Bharti Hexacom Stock Target 2026: Growth Outlook, Valuation & Buy-or-Not Analysis

The Core Thesis:

This stock’s trading at premium valuation, sure - but here’s the thing most people miss. The company just posted a 53% operating margin last quarter. That’s not a typo. While everyone’s obsessed with the parent company’s national story, this regional player is quietly printing money in two circles where competition’s basically a duopoly. The margins keep expanding, cash flow’s strong, and the stock’s still got room to run as 5G penetration deepens in these markets.

How This Business Actually Makes Money

This is a wireless telecom operator - plain and simple. They run mobile networks in Rajasthan and the North East states (Arunachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland, and Tripura). Think of it as the Airtel you know, but focused exclusively on these two circles.

They’ve got two main revenue streams. The big one - about 95% of sales - comes from mobile services: voice calls, data packs, SMS, roaming charges, the works. The smaller chunk comes from fixed-line broadband and landline services, mainly in Rajasthan. They operate under the Airtel brand (they’re 70% owned by Bharti Airtel), so they get all the brand muscle and technology backbone of the parent.

Here’s what matters for your money: They’re the number two player in both these circles with a 37.6% market share. In telecom, being number one or two is everything - you get economies of scale, better tower utilization, pricing power. They’ve been rolling out 5G aggressively over the last year, adding fiber capacity for home broadband, and pushing postpaid customers hard (postpaid users spend 3-4x more than prepaid).

The latest quarter shows they’re adding about 1.4 million customers every three months. More importantly, they’re not just adding users - they’re upgrading existing ones to higher-value plans. That’s how you get to 53% operating margins.

Youtube Link:

The Numbers Tell a Growth Story

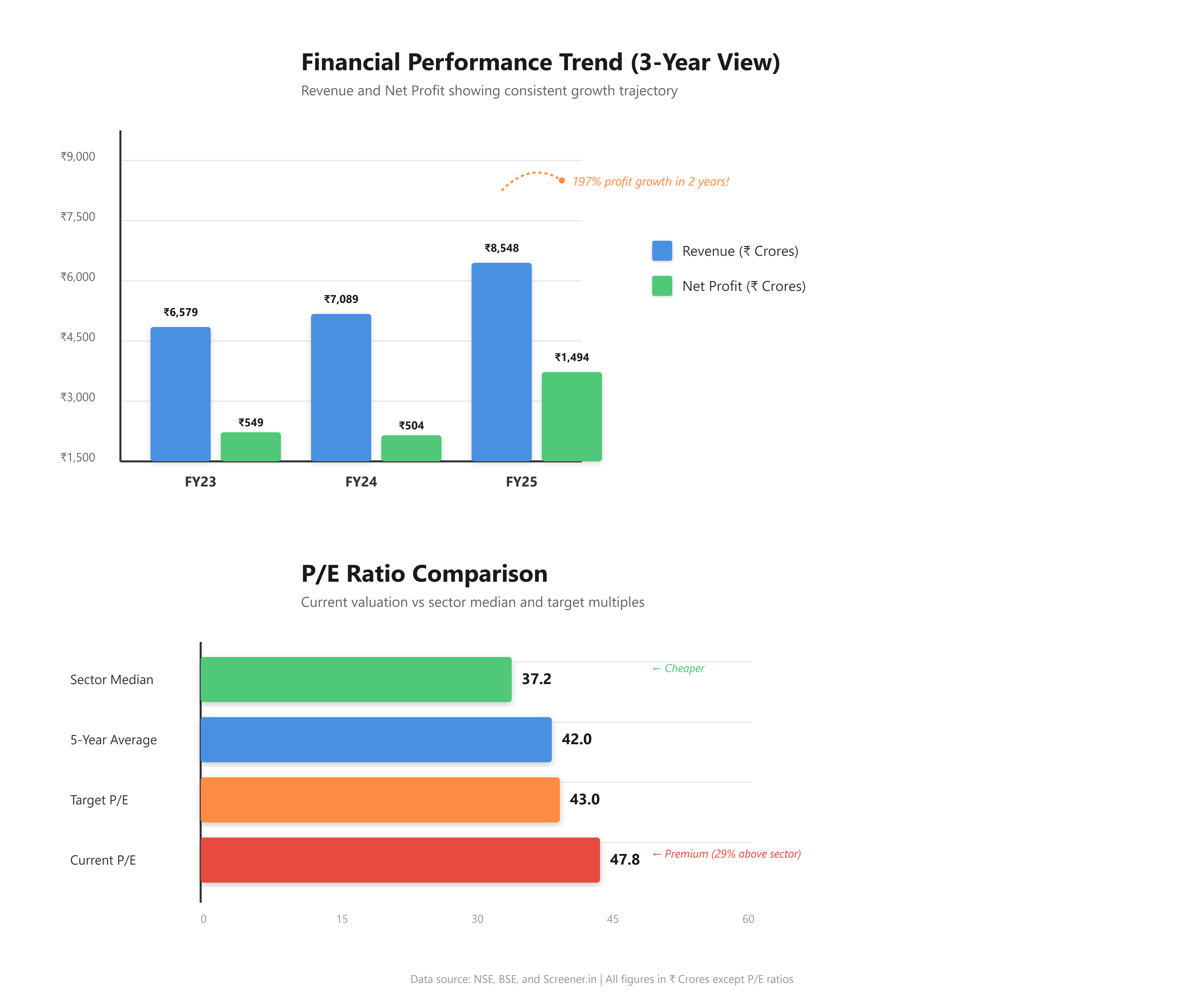

Revenue’s been climbing steadily. Over the last three years, sales grew at 17% annually - from ₹6,579 crores in FY23 to ₹8,548 crores in FY25. The trailing twelve months just crossed ₹9,200 crores. That’s not explosive growth, but it’s solid and consistent.

But here’s where it gets interesting: profits are growing way faster than sales. Net profit jumped from ₹549 crores in FY23 to ₹1,494 crores in FY25. That’s a 143% increase in three years. Last twelve months, they earned ₹1,755 crores in profit. Earnings per share hit ₹35 for the trailing year, up from just ₹10 two years ago.

Why the profit surge? Two reasons. First, they’re getting more revenue from each customer without adding proportional costs - that’s operating leverage kicking in. Second, they paid off expensive debt and refinanced at lower rates. The operating margin went from 42% in FY23 to 49% in FY25, and it’s now running at 53% in the latest quarter.

Cash generation’s healthy too. They threw off ₹4,583 crores in operating cash flow last year. After spending on network expansion and 5G rollout, they’ve been paying down debt steadily. Net debt to EBITDA ratio dropped to 1.25 times - that’s comfortable territory for a capital-intensive telecom business.

The balance sheet’s in good shape. Promoter holding’s rock solid at 70% - hasn’t budged in years. No signs of selling. Book value is ₹125 per share, though that’s not super relevant for a telecom company (most value’s in licenses and networks, not physical assets).

Valuation: Expensive, But Maybe Worth It

Let’s talk price. At ₹1,689, the stock trades at a P/E ratio of 47.8. That’s steep - no sugarcoating it. The telecom sector median P/E is 37.2, so you’re paying a 29% premium to peers.

Here’s how I justify it. This isn’t your typical telecom stock. First, the ROE is 25.2% - they’re turning every rupee of shareholder money into ₹0.25 of annual profit. That’s excellent. Second, the ROCE (return on capital employed) is 17.4% - above their cost of capital, meaning every investment they make is value-accretive.

Third, and most important: the growth profile. Earnings are compounding at 35% annually over the last five years. Show me another telecom stock growing profits that fast. The market’s willing to pay up because the earnings growth is real and accelerating.

The P/B ratio of 13.8 looks scary on paper, but again - book value in telecom doesn’t capture the spectrum licenses, customer base, or brand value. Focus on earnings and cash flow instead.

Dividend yield’s a modest 0.58%, which is fair. They paid out 33% of profits as dividends last year (₹10 per share). The rest is being reinvested in 5G and fiber expansion - smart capital allocation given the growth opportunities.

Compare this to parent Bharti Airtel trading at a P/E of 37. This company’s growing faster, has better margins in its circles, and you’re only paying a 29% premium. That gap should narrow.

My target price of ₹2,050 implies a 21% upside from current levels. I’m valuing it at 43x forward earnings (assuming ₹48 EPS for FY27), which still represents a premium but accounts for the superior growth and margins. If they hit my estimates, that target could be conservative.

Long-Term View: 12-16% Annual Returns Over the Next Decade

Here’s my 5-15 year outlook: expect 12-16% annual returns if you buy at these levels. Not spectacular, but solid for a large, established business.

The bull case is straightforward. India’s data consumption per user is still one-tenth of developed markets. As 5G penetration increases (currently under 15% in these circles), average revenue per user (ARPU) should climb from ₹256 to potentially ₹350-400 over the next 3-4 years. That’s a 40% revenue boost without adding a single customer. Layer on 5-7% annual subscriber growth, and you’re looking at high-teens revenue growth for several years.

Management’s investing heavily - ₹2,341 crores in capex last year, mostly on 5G and fiber rollouts. They’re expanding fiber home passes aggressively, which locks in customers and boosts ARPU through convergence (mobile + broadband bundles). The parent company’s partnership with Google for data centers in the region could drive enterprise connectivity revenue.

Promoters aren’t selling - that 70% stake hasn’t moved. They’re paying steady dividends (₹10 last year) while reinvesting for growth. Clean balance sheet gives them flexibility.

Now the risks - and there are real ones. First, competition. If Vodafone Idea somehow stabilizes or if Reliance Jio decides to get aggressive on pricing in these circles, margins could get squeezed. Telecom’s a scale game - if market share slips, profitability follows.

Second, regulatory risk. The government could hike spectrum fees, impose new license conditions, or delay spectrum auctions. Anything that increases costs or limits pricing power is bad news.

Third, execution. They’re rolling out 5G fast, but if the technology fails to drive ARPU increases - if customers don’t see value in paying more for 5G speeds - the investment won’t pay off. Customer upgrades need to happen.

Fourth, the valuation itself is a risk. At 48x earnings, you’re paying for perfection. One bad quarter, one margin slip, and the stock could correct 15-20% fast. This isn’t a bargain - you’re buying quality at a full price.

The India telecom sector’s in a sweet spot though. After brutal price wars from 2016-2020, the market’s consolidated to basically three players. Pricing discipline has returned. Data consumption’s exploding. 5G’s driving upgrades. Rural penetration still has legs. The regulatory environment’s stable. These are tailwinds that should persist for years.

For a 10-15 year hold, I’m modeling 14-15% revenue CAGR, operating margins stabilizing around 50-52% (down slightly from the current 53% as they invest in customer acquisition), and modest P/E compression to 35x by year 10. That gets you to a 13-14% annualized return, plus dividends. Not bad for a large-cap, established business in a duopoly market.

Bottom line:

This is a quality business trading at a quality price. If you’re comfortable with telecom exposure and want a regional play levered to India’s data consumption boom, this fits. Just don’t expect it to triple in three years - this is a grind-it-out compounder, not a momentum rocket.