Profit Jumped 648%. The Market Didn’t Even Notice.

A company just posted 648% profit growth. Not 64%. Not 164%. Six hundred and forty-eight percent.

Revenue grew a quiet 22%. Margins didn’t just improve — they structurally reset. EBITDA tripled. Net profit went from an afterthought to a statement.

And the market? Dead silent. No buzz. No analyst note. No breakout on the charts.

That silence is either the biggest warning sign — or the biggest opportunity. Let’s find out which.

Section 1

One-line insight: When a business this small prints a 19% net margin and 21% EBITDA margin in the same quarter — it's not an accident. Something structural just changed.

Section 2 · What the Market Is Missing

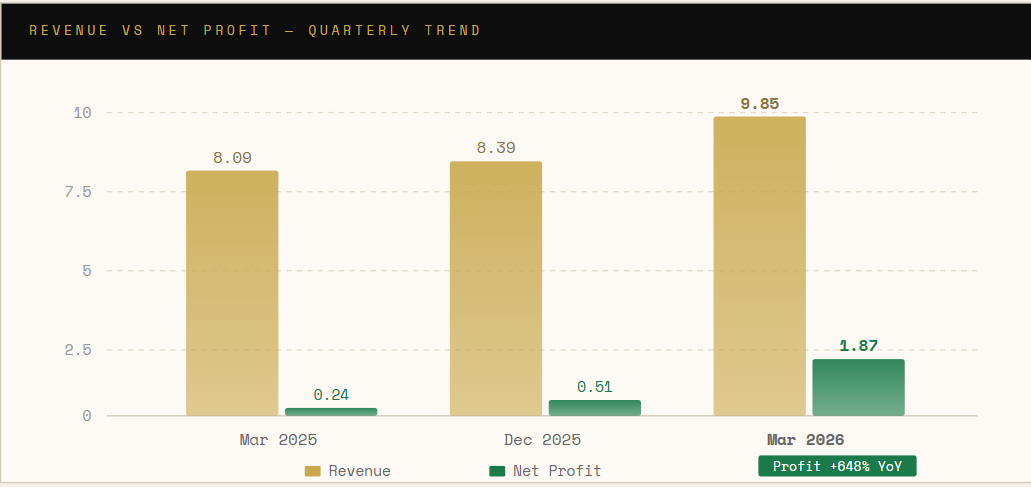

Here’s why this stock sits in the shadows: the revenue number looks small. ₹9.85 crore in a single quarter. Most institutional desks won’t even glance at something this size. The screeners auto-filter it out. Analyst coverage? Essentially zero.

But that’s exactly the market’s mistake.

They’re looking at the revenue — ₹9.85 crore — and dismissing it. They’re not looking at what happened inside that revenue. EBITDA margins at 21.5%. Net margins at 19%. A year ago, this business was barely scraping 9% EBITDA and sub-3% net margins.

The misunderstood truth: This isn’t a growth story yet. It’s a margin inflection story. And margin inflections precede growth reratings — almost every time.

The quarterly profit was ₹24 lakhs just a year ago. Now it’s ₹1.87 crore. People see that jump and assume it’s a one-quarter aberration. But look at the sequential trend: Dec quarter already showed ₹51 lakhs, up from Mar 2025’s ₹24 lakhs. This isn’t a spike. It’s a staircase — and the last step was a leap.

The market is ignoring it because it doesn’t fit a comfortable pattern. Too small to screen. Too fast to believe. That’s where the opportunity hides.

Youtube Link:

Section 3 · Business Simplified

This is a B2B industrial manufacturer. It makes specialty components — the kind of product that sits inside larger systems, unseen by end consumers, but absolutely critical to the buyer’s operations.

Who pays them? Industrial customers, manufacturers, and project-based buyers who need precision-spec components. These aren’t one-time retail transactions. These are repeat, relationship-driven orders. Once a customer qualifies your product, switching is expensive and operationally risky.

Why it’s sticky: In B2B industrial supply, re-qualification costs are high. A customer doesn’t switch a vendor just because a competitor is ₹2 cheaper. They switch when they absolutely must. That’s a moat — small but real.

The business model has fixed costs that don’t scale linearly with revenue. As volumes grow, profits grow faster. That’s exactly what the numbers are showing. Revenue grew 22%. Profit grew 648%. The gap between those two numbers is the story.

Section 4 · Financial Momentum

Revenue trend: Slow, steady, and now accelerating. ₹8.09 Cr → ₹8.39 Cr → ₹9.85 Cr. The March quarter showed the sharpest sequential jump. Pipeline is converting.

Profit trend: Explosive. ₹0.24 Cr → ₹0.51 Cr → ₹1.87 Cr. Each quarter better than the last. Not a one-off. A trend.

Margins: This is where the story gets powerful. EBITDA margin has gone from 9.3% to 21.5% in three quarters. Net margin from 3% to 19%. This is operating leverage at work — fixed costs being diluted by growing revenue while pricing power holds.

This is not just a profit improvement.

It’s a cost structure reset.

The machine is now running hot — without adding proportional costs.

Section 5 · Key Triggers

What could move this stock from “unnoticed” to “repriced”? These are the levers:

📦Volume Scale-UpRevenue growing at 22% is fine. But at 30–35%, the operating leverage becomes violent. Every rupee of incremental revenue above fixed costs flows almost entirely to the bottom line.

🔍Discovery by Small-Cap FundsOne well-watched fund adds this to their portfolio — even in a small position — and suddenly it’s on every retail radar. At this size, it only takes ₹5–10 Cr of buying to move the stock meaningfully.

📋Order Book VisibilityAny disclosure of a large order or multi-year contract would reframe this from a one-quarter story to a multi-year story instantly.

📈Sustained Margin MaintenanceIf Jun 2026 quarter prints similarly — even 15%+ net margin — the market can no longer call this a fluke. That’s the confirmation event.

🏭Capex Signal or Expansion AnnouncementManagement signaling capacity expansion would confirm they see demand visibility. That changes the narrative from turnaround to growth story.

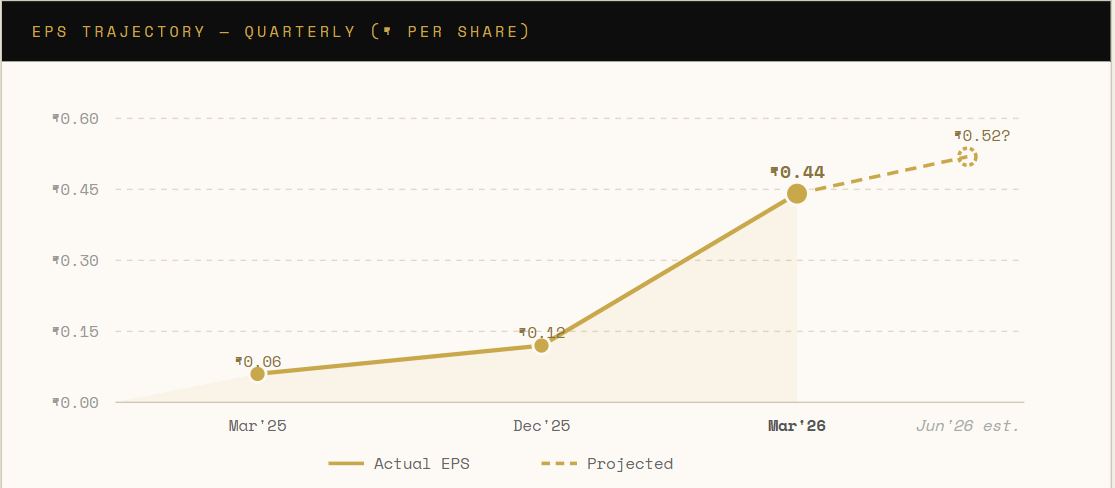

📈 Earnings Momentum Projection

Section 6 · Smart Money Signal

You won’t find flashy headlines here. But the signals are real for those who look.

📊Margin Velocity

Margins at this level, in a business this small, suggest pricing power or cost renegotiation — either way, management is in control of the numbers, not a prisoner of them.

🔁Consistent Sequential Improvement

Three consecutive quarters of improvement — from ₹0.24 Cr to ₹0.51 Cr to ₹1.87 Cr — is not noise. That’s a trend. Noise doesn’t follow a pattern.

🪣Low Float Advantage

Micro-caps with improving fundamentals often sit idle for months — then move violently when one large buyer enters. The float is small. The trigger won’t need much.

⚙️Operating Leverage Signal

Revenue grew 22%. Profit grew 648%. The gap in those two numbers tells you fixed costs are largely covered. Incremental revenue is now almost entirely profit.

Section 7 · Risks — No Sugarcoating

It’s a micro-cap. Liquidity is thin.Buying at the wrong time — or trying to exit in a hurry — can be painful. Bid-ask spreads can be wide. Price discovery is poor.

One quarter does not a trend make.The Jun 2026 result is the real test. If margins compress sharply, this entire thesis collapses. Confirmation is mandatory before meaningful allocation.

Business concentration risk.At ₹40 Cr annual revenue scale, the loss of one or two key customers can materially impact results. Diversification may be limited.

No public analyst coverage means no warning system.Negative developments may not surface quickly. Investors need to monitor quarterly filings themselves — there’s no broker alert network here.

The profit jump may have a one-time component.Until full annual accounts are analysed, it’s worth checking if there are any exceptional or non-operating income items baked into the ₹1.87 Cr figure.

Section 8 · Final Verdict

This is not a stock you buy today and forget about. It’s a stock you watch closely starting today.

Here’s the thesis in one sentence: a small industrial business has quietly crossed the fixed-cost hurdle, and every rupee of new revenue is now printing profit at a velocity the market hasn’t priced in yet.

The Jun 2026 quarter result is your verification event. If EBITDA margins hold above 15% and net profit stays above ₹1 Cr, the story is real. At that point, re-rating becomes a question of when, not if.

Opportunities like this don’t announce themselves. They’re found in the filings that nobody reads, in the companies nobody covers, in the quarters that slip by unnoticed.

This is one of those quarters.