AXISCADES Technologies: Q3 FY2025 Results & Future Growth Roadmap

🚀 The Future of AXISCADES: A Multibagger in the Making?

📌 Key Takeaways from Q3 FY2025

🔹 Revenue Growth: ₹274 Cr (+18.4% YoY) 🔹 EBITDA: ₹40 Cr (+36.9% YoY), margin expansion to 14.6% 🔹 PAT: ₹14.8 Cr (+96% YoY), PAT margin at 5.3% 🔹 Core Business Contribution: 99% EBITDA from Aerospace, Defense & AI 🔹 Defense Segment Growth: +88% YoY, EBITDA margin at 18% 🔹 Aerospace Growth: +11% YoY, EBITDA margin at 24% 🔹 Order Book: $83 million (~₹710 Cr) as of Dec 31, 2024 🔹 Debt Reduction: Finance costs down 39.7% YoY, net debt at ₹35.5 Cr

📊 AXISCADES: A Deep Dive Into Growth Plans & Expansion Strategy

AXISCADES Technologies Limited is rapidly evolving into a defense, aerospace, and AI-driven powerhouse. With strong revenue visibility, aggressive CAPEX plans, and high-margin contracts, the company is setting itself up for exponential growth in the coming years.

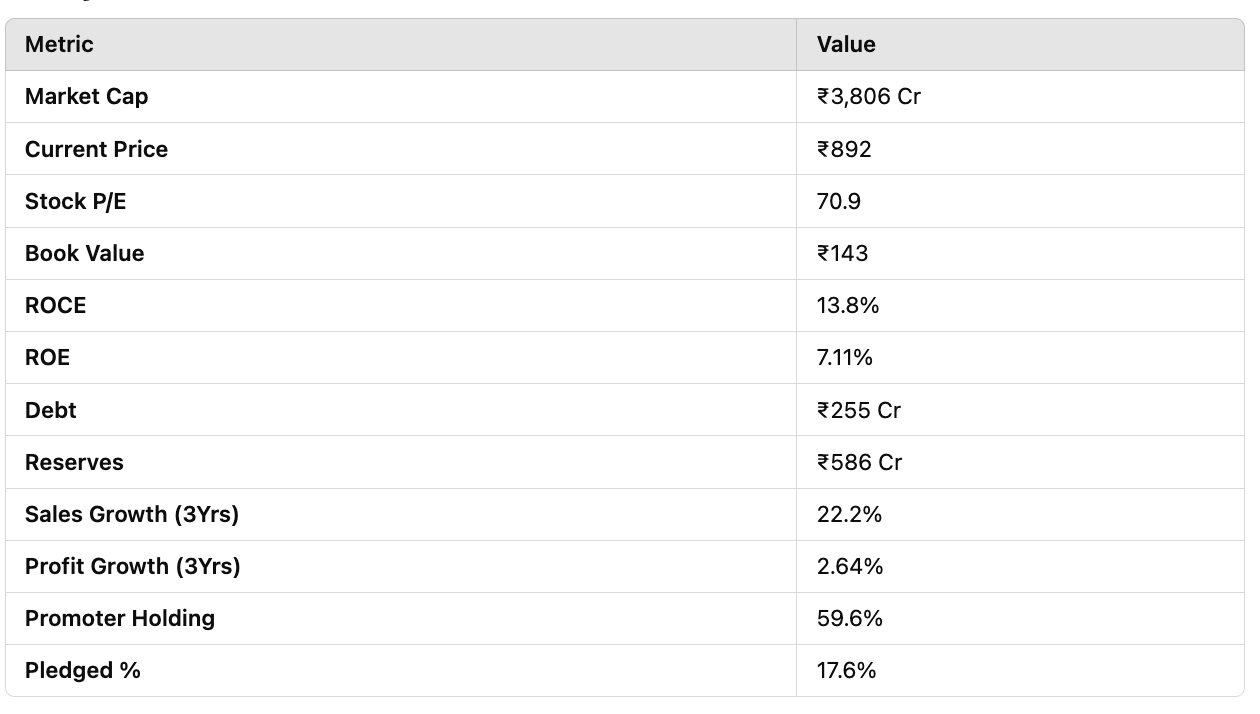

🔹 Key Financial Metrics & Valuation

🌍 Expansion Plans: The Next Growth Phase

🛡️ Aerospace & Defense Focus

✔ Increased defense contracts with India’s DRDO & global OEMs ✔ Scaling up production of anti-drone systems & radar technologies ✔ New orders expected for Sukhoi & LCA Tejas upgrades ✔ Large pipeline of offsets & defense exports

💡 AI & Semiconductor Growth (ESAI)

✔ AI-based MRO (Maintenance, Repair & Overhaul) facilities ✔ Expansion in post-silicon product development ✔ Micro data centers & quantum AI-driven solutions ✔ Partnerships with Texas Instruments, NVIDIA, NXP, Qualcomm

🏗️ Major CAPEX Investments

📌 ₹180 Cr Expansion Plan (Radar integration, AI-based MRO, Defense R&D) 📌 Devanahalli Atmanirbhar Cluster (DAC) – ₹500 Cr+ mega project 📌 Electronic City (40,000 sq ft) – UAV & Defense tech hub 📌 Aero Land (180,000 sq ft) – AI-driven aerospace technology development

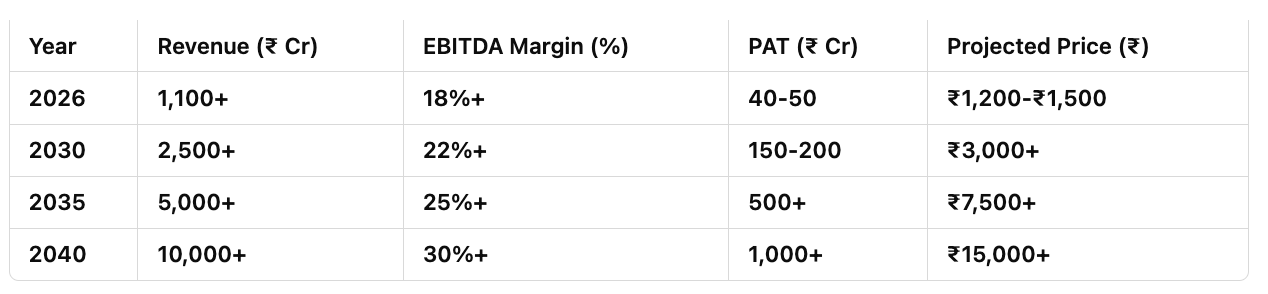

📈 Future Financial Projections & Expected Returns

📢 Bull & Bear Case Scenarios

🔷 Bull Case: ✔ Strong execution on defense, aerospace, & AI contracts ✔ **EBITDA margin expansion from 14.6% to 22%+ ✔ Re-rating due to defense sector tailwinds ✔ Global defense offsets unlocking high-value contracts

🔻 Bear Case: ⚠ Execution delays in high-value defense projects ⚠ ESAI expansion hurdles & slower-than-expected AI adoption ⚠ Valuation concerns (P/E 70.9) if earnings fail to scale

💰 Investment Thesis & Valuation Estimate

📌 Current Valuation:

P/E 70.9 is expensive, but justified with 50%+ EBITDA growth expectation

As profits scale, P/E compression to ~30-35 range is expected

📌 Investment Outlook:

Short-Term (1-2 Years): 50-70% upside if execution is strong

Long-Term (5+ Years): Potential ₹3,000+ stock price (~3x upside)

Ultra-Long-Term (15+ Years): ₹10,000+ stock if AI & Defense scale massively

📢 Investor Takeaway: AXISCADES is a high-risk, high-reward play on India’s defense & AI sector. Investors should closely monitor execution on defense & AI projects before aggressive positioning.

🚀 Verdict: Potential ₹3,000+ multibagger by 2030, but execution risk remains key.

📜 Disclaimer

This newsletter is for informational purposes only and does not constitute investment advice. Readers should conduct their own research before making investment decisions.