Astral Ltd Stock Analysis: India’s Leading Plumbing & Adhesives Company | Future Growth & Risks

Section I: Investment Thesis & Summary

This is a quality compounder that’s quietly built a near-unassailable position in India’s building materials space — particularly in high-margin CPVC plumbing pipes — and the market is still not fully pricing in how durable that moat is.

Yes, the stock looks expensive at first glance. A P/E north of 77x isn’t something you shrug off. But strip away the noise — a soft Q1 FY26, some raw material headwinds, and macro jitters in the construction sector — and what you’re left with is a business that consistently grows volumes, protects margins, and generates clean cash. That’s rare. That’s worth paying for.

The setup right now is actually attractive. The stock is down about 20% from its 52-week high of ₹1,867. The underlying business hasn’t changed. The long thesis is intact. This is a dip-buy opportunity in a business that doesn’t come cheap very often.

Section II: Business Model & Operations

Simply put — this company makes the pipes inside your walls, the tanks on your terrace, the adhesives holding tiles in place, and increasingly, the paint on your walls too.

The core business is pipes and fittings, accounting for about 72% of consolidated revenues. The sweet spot here is CPVC (Chlorinated Polyvinyl Chloride) — a premium grade of plumbing pipe that handles hot water, is corrosion-resistant, and commands meaningfully better margins than regular PVC. They’re among India’s top two players in CPVC. That’s not a position you walk into — it took 25 years to build.

The second leg is Adhesives and Paints, a more recent diversification play. The adhesives and sealants business (under brands acquired through Resinova and Seal IT) serves both construction and industrial segments. Paints are still in build mode — the company entered via the Gem Paints acquisition in 2022 — and while it’s a capital-intensive, long-gestation bet in a category dominated by giants, management is clearly in this for the 10-year game.

What’s happening operationally right now is interesting. The company signed an agreement to acquire 80% stake in Nexelon Chem — essentially backward integrating into CPVC resin production. This is a ₹150 crore project, set to produce 40,000 metric tonnes annually once commissioned in Q2 FY27. That’s a big deal. Right now, CPVC resin is imported, which means raw material cost exposure. Nexelon changes that math structurally, and over time, should give them better margin control.

Volume momentum in the plumbing segment is strong — Q2 FY26 volumes grew 20.6% year-on-year. That’s not a fluke. The infrastructure push in India, urban housing demand, and the Jal Jeevan Mission (piped water to rural India) are all creating a multi-year demand runway for quality piping systems.

Youtube Link:

Section III: Historical Financial Review

Let’s talk numbers — but in plain terms.

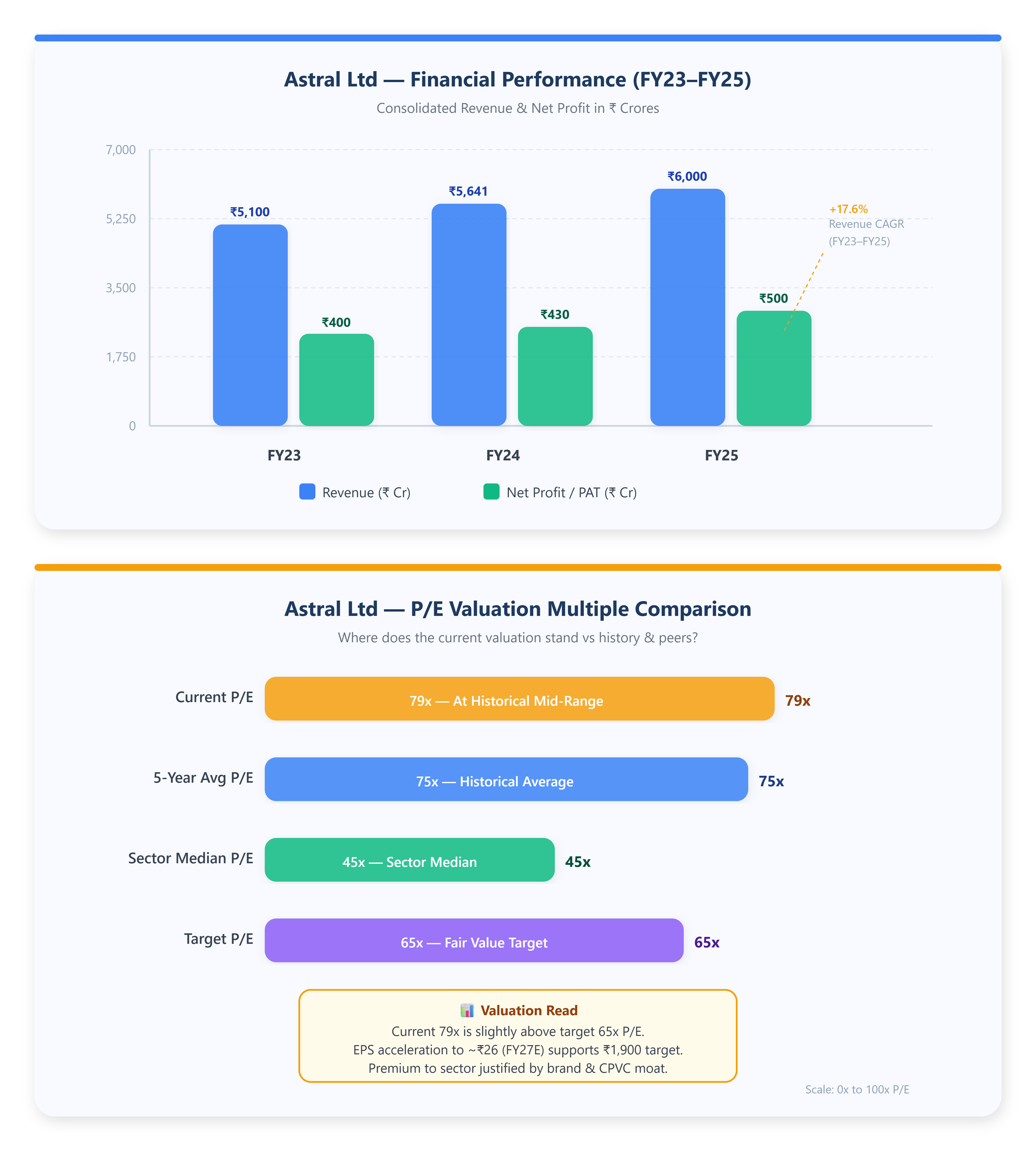

Revenue Story: Revenue for FY23 came in at approximately ₹5,100 crores. FY24 grew to ₹5,641 crores. FY25 crossed approximately ₹6,000 crores. That’s a 3-year revenue CAGR of roughly 9–10% — not explosive, but steady and consistent. Important context: FY24 was actually a drag year for the pipes sector because PVC resin prices fell sharply, forcing companies to reprice finished goods. The fact that this company still grew through that is telling.

Profitability: FY25 consolidated net profit is approximately ₹500 crores. FY23 was around ₹400 crores. That’s PAT growing at roughly 12–13% CAGR — faster than revenue growth, which means margins are actually expanding at the operating level.

Diluted EPS (LTM): ₹18.79 — a solid number, but the trajectory matters more. EPS has been growing, and with operating leverage kicking in as volumes scale, that ₹18.79 can easily be ₹24–26 by FY27.

Cash Position: The company held cash and bank balances of ₹555 crores as of Q2 FY26. For a ₹40,000 crore business, that’s lean — but they’re also almost entirely debt-free. No debt is a massive advantage in a rising interest rate environment.

Operating Cash Flow Per Share: Roughly ₹22–24 on an LTM basis, actually running slightly ahead of reported EPS — which tells you earnings quality is high. Profits are being converted to cash, not sitting in receivables.

Q3 FY26 Check (Dec 2025): Revenue came in at ₹1,542 crores, up 10% year-on-year. Net profit was ₹107 crores — a 6% dip versus the same quarter last year. Operating margins came in at 15%, slightly below the 16% of Dec 2024. The miss on profits is partly explained by higher depreciation from new capacity additions and some softness in the adhesives segment. Not alarming, but worth watching.

Section IV: Fundamental Valuation Metrics & Investment Call

Let me break down the valuation picture honestly.

P/E Ratio: ~77–79x Yes, that’s expensive. But here’s the thing — this stock has historically traded at 65–90x earnings. The current P/E is bang in the middle of its own historical range. You’re not buying a bargain; you’re buying a fair-to-slightly-discounted quality compounder. The 5-year average P/E is approximately 75x. So at 77x, it’s roughly at par with historical norms. Given the Nexelon integration, volume tailwinds, and earnings acceleration expected in FY27, the entry here is reasonable.

P/B Ratio: ~10.6x The stock trades at 10.6 times its book value (book value: ₹141 per share). This is high in absolute terms, but this is the price you pay for a business with high asset efficiency and strong brand equity built over decades. It’s not a red flag by itself.

ROCE: 19.7% | ROE: 14.9% ROCE of 19.7% is healthy — the business earns well above its cost of capital. ROE at 14.9% is a touch lower than the company’s historical average, partly because of the capital deployed in paints, which hasn’t fully matured. As paints scale, ROE should improve towards 18–20% over the next 3 years.

EPS Growth: Picking Up After a flattish FY24, EPS is back on the growth track. At the current trajectory — 20% volume growth in pipes, margin stability, and cost efficiencies — FY27 EPS of ₹24–26 is a realistic base case. On ₹25 EPS at a target P/E of 65x (a modest derating given growth normalization), fair value is approximately ₹1,625. Apply a premium for the Nexelon integration optionality, and ₹1,900 is a defensible 12–18 month target. That’s ~27% upside from current levels.

Dividend Yield: 0.25% Don’t hold this for dividends. They’ve declared ₹3.75 per share for FY26 so far — symbolic, but consistent. The real return story here is capital appreciation, not yield.

Section V: Long-Term Outlook & Risk Assessment

5-Year Return Estimate: 12–18% CAGR | 10-Year Return Estimate: 14–20% CAGR

Here’s why the long-term compounding case holds.

India is urbanizing at an unprecedented pace. The government is spending aggressively on housing — PMAY, Smart Cities, and Jal Jeevan Mission collectively represent hundreds of billions in infrastructure outlay that eventually requires pipes, tanks, fittings, and adhesives. This company sits right at that intersection.

Growth Levers: The Nexelon CPVC resin plant (FY27 commissioning) is the single most exciting medium-term catalyst. Today, CPVC resin is imported — mostly from Asian manufacturers — and represents a significant raw material cost line. Once Nexelon comes online, the company gains both cost advantage and supply chain resilience. This isn’t just a margin improvement story; it’s a moat-deepening story.

The paints segment is currently dilutive. But this is management playing the 10-year game. With their existing distribution reach (over 200,000 retail touchpoints), and a product portfolio that can cross-sell alongside pipes and fittings, there’s a credible path to a meaningful paints business. Don’t expect profitability here for 2–3 more years — but don’t dismiss it either.

Promoter Holding: 54.2% This is a promoter-driven business, and at 54%, promoters have meaningful skin in the game. No significant selling pressure visible — a reassuring sign of confidence in the long-term trajectory.

Capex: The business is in an elevated capex cycle — new plants, Nexelon, expanded manufacturing. This has pushed depreciation higher (₹72–73 crores per quarter in FY26 vs ₹46 crores in FY23) and is temporarily suppressing reported net profit growth. But this is good capex — it’s building capacity ahead of demand, which is exactly what you want quality compounders to do.

Risks — Let’s Be Real

Raw Material Concentration: Until Nexelon is operational, the company remains exposed to imported CPVC resin prices. A sharp appreciation in the dollar or supply chain disruption could hurt margins quickly.

Competition Intensifying: The pipes and fittings space is attracting more players. Prince Pipes, Supreme Industries, and Finolex are all competing hard, especially in the affordable PVC segment. Pricing pressure in commodity pipe varieties is real.

Paints Segment Drag: Entering a market dominated by Asian Paints and Berger isn’t for the faint-hearted. If paints don’t scale as planned, it could be a multi-year drag on consolidated returns.

Valuation is Not Forgiving: At 77x P/E, there’s almost zero margin of error. A bad quarterly result or a negative management commentary can shave 10–15% off the price overnight, as we’ve seen before.

Slowdown in Real Estate: Any sustained cooling in India’s housing construction activity will directly impact pipe volumes. This risk is real, though current indicators — both government and private sector — remain supportive.

Bottom Line:

This is a quality business in a structural growth sector with a credible 10-year tailwind. It’s not cheap. But it rarely is. The current pullback from highs, combined with strong volume momentum and the Nexelon integration optionality, makes the risk-reward here compelling for investors with a 3-year or longer horizon.