5 Money Mistakes Freshers Regret

Real Stories from Bengaluru & Delhi Tech Parks

Dear Wealth Warriors,

Last week, we explored how starting early can transform ₹500 into crores through the magic of compounding. Today, we're shifting gears for a much-needed reality check.

We interviewed 50 young professionals across Bengaluru's tech corridors and Delhi's corporate hubs. The findings? A staggering 80% regretted the same five financial missteps within their first few years of employment.

Let's dive into these stories—so you don't have to learn these lessons the hard way. After all, galtiyon se seekhna hi asli wealth hai (learning from mistakes is the real wealth).

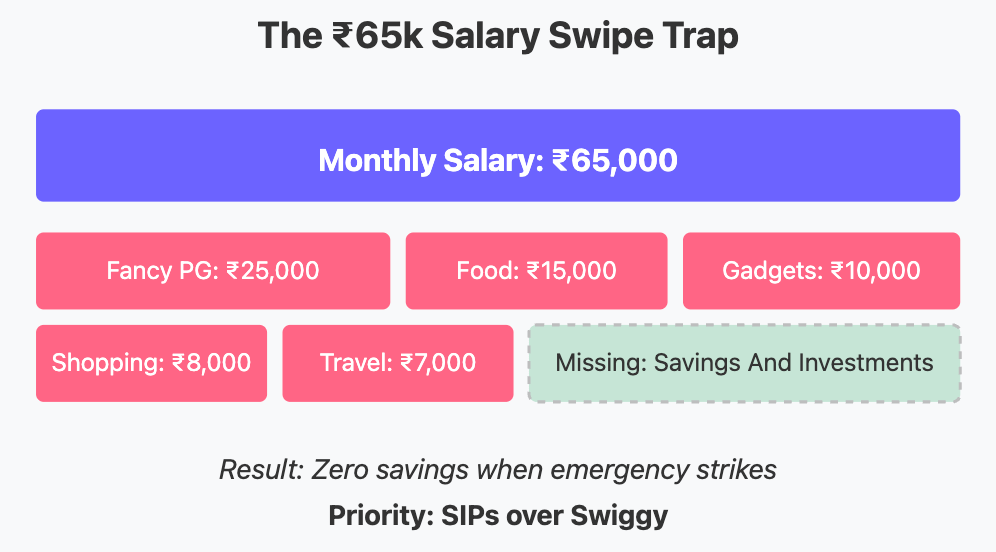

Mistake #1: Lifestyle Inflation – 'The ₹50k Salary Swipe Trap'

Meet Ananya, 23, a software developer in Bengaluru. First salary: ₹65,000. By month three, her expenses looked like this:

₹25,000 on rent for an 'Instagram-worthy' PG in Koramangala

₹15,000 on food delivery and café-hopping

₹10,000 on a fitness band she barely used after the first week

The Result? Zero savings. When her laptop broke down before a critical project deadline, she had to make the embarrassing call to her parents asking for ₹40,000.

"I thought I was investing in my happiness, but really, I was just following what my peers were doing. Now I'm back to square one, but with a bigger appetite," she confesses.

Key Takeaway: 'Lifestyle upgrades' are wealth's slow poison. Your first few years of earning are crucial for building habits, not depleting resources. Prioritize SIPs over Swiggy.

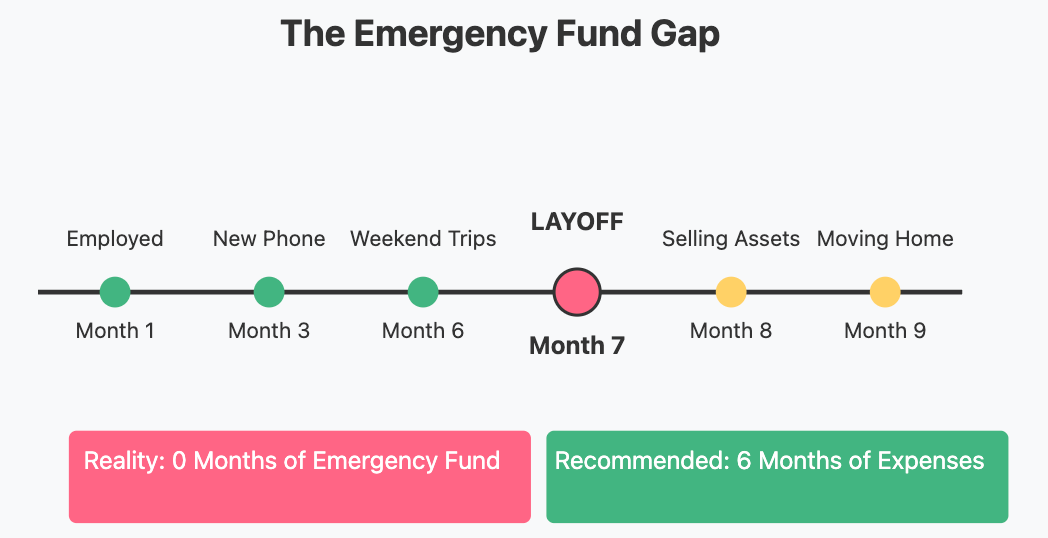

Mistake #2: Ignoring Emergency Funds – 'The Delhi Job-Loss Disaster'

Emergency Fund Visualization

Rahul, 24, from Delhi, earned ₹55,000 monthly at a promising fintech startup. His spending pattern:

Weekly clubbing in Hauz Khas: ₹12,000/month

Latest iPhone on EMI: ₹8,000/month

Designer clothes: ₹10,000/month

Then, the inevitable happened. Tech layoffs hit his company in early 2025. With zero emergency fund, he faced hard choices:

Sold his iPhone at a 50% loss

Moved back with his parents in Ghaziabad

Cancelled attending his college friend's destination wedding due to financial embarrassment

"I thought job security was guaranteed with my skills. Now I understand why my father always kept a separate emergency account. It's not just about money—it's about dignity," Rahul reflects.

Key Takeaway: Before buying that PS5 or booking that Goa trip, secure 6 months of living expenses in a separate liquid fund. Job security in 2025's tech landscape is a myth.

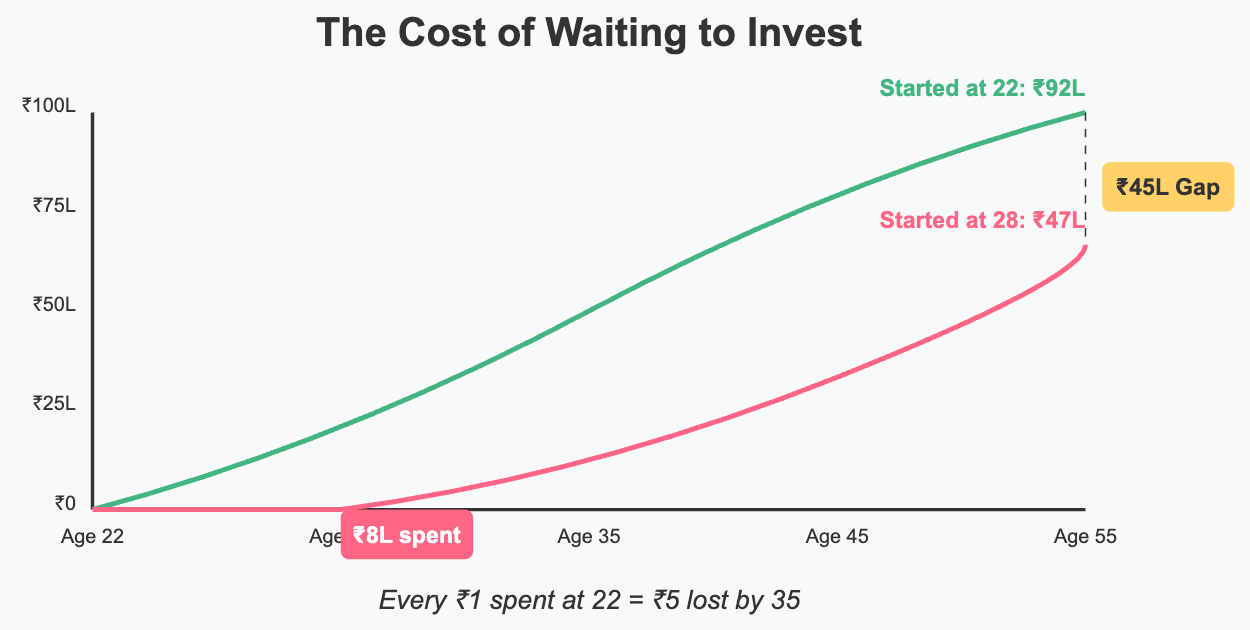

Mistake #3: 'I'll Invest Later' – The ₹10L Regret

Cost of Delayed Investing

Priya, now 28, works as a UX designer in Bengaluru. Her early career philosophy was clear: "Pehle enjoy karte hain, baadme invest karenge." (Let's enjoy first, we'll invest later.)

By her estimation, she spent roughly ₹8 lakhs over 6 years on:

Weekend getaways to Coorg and Goa

The latest MacBook and iPad Pro

Designer clothing and dining experiences

The sobering math: Had she invested that ₹8 lakhs in a diversified equity fund with 12% returns, she would be looking at approximately ₹22 lakhs by age 30.

"I now realize time is the soil in which money grows. I can always earn more, but I can never get back those early years of compounding," Priya laments.

Key Takeaway: Every ₹1,000 you spend today on non-essentials is potentially ₹5,000 less in your future. The YOLO (You Only Live Once) mindset comes with a hefty price tag that compounds negatively over time.

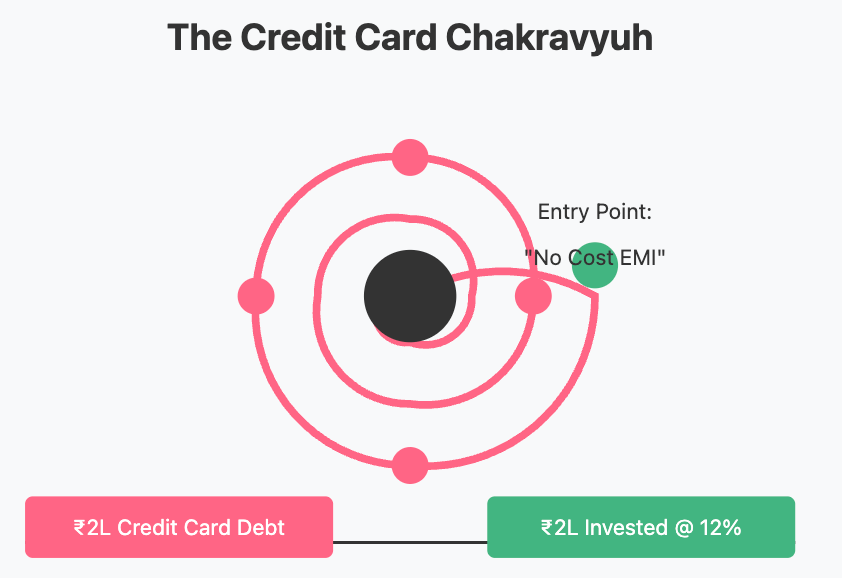

Mistake #4: Taking on Bad Debt – 'The Credit Card Chakravyuh'

Credit Card Debt Trap

Arjun, 25, a Delhi-based graphic designer, fell for the classic trap: "No Cost EMI" offers that seemed too good to be true—because they were.

His story began with a new iPhone purchase that quickly spiraled:

Initial purchase: ₹79,000 on "No Cost EMI"

Processing fees (hidden in fine print): ₹3,500

Missed one payment: ₹1,200 late fee + interest

Additional impulse purchases (because "credit limit available"): ₹1.2 lakhs

Before he knew it, Arjun was ₹2 lakhs in debt with a crushing 24% annual interest rate.

"The morning UPI requests from debt collectors became my alarm clock. I was earning for the bank, not for myself," Arjun shares.

After 10 months of aggressive repayment and cutting all discretionary expenses, he finally escaped the debt trap—but not before paying nearly ₹40,000 in interest alone.

Key Takeaway: If you want to own gold, invest in SIPs, not EMIs. The same ₹15,000 monthly payment that drowns you in consumer debt could be building a solid investment portfolio instead.

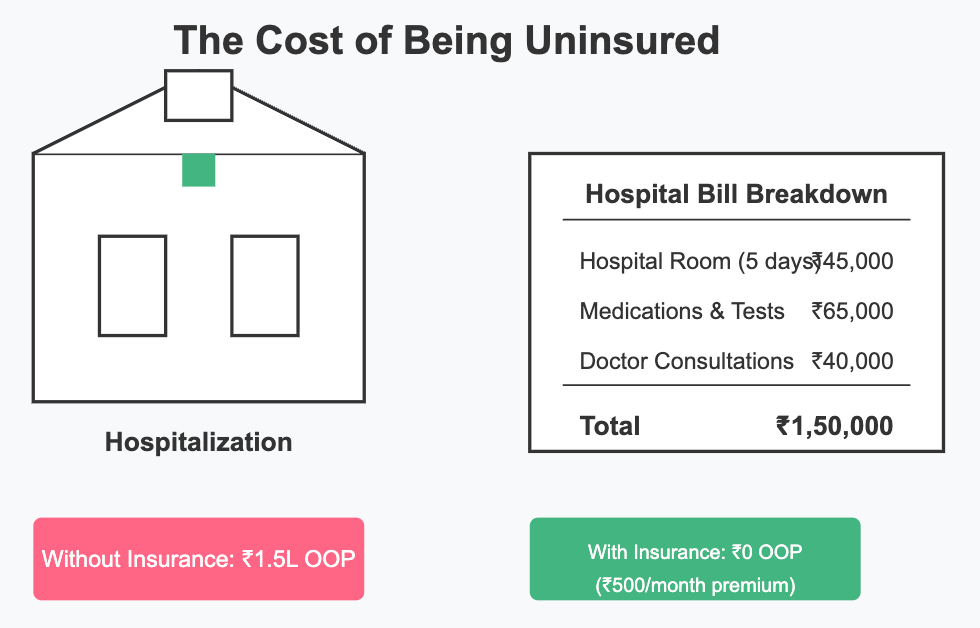

Mistake #5: Not Insuring Health – 'The Bengaluru Hospital Nightmare'

Health Insurance Impact

Sneha, 26, a content strategist in Bengaluru, had a simple philosophy about health insurance: "I'm young, fit, kyu paisa waste karu?" (Why waste money on it?)

Then dengue season hit Bengaluru hard in 2024. After ignoring early symptoms, she ended up hospitalized for 5 days with severe complications.

The financial damage:

Hospital bill: ₹1.5 lakhs

Lost income from unpaid sick leave: ₹45,000

Months to rebuild depleted savings: 8

"Calling my parents to ask for money at 26 was more painful than the IV needles. I realized that health insurance isn't an expense—it's protection for my dignity and independence," Sneha says.

Key Takeaway: A basic health insurance plan costs ₹500-1,000 monthly—less than two food delivery orders. Yet it's the difference between financial stability and distress during health emergencies. In 2025's healthcare landscape, going uninsured is gambling with both health and wealth.

Your Wealth Warrior Action Steps

Track last month's expenses: Use apps like Walnut or Money Manager to categorize where your money went. How much went to needs vs. wants? Aim for the 50/30/20 rule (50% needs, 30% wants, 20% savings).

Start an emergency fund today: Open a separate savings account or liquid fund with auto-transfers on salary day. Target: 1 month's expenses within 90 days, 6 months' within a year.

Insure your health immediately: Apps like PolicyBazaar or Digit can get you covered in under 15 minutes. A ₹5 lakh cover costs roughly the same as one weekend outing—but delivers lifelong protection.

Audit your debt: List all credit cards, loans, and EMIs with their interest rates. Attack the highest-interest debt first, and avoid new consumer debt entirely.

Final Thoughts

Remember, Wealth Warriors: Financial mistakes are only failures if you don't learn from them. The best investment decisions are often the boring ones—systematic, consistent, and patient.

Next week, we'll tackle "Student Loans vs. SIPs: Which Should Come First?" Subscribe for our free "Emergency Fund Calculator" to determine exactly how much you need based on your lifestyle.

Until then, remember: Aaj ka sacrifice, kal ka crorepati! (Today's sacrifice makes tomorrow's millionaire!)

Keep growing,

Value Picks

Did you find this valuable?

If so, please consider:

Sharing this newsletter with that friend who's always "just one swipe away" from financial trouble

Commenting below with your own financial regret story

Joining our Telegram community for daily money tips and accountability