Building Generational Wealth: A Vision for Your Family's Future

Last week, I met Rajesh at a wedding in Delhi. Mid-conversation about his new job at an IT firm, he casually mentioned how his grandfather had bought land in Gurgaon for ₹50 per square foot in 1985. Today? That same plot is worth ₹15,000 per square foot. "If only he'd bought more," Rajesh sighed, staring into his drink.

That moment crystallized something I've been thinking about for years – the profound difference between building wealth for yourself versus building wealth that transcends generations.

The Mindset Shift That Changes Everything

Most young professionals I meet think in financial quarters. Maybe annual bonuses if they're feeling ambitious. But here's what three decades of managing portfolios taught me: generational wealth isn't built by thinking in years. It's built by thinking in decades.

When I started my career in the early '90s, I watched families make two distinct choices. Some invested with a 5-year horizon, constantly tweaking and second-guessing. Others planted seeds they knew their children would harvest. Guess which group built empires?

The Ambani family didn't become India's wealthiest by chasing quick gains. Dhirubhai started with polyester yarn – hardly glamorous – but he understood something most missed. He wasn't just building a business; he was creating a financial ecosystem that would compound across generations.

The Hidden Mathematics of Generational Thinking

Here's where it gets interesting, and frankly, a bit shocking when you run the numbers.

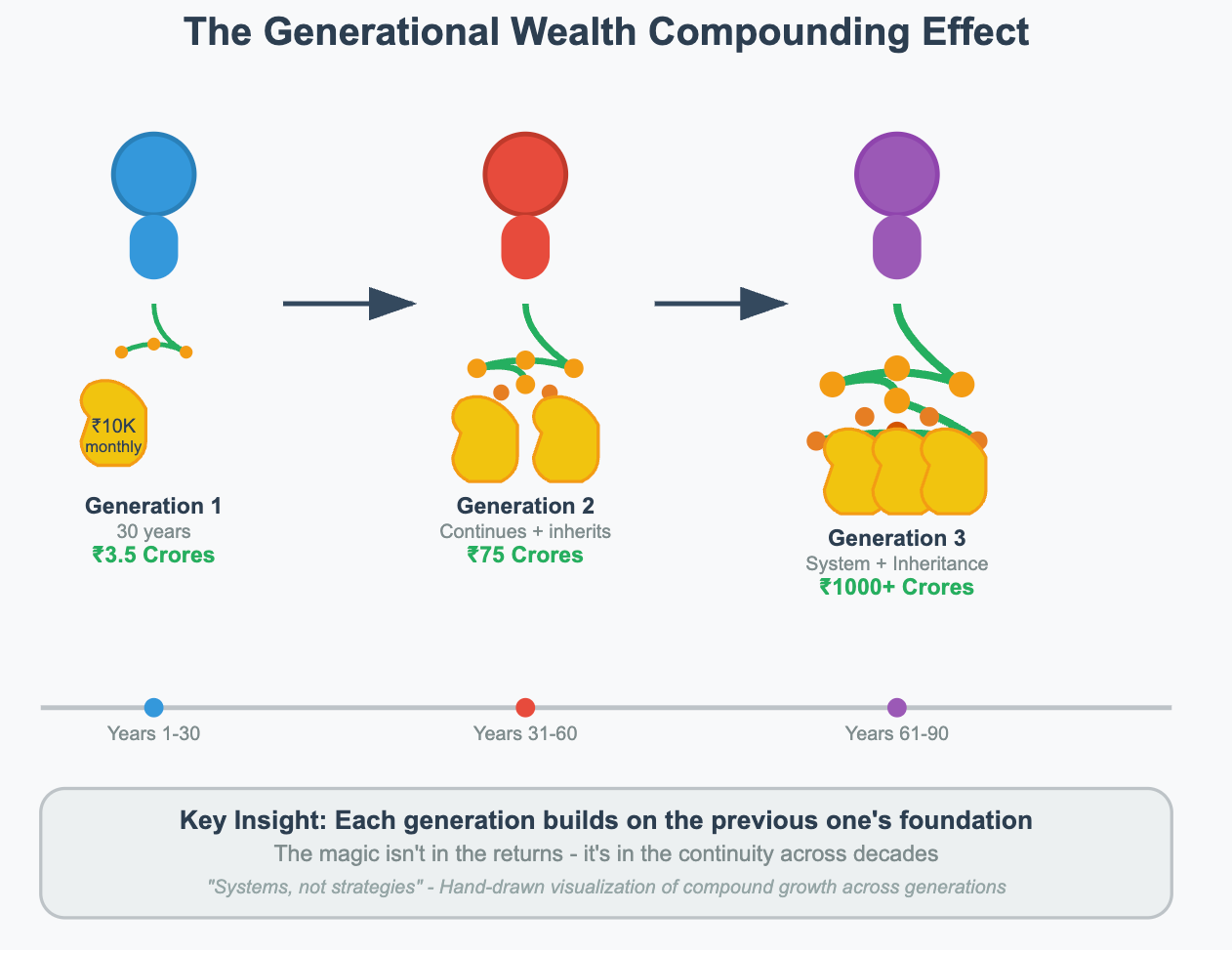

Consider two scenarios: Priya invests ₹10,000 monthly for 30 years at 12% annual returns. She accumulates roughly ₹3.5 crores. Impressive, right? Now imagine her daughter continues this exact same investment for another 30 years. The total? Nearly ₹75 crores.

But wait – there's a third scenario most people never consider. What if Priya had invested ₹15,000 monthly (just ₹5,000 more) and her family maintained this discipline across three generations? We're talking about wealth that crosses ₹1,000 crores.

The difference isn't just mathematical. It's philosophical.

The Three Pillars I've Observed in Wealth-Building Families

After watching hundreds of families build – or fail to build – lasting wealth, three patterns emerge consistently.

First, they diversify across time, not just assets. Most investors diversify their portfolio. Generational wealth builders diversify their timeline. They'll hold some investments for 5 years, others for 50. They understand that different assets peak at different life stages.

Second, they create systems, not strategies. Strategies can be abandoned during market downturns – and trust me, I've seen it happen countless times during the 2008 crisis. Systems become family culture. When your children grow up seeing monthly SIPs as normal as paying electricity bills, you've created something powerful.

Third, they think in terms of financial education inheritance. The Tata family didn't just pass down companies; they passed down business acumen. Your greatest inheritance to your children isn't money – it's teaching them how money works.

The India-Specific Opportunity Most Miss

Here's something that keeps me excited about Indian markets even after all these years: we're sitting on one of the world's greatest demographic advantages. While developed nations worry about aging populations, India has 600 million people under 25.

This isn't just a statistic. It's a generational wealth opportunity.

When these young Indians start earning and investing over the next two decades, the demand for quality companies will create returns that make today's markets look conservative. Families who position themselves now – in sectors like consumer goods, healthcare, and education – are essentially front-running history.

I recently increased my allocation to companies serving India's aspirational middle class. Not because they're undervalued today, but because they'll be essential 20 years from now.

The One Decision That Matters Most

If you take nothing else from this, remember this: the biggest risk to generational wealth isn't market crashes or inflation. It's interruption.

Every family I've seen fail at building lasting wealth made the same mistake – they stopped. Market crash? They paused investing. Job loss? They liquidated positions. Family emergency? They broke the system.

The families who succeed? They plan for interruptions. They create multiple income streams, maintain emergency funds that don't touch investment capital, and most importantly, they teach their children that wealth building continues regardless of temporary setbacks.

Your Next Step: Open a conversation with your family about money. Not just budgets or expenses, but your vision for where you want your family to be in 2050. Because here's the truth – generational wealth starts with generational thinking, and that starts today.

What would your family look like with three decades of compound growth behind it? More importantly, what are you willing to do today to find out?

Very well articulated

Wonderful education