Bombay Super Hybrid Seeds Ltd

Revenue Projections for next three years

Investment Highlights

Market Cap: ₹1,492 Cr

Current Price: ₹142

52-Week High/Low: ₹266 / ₹129

Stock P/E: 58.9

Book Value: ₹8.71

ROCE: 23.9%

ROE: 33.0%

Dividend Yield: 0.00%

Business Overview

Bombay Super Hybrid Seeds Ltd (BSHSL) is a leading player in India’s agricultural seed market, focusing primarily on edible oilseed segments like groundnut and sesame. With a robust R&D program and a product portfolio of over 120 varieties, BSHSL operates across 14 Indian states with depots in 8 of them.

Growth Drivers

R&D Expansion

Planned capital expenditure of ₹1 Cr for developing new high-yielding and disease-resistant varieties, including pearl millet, corn, wheat, and hot pepper.

Collaboration with premier research organizations such as ICRISAT, CIMMYT, and IARI.

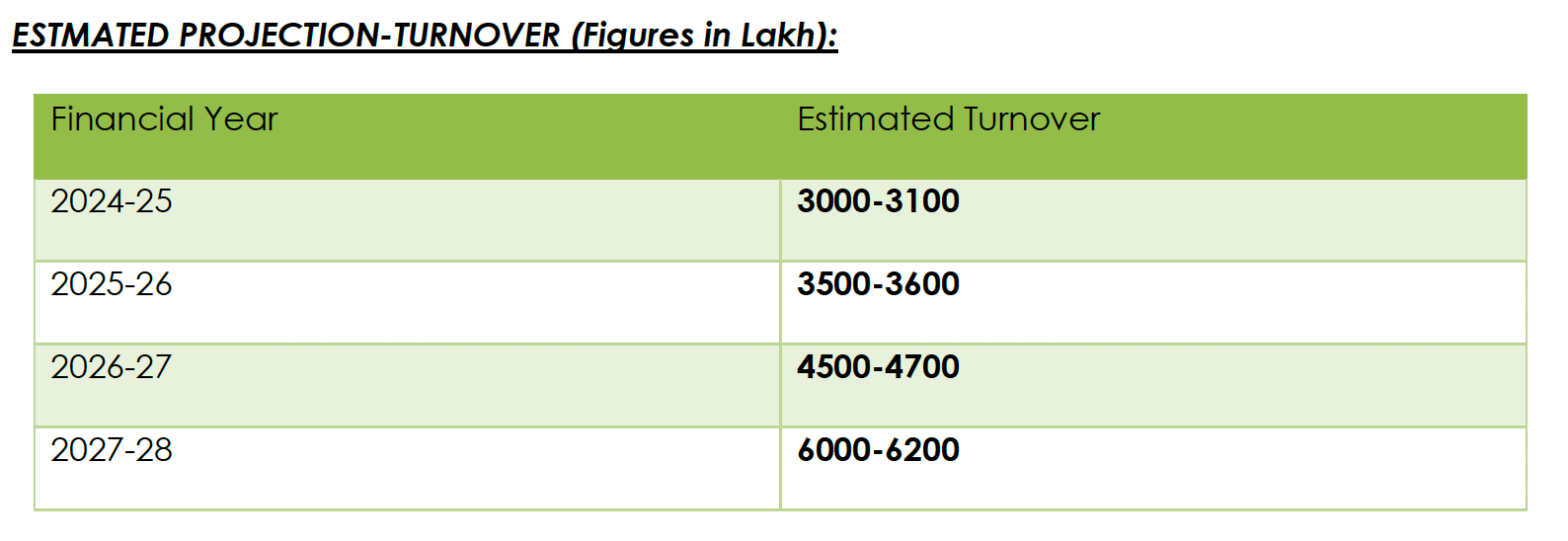

Revenue Projections

Estimated revenue growth from ₹3,000-₹3,100 Cr (FY25) to ₹6,000-₹6,200 Cr (FY28).

Sales CAGR of 14.5% over the last three years reflects strong market demand and operational efficiency.

Technological Advancements

Investments in Buhler Sortex machinery for precision seed grading.

Development of 10,000 metric tons of low-energy seed cold storage.

Diversified Product Portfolio

Groundnut dominates revenue with a share of ~55%. Expansion in gram, cumin, and other high-value crops adds diversification.

Export Market Potential

Export licensing and participation in global seed trade events signal future international growth.

Financial Highlights

Sales (H1FY24): ₹15,042.42 Lakh, YoY growth of 26%.

EBITDA Margin: 10.51% (H1FY24), improving steadily.

Profit After Tax (H1FY24): ₹1,220.65 Lakh.

Balance Sheet:

Debt: ₹37.4 Cr, significantly reduced from previous years.

Reserves: ₹80.9 Cr, showcasing strong equity growth.

Strategic Rationale for CapEx

The company’s ₹1 Cr R&D allocation targets product innovation and improving crop yield. Collaborations for biofortified wheat and anti-cancer Korean cabbage exemplify a strategic pivot towards health-focused agricultural products.

Competitive Landscape

Strengths:

Largest seed portfolio in India.

Established partnerships with global research institutions.

High ROE (33%) and strong promoter holding (73.8%).

Weaknesses:

Low dividend yield indicates limited shareholder return.

High valuation (P/E 58.9) raises concerns of overvaluation.

Threats:

Climate risks impacting crop yield.

Increasing competition from domestic players like Kaveri Seeds and multinational corporations.

Valuation Estimate

Assuming a conservative forward P/E of 40 and FY25 projected earnings of ₹80 Cr, the target price is ₹152, reflecting a modest upside potential of 7% from the current market price.

Investment Thesis

Bombay Super Hybrid Seeds Ltd is well-positioned for sustained growth, driven by its robust R&D capabilities, diversified portfolio, and expanding geographical footprint. However, its high valuation and dependency on monsoon conditions pose risks. Long-term investors seeking exposure to India’s agritech sector may find value in its growth story.

Disclaimer

This report is for informational purposes only and does not constitute financial advice. Investors are advised to conduct their own research or consult a financial advisor before making investment decisions.

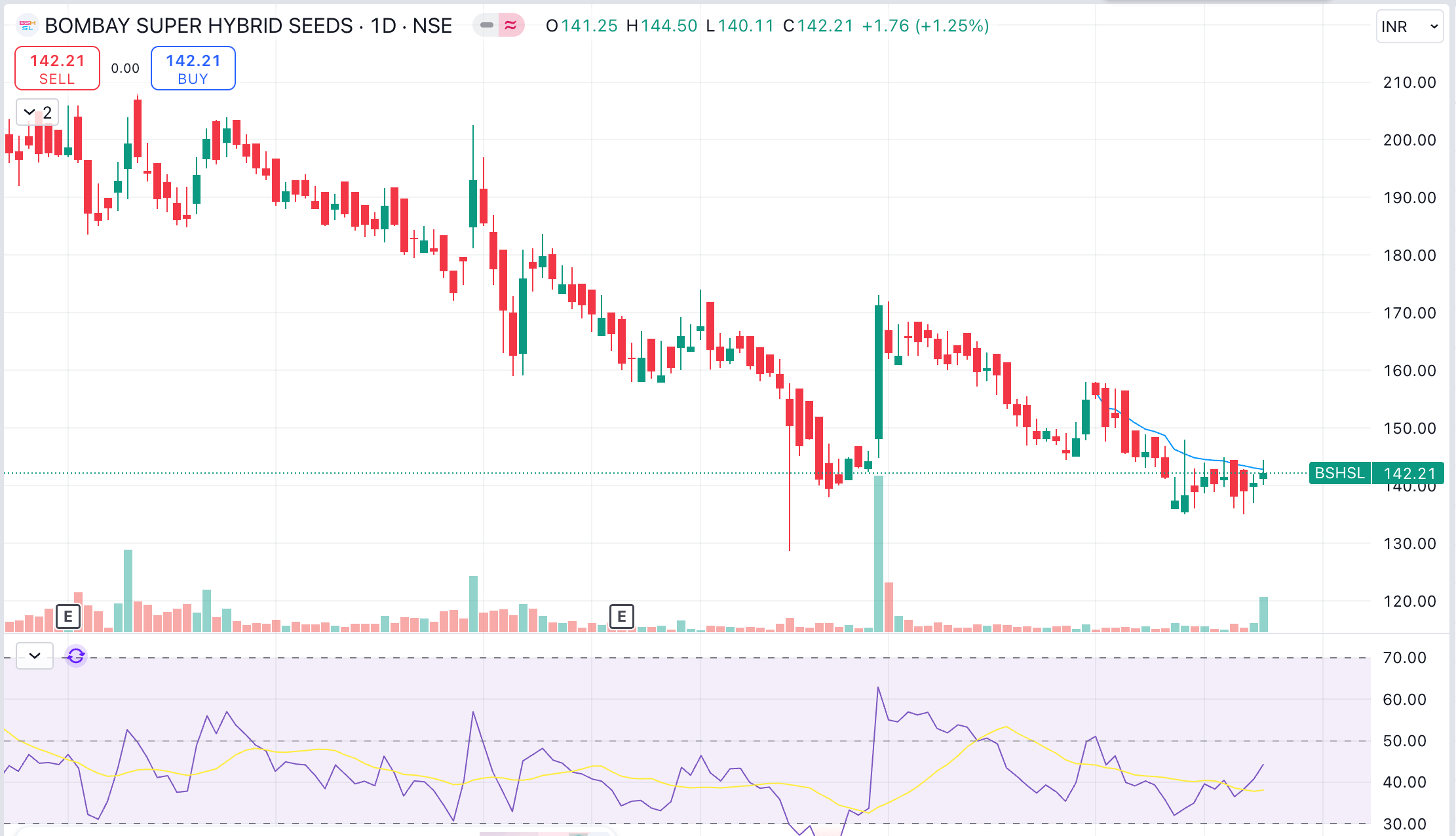

Technically Stock Price reversed