Anand Rathi Wealth: Strong Growth Trajectory Amid Expanding Wealth Management Opportunity

Financial Health: Robust Profitability and Growth

Anand Rathi Wealth Limited (ARWL) has demonstrated exceptional financial performance in FY25. The company reported:

Revenue growth: 30.4% YoY increase to ₹981 crores

PAT growth: 33.2% YoY increase to ₹301 crores

Profitability metrics:

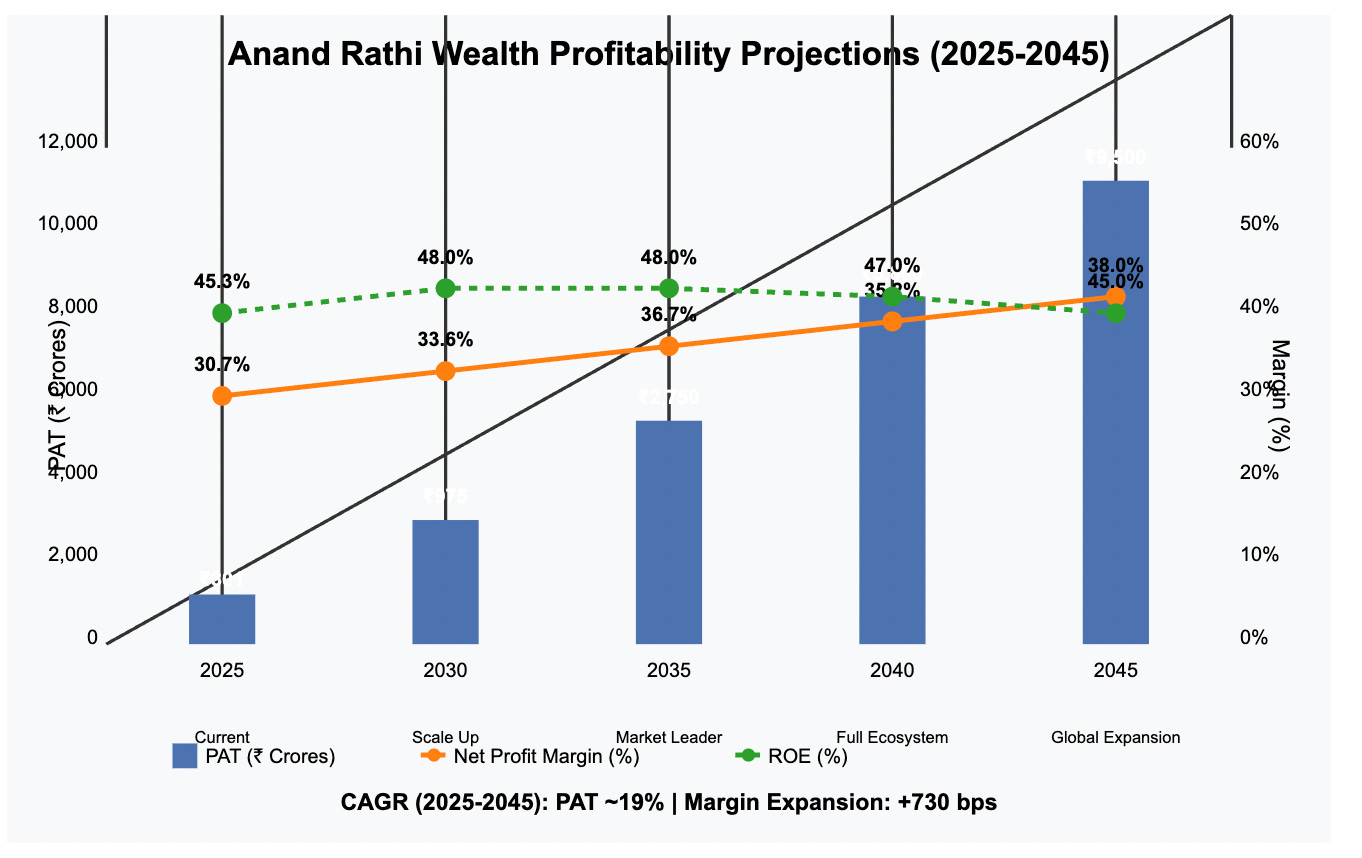

Net profit margin of 30.7% (improved from 30.0% in FY24)

Operating margin (OPM) of 42.6%

PBT margin of 41.3% (improved from 40.6% in FY24)

The company's debt position remains conservative with total debt of ₹79.3 crores against a healthy equity base, resulting in a low debt-to-equity ratio. With strong cash equivalents of ₹44.1 crores, ARWL maintains solid liquidity.

Valuation Assessment: Premium Valuation Reflecting Growth

ARWL currently trades at premium multiples that reflect its strong growth trajectory:

P/E ratio: 49.0x (significantly higher than industry average, reflecting premium growth)

P/S ratio: 15.6x (based on market cap of ₹14,684 crores and sales of ₹939 crores)

PEG ratio: ~1.5x (assuming 33% growth rate)

The high valuation multiples indicate investor confidence in the company's growth potential and business model, though they also suggest expectations for continued strong performance.

Growth Projections

Business Strength Indicators: Impressive Capital Efficiency

ARWL demonstrates exceptional capital efficiency metrics:

ROE: 45.3% (indicating highly efficient use of shareholder capital)

ROCE: 56.3% (showing strong returns on total capital employed)

The company's AUM grew impressively by 29.9% YoY to ₹77,103 crores as of March 2025, demonstrating strong business momentum. Key operational strengths include:

Client base expansion to 11,732 client families (18.4% YoY growth)

Extremely low client attrition rate of 0.52% for FY25 (improved from 0.99% in FY24)

Growing relationship manager count to 380 (14.5% YoY increase)

Consistent growth in AUM per relationship manager to ₹198 crores (13.8% YoY growth)

Industry Context: Well-Positioned in Growing Wealth Management Space

ARWL is strategically positioned in India's rapidly growing wealth management sector:

India's HNI population is projected to grow at 15.7% CAGR from 2022 to 2027

Mutual fund penetration in India (equity AUM to GDP ratio of 9.2%) remains significantly below global average (32.4%), indicating substantial growth runway

The company has expanded to 17 major Indian cities plus a representative office in Dubai

The company is targeting the higher-reward HNI segment, focusing on clients with financial assets between ₹50 lakhs and ₹5 crores. This segment offers better sustainability and scalability.

Risk Evaluation: Limited Concerns Amid Strong Positioning

Key risks to consider include:

Valuation risk: The high P/E multiple of 49x could face pressure if growth slows

Market dependency: Performance heavily tied to equity market conditions

Competitive intensity: Wealth management industry faces increasing competition from established players and new entrants

However, the company has demonstrated resilience through:

Low client attrition rate of 0.52%

Strong client vintage with 79% of clients having relationships longer than 3 years

Disciplined management execution with consistent outperformance against guidance

Forward Outlook: Ambitious Growth Targets

Management has provided strong guidance for FY26:

Revenue target: ₹1,175 crores (19.8% YoY growth)

PAT target: ₹375 crores (24.6% YoY growth)

AUM target: ₹100,000 crores (29.7% YoY growth)

The company has consistently outperformed previous guidance, enhancing credibility of their forward projections. ARWL is also diversifying revenue streams through:

Digital Wealth initiative targeting mass affluent segment (₹10 lakhs to ₹5 crores)

OFA platform leveraging technology to serve retail segment

Key Investment Takeaways

Consistent outperformer: ARWL is among only six companies in India's top 1,000 listed entities achieving 20%+ YoY growth every quarter since listing in December 2021

High capital efficiency: Exceptional ROE (45.3%) and ROCE (56.3%) demonstrate superior capital allocation

Structural growth story: Well-positioned to benefit from India's expanding wealth management opportunity with significant runway ahead

Shareholder-friendly: Consistent dividend payouts (₹14 per share for FY25) and completed share buyback program

Premium valuation justified by growth: While trading at high multiples, the company's consistent growth trajectory and execution support the premium

Execution excellence: Management has consistently outperformed guidance, building credibility for future projections

ARWL represents a quality play on India's wealth management growth story, supported by strong execution, client loyalty, and expanding market opportunity, though investors should be mindful of the premium valuation.