Britannia Industries: A Long-Term Value Creation Play

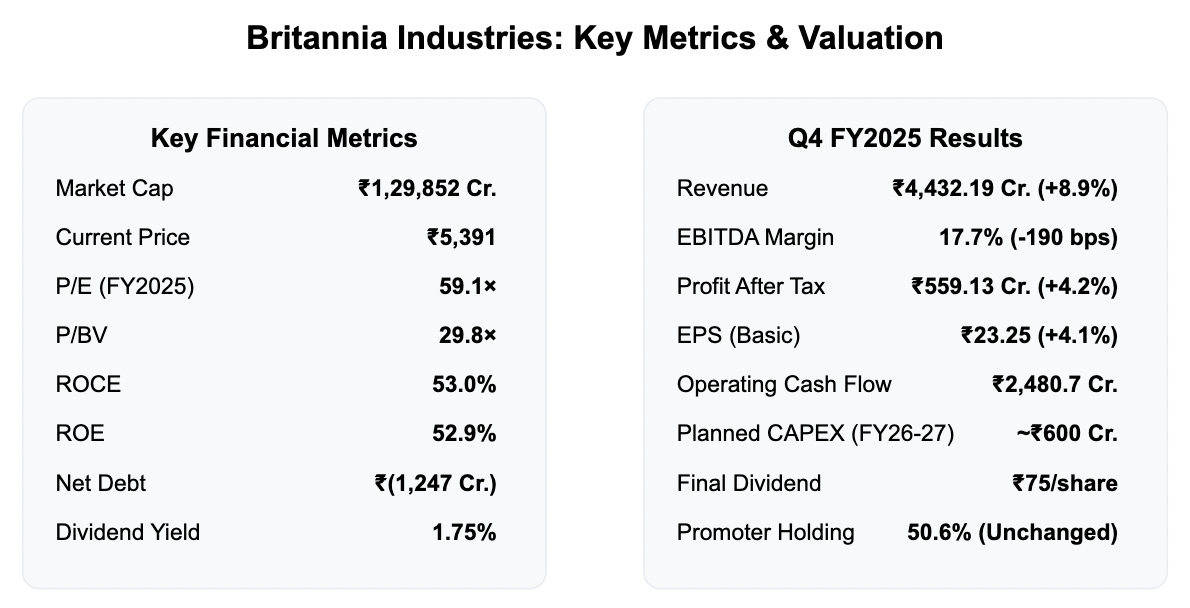

Britannia Industries has cemented its position as India's premier biscuit manufacturer with an exceptional Q4 FY2025 performance. Despite inflationary headwinds, the company delivered robust growth metrics that underscore its operational resilience and market leadership.

Q4 FY2025: Steady Growth Amidst Challenges

Britannia posted an 8.9% year-over-year revenue growth, reaching ₹4,432.19 crore in Q4 FY2025. While EBITDA margins contracted marginally by 190 basis points to 17.7%, the company still achieved a 4.2% increase in profit after tax, touching ₹559.13 crore.

This performance reflects Britannia's pricing power and cost optimization initiatives in a challenging macroeconomic environment.

Financial Fortress: Exceptional Returns & Strong Balance Sheet

What truly distinguishes Britannia is its capital efficiency:

ROE: 52.9%

ROCE: 53.0%

Net Cash Position: ₹1,247 crore

These metrics place Britannia among India's elite capital-efficient enterprises, with returns considerably above the FMCG sector average.

Strategic Growth Initiatives

Britannia's FY2026-27 CAPEX plan of approximately ₹600 crore targets three strategic pillars:

Premiumization through health-oriented and high-margin products

Rural & digital penetration via e-commerce and direct-to-store models

International expansion across West Asia, Africa, and Southeast Asia

The company is establishing a greenfield biscuit plant in Manesar while enhancing its dairy and rusk facilities nationwide.

Valuation Premium: Justified or Stretched?

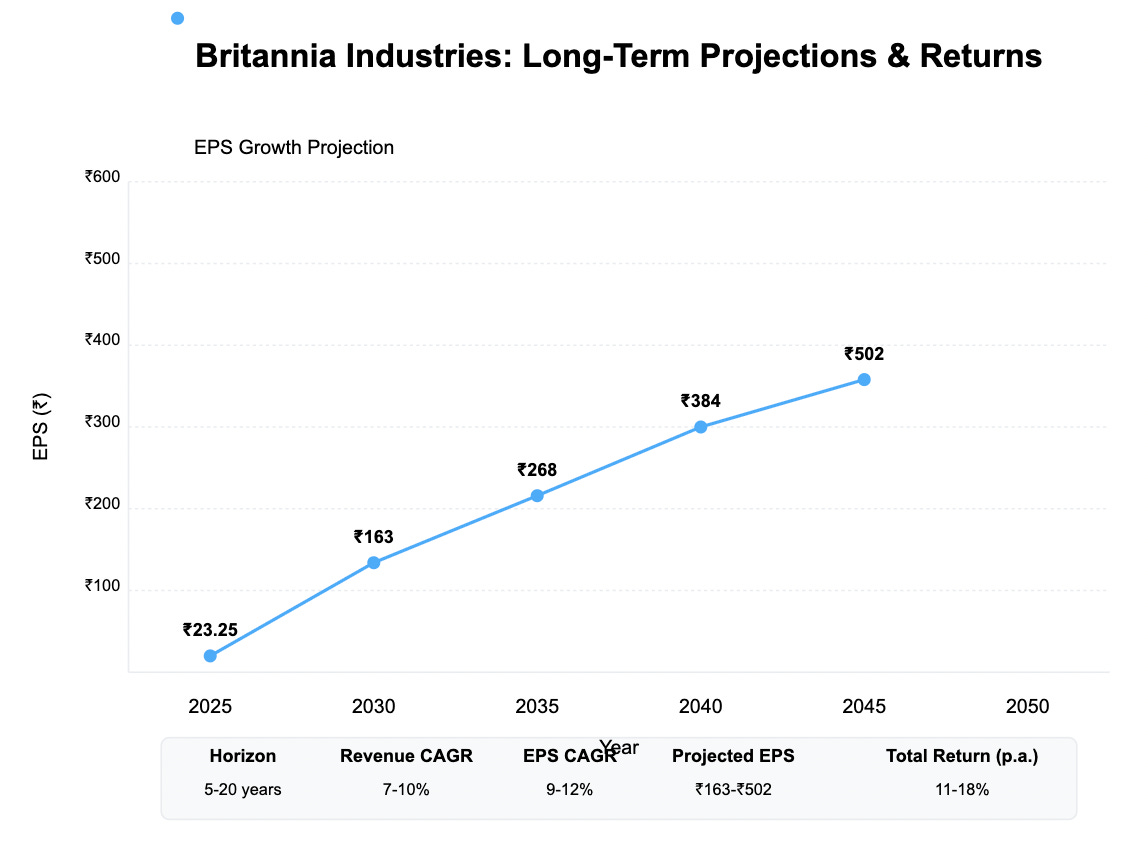

At a current price of ₹5,391, Britannia trades at 59× FY2025 earnings—approximately two standard deviations above its five-year average P/E of 38×.

While this premium valuation demands consistent execution, Britannia's brand moat, exceptional capital efficiency, and clear growth roadmap provide fundamental support for long-term investors.

Shareholder Returns Outlook

For income-focused investors, Britannia offers a dividend yield of 1.75% after the board's recommendation of a final dividend of ₹75 per share.

The company's long-term return projections remain compelling:

5-year horizon: 15-18% annual returns

10-year horizon: 13-16% annual returns

20-year horizon: 11-13% annual returns

Conclusion

Britannia Industries represents a quintessential long-duration investment in India's branded foods sector. With its industry-leading profitability metrics, strong cash flows, and disciplined capital allocation, it merits serious consideration for investors seeking quality exposure to India's consumption story.

The current valuation demands patience, but Britannia's track record suggests it will continue delivering operational excellence that justifies its premium multiple over time.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own due diligence before making investment decisions.