9% - that’s good, they’re not selling. But FII holding is tiny at 4.2%, which means foreign investors aren’t interested. That limits buying pressure.

Bottom line: This is a deep value play with hair on it. The discount to book is real, the company is conservatively managed, and there’s no debt risk. But the path to unlocking value is unclear and could take years. It’s not a momentum stock or a growth story - it’s a patient value investor’s bet that’s probably best suited for someone who wants exposure to the Jindal Group’s investment portfolio at a discount. Just don’t expect fireworks anytime soon.