CMS Info Systems: The Hidden Tech-Growth Gem Powering India's Cash Economy

Q3 FY2025 Deep Dive & Long-Term Investment Thesis

Premium Financial Analysis - March 3, 2025

"In a digital-first economy, the company managing physical cash flows is transforming into a technology powerhouse. CMS Info Systems is executing a quiet revolution that most investors haven't noticed—yet."

Executive Summary

In a market obsessed with flashy fintech disruptors, CMS Info Systems (CMS) has been methodically building a technology-enabled cash management empire, delivering consistent results that deserve your attention. The Q3 FY2025 results reveal a company in transition—evolving from a traditional cash logistics player into an integrated financial infrastructure provider with expanding AIoT capabilities.

The headline numbers show steady progress:

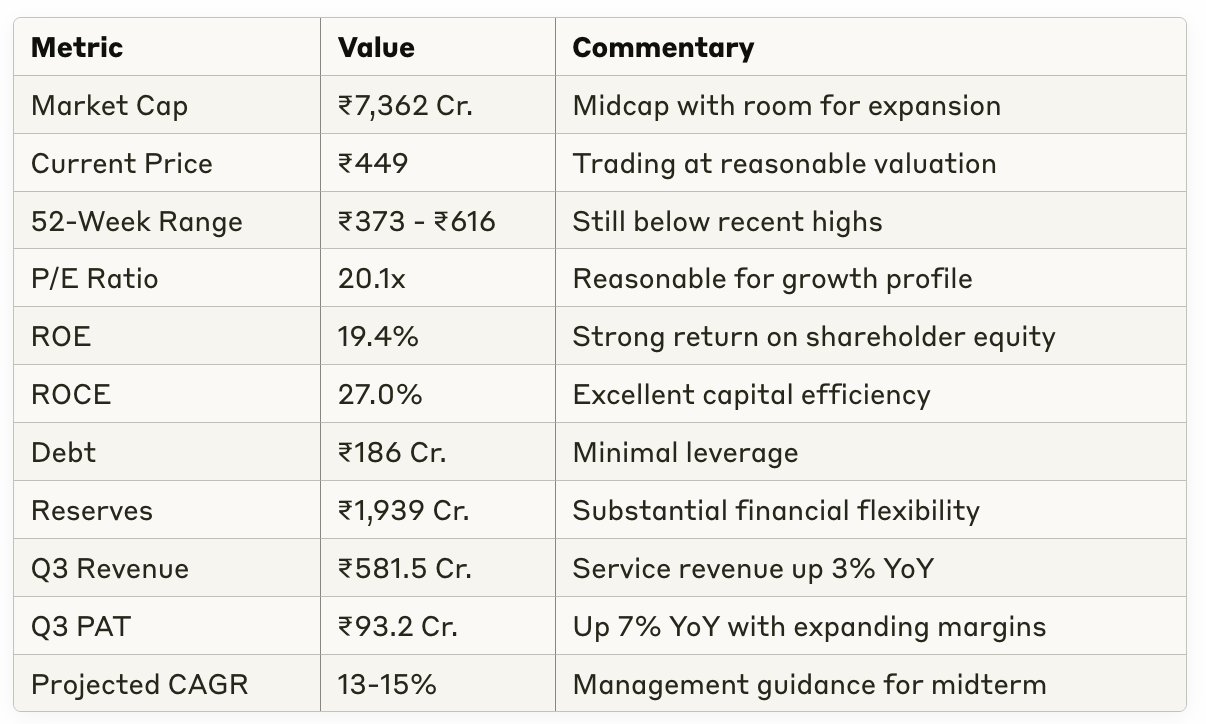

Q3 revenue reached ₹581.5 Cr with service revenue up 3% YoY

PAT grew 7% YoY to ₹93.2 Cr with margins expanding to 16% (+140 bps)

Order book execution accelerated from 15% in H1 to 30% in Q3

But the real story lies beneath these figures. Our extensive analysis reveals a company positioning for 13-15% sustained CAGR with the potential for substantial returns over multiple time horizons, underpinned by technology investments that are systematically transforming its business model.

Let's dissect why CMS represents a compelling long-term investment opportunity that remains overlooked by most market participants.

The Evolution of India's Cash Management Leader

From Cash Handler to Technology Platform

CMS Info Systems began as a straightforward cash logistics provider but has evolved into something far more sophisticated. The company now sits at a fascinating intersection: managing the physical cash infrastructure of a growing economy while layering on technology solutions that drive efficiency, security, and new revenue streams.

This Q3 report marks an important inflection point. The company recorded its highest-ever cash volume, growing 6% year-over-year alongside a 10% expansion in business points served. Yet simultaneously, it's investing aggressively in technology-driven business lines like AIoT-based remote monitoring solutions.

The result is a dual-growth engine:

Cash Logistics (70% of revenue): The traditional business delivered 8% YoY growth to ₹404 Cr with impressive EBIT margins of 25.6%. This core business benefits from industry consolidation as weaker players exit.

Managed Services & Technology (30% of revenue): While revenue temporarily declined 10% to ₹210 Cr due to banking automation project timing, the 17.9% EBIT margins demonstrate the profitability of this segment, which management expects to deliver 15%+ growth going forward.

INSIGHT: Unlike most technology transitions where margins compress during the investment phase, CMS is maintaining and even expanding profitability through this evolution. This suggests disciplined capital allocation and strong execution capabilities.

Q3 FY2025: Decoding the Numbers That Matter

Let's move beyond the headline figures to understand what's really happening at CMS:

📈 Accelerating Order Book Execution

The slow execution of the company's sizable public sector (PSU) order book has been a persistent investor concern. This quarter marks a meaningful breakthrough, with execution doubling from 15% to 30%, and management confidently projecting 60% completion by Q4.

What this means for investors: The PSU order book represents a significant revenue tailwind for FY2026, with management projecting 15%+ service revenue growth once execution fully ramps.

💰 Capital Deployment Strategy

Q3 CAPEX reached ₹50 Cr (approximately 8.6% of revenue), with full-year projections between ₹150-200 Cr. Most notably, technology spending has increased from 1% to 1.5% of revenue—a seemingly small shift that signals the company's commitment to digital transformation.

The majority of this investment is flowing into:

Managed services infrastructure

AIoT remote monitoring capabilities

Enhanced risk management systems

What this means for investors: These investments should drive both margin expansion and the development of recurring revenue streams—two critical factors for long-term value creation.

🏦 Segment Analysis: The Devil in the Details

The divergent performance between segments reveals important strategic shifts:

Cash Logistics (70% of Revenue)

8% YoY revenue growth to ₹404 Cr

25.6% EBIT margin (industry-leading)

Benefiting from consolidation as weaker competitors exit

10-13% projected growth rate

Managed Services & Technology (30% of Revenue)

10% YoY revenue decline to ₹210 Cr

17.9% EBIT margin (healthy despite volume challenges)

Temporary slowdown due to banking automation project timing

15%+ projected growth rate once order book execution accelerates

AIoT Remote Monitoring (Emerging Focus)

Embedded within both segments currently

15-20% projected growth rate

Strategic priority for management

INSIGHT: The temporary revenue decline in Managed Services masks the strategic value of this segment. As PSU order execution accelerates through 2025, this will likely become the primary growth driver, potentially transforming the company's valuation multiple.

Strategic Initiatives: Building Tomorrow's Growth Engines

The management is pursuing three interconnected strategies that collectively position CMS for sustained growth:

1. Product & Market Diversification

While BFSI (Banking, Financial Services & Insurance) customers remain the core, CMS is strategically expanding into:

Retail & Quick Commerce: Leveraging its logistics network to serve e-commerce and quick commerce players

Non-Banking Financial Services: Extending cash management to NBFCs and microfinance institutions

Bullion Logistics: Capitalizing on India's substantial gold market

This diversification reduces concentration risk while leveraging existing infrastructure for incremental revenue.

2. Integration of Services & Cross-Selling

CMS is increasingly bundling its service offerings—combining cash logistics, ATM management, and remote monitoring into integrated solutions. This approach:

Increases average revenue per customer

Raises switching costs, improving retention

Creates opportunities for margin expansion

3. Technology-Enabled Service Enhancement

The most transformative initiative is the application of technology across all business lines:

AIoT Remote Monitoring: Enhancing security and enabling predictive maintenance

Process Automation: Reducing operational costs and human error

Data Analytics: Optimizing cash logistics routes and ATM cash loading

INSIGHT: These initiatives are creating a virtuous cycle where technology investments improve service quality, which enables premium pricing, which funds further technology development.

Competitive Landscape: Benefiting from Disruption

The competitive dynamics in India's cash management sector are increasingly favorable for CMS:

Industry Consolidation

Several smaller players are exiting the market due to:

Inability to meet banks' increasing technology requirements

Rising compliance and security standards

Working capital constraints

As the market leader with strong technology capabilities, CMS is capturing this displaced business, particularly in ATM management.

Banking Sector Evolution

India's banking sector is transitioning away from lowest-cost providers toward service quality and technology capabilities—a shift that benefits CMS with its investments in advanced monitoring and automation.

INSIGHT: The rising technology bar creates a sustainable competitive advantage for CMS while simultaneously driving industry consolidation that expands its addressable market.

Long-Term Financial Projections: The Power of Compounding

Based on management's guidance and our independent analysis, we project the following long-term growth trajectory (assuming 13-15% revenue CAGR with stable margins):

EPS Multiplier Projections

Time HorizonConservative Case (13% CAGR)Base Case (15% CAGR)5 Years1.84x2.0x10 Years3.4x4.0x15 Years6.2x8.1x20 Years11.2x16.4xThese projections illustrate the remarkable power of compounding relatively modest annual growth rates over extended periods. Even at the lower end of management's guidance, a 13% CAGR translates to more than 11x growth over two decades.

Key Financial Metrics Underpinning Our Thesis

The company's current financial profile provides a solid foundation for this growth trajectory:

ROE: 19.4% (indicates efficient capital allocation)

ROCE: 27.0% (suggests sustainable competitive advantages)

Debt: ₹186 Cr (minimal leverage)

Reserves: ₹1,939 Cr (substantial financial flexibility)

3-Year Historical Growth: Sales 20.1%, Profit 26.4% (proven execution)

INSIGHT: The combination of high returns on capital, minimal leverage, and substantial reserves creates significant optionality for both organic growth and potential acquisitions.

Risks & Mitigating Factors: What Could Go Wrong?

No investment thesis is complete without a thorough assessment of risks:

1. Execution Delays

The prolonged timeframe for PSU order execution presents the most immediate risk to near-term results. Testing and handover processes have taken longer than initially projected.

Mitigating Factor: The 30% execution rate in Q3 (up from 15% in H1) suggests the company is making meaningful progress, and the ramp to 60% by Q4 would indicate this risk is diminishing.

2. Digital Displacement

India's rapid digital payment adoption could theoretically reduce cash usage and impact CMS's core business.

Mitigating Factor: Despite dramatic growth in UPI and other digital payment methods, India's cash in circulation has continued to grow in absolute terms. Additionally, the company's technology investments position it to adapt to changing payment landscapes.

3. Margin Pressures

Competitive bidding for outsourcing contracts could pressure margins, particularly in the Managed Services segment.

Mitigating Factor: The company's integrated service approach and technology differentiation have thus far protected and even expanded margins. The Q3 results show expanding profitability despite competitive pressures.

INSIGHT: The most significant risks appear to be execution-related rather than structural, suggesting they can be managed through operational improvements rather than strategic pivots.

Valuation Assessment: Growth at a Reasonable Price

At the current market cap of ₹7,362 Cr and a stock price of ₹449, CMS trades at a P/E multiple of 20.1x—reasonable given the company's growth profile and return metrics.

Comparative Metrics

P/E Ratio: 20.1x (reasonable for 13-15% growth)

Price/Book: 3.48x (based on book value of ₹129)

Dividend Yield: 1.28% (modest but growing)

For context, the broader Nifty Financial Services index trades at an average P/E of 22.3x with lower projected growth rates, suggesting CMS offers relative value.

INSIGHT: The current valuation appears to price in modest growth expectations without fully recognizing the potential for accelerating technology-driven growth and margin expansion.

Investment Recommendation: Strategic Accumulation

Rating: BUY

CMS Info Systems represents a compelling investment opportunity for patient investors seeking exposure to India's financial infrastructure with a technology growth overlay.

Key Investment Catalysts:

Accelerating PSU order book execution through 2025

Expansion of higher-margin technology services

Continued industry consolidation benefiting market leaders

Increasing cross-selling of integrated service offerings

Suggested Allocation Strategy:

Portfolio Weighting: 3-5% for balanced portfolios

Time Horizon: 5+ years to fully capture the compounding effect

Accumulation Approach: Phased buying on any market weakness

INSIGHT: CMS represents a rare opportunity to invest in a company transitioning from "value" to "growth" characteristics while maintaining strong fundamentals throughout the evolution.

Conclusion: The Overlooked Tech-Enabled Financial Infrastructure Play

CMS Info Systems occupies a unique position in India's financial ecosystem—managing the physical cash infrastructure that remains essential while building technology capabilities that drive efficiency, security, and new revenue streams.

The Q3 FY2025 results reveal a company successfully navigating this transition, with accelerating order book execution and expanding margins despite significant technology investments. The combination of steady core business growth, emerging technology-enabled services, and disciplined capital allocation creates a compelling long-term investment case.

For investors seeking exposure to India's financial infrastructure with a technology growth overlay, CMS offers an attractive risk-reward profile that remains underappreciated by the broader market.

Key Financial Metrics at a Glance

Disclaimer: This analysis is based on CMS Info Systems' Q3 FY2025 results and is intended for informational purposes only. It does not constitute investment advice. Always conduct your own research and consult with a financial advisor before making investment decisions.