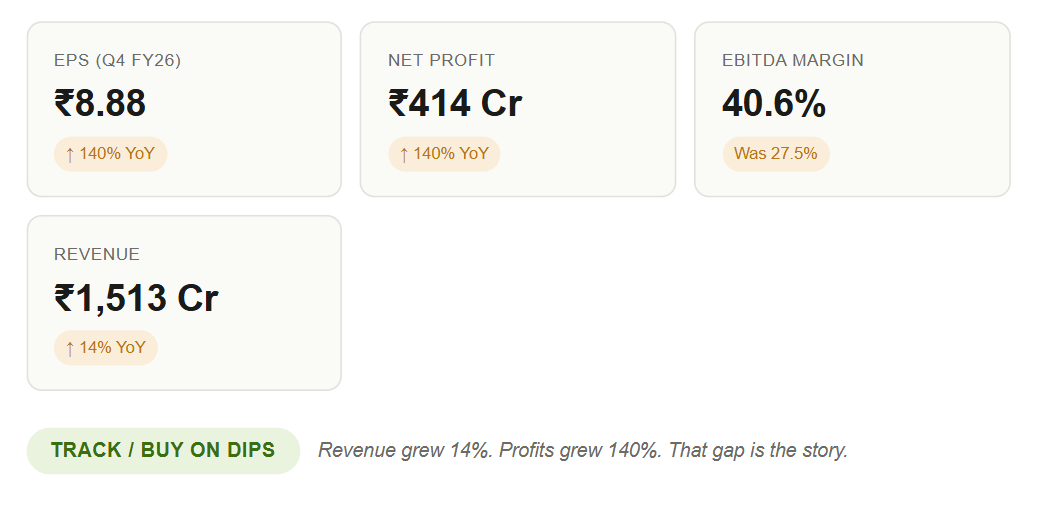

140% Profit Jump. Zero Hype. That's The Setup.

Three ships are at sea right now. One carries crude oil. One carries chemicals. One carries soldiers.

All three are owned by the same company — one most investors have written off as “just another PSU.”

In March 2026, that company just made 140% more money than it did a year ago.

And almost nobody is talking about it.

Section 01 — Quick Snapshot

The Numbers at a Glance

Section 02 — What the Market Is Missing

The Misunderstanding That Creates Opportunity

Most investors see three letters — PSU — and stop reading. That’s the gift.

They remember a bloated government company from a decade ago. Slow decisions. Aging ships. Bureaucratic fog. They extrapolate that memory forward and miss what’s actually happening in the numbers.

Here’s what they’re missing: Revenue grew 14%. Fine. Respectable. Forgettable. But EBITDA grew 68%. And net profit grew 140%. In one year. That is not a commodity company getting lucky. That is operating leverage kicking in — and when it starts, it compounds quietly before anyone notices.

They also miss the structural angle. This company operates at the intersection of India’s two most inelastic demands — energy imports and national security logistics. Neither of those goes away in a downturn.

The margin expansion tells the real story. A business that was earning 27.5% EBITDA margin a year ago is now printing 40.6%. That is not freight rates alone. That is a business hitting operating efficiency at scale — fixed costs absorbed, utilization up, pricing power quietly improving.

Youtube:

Section 03 — Business Simplified

What This Company Actually Does

India imports over 85% of its crude oil. All of it needs to cross the ocean. Most of it moves on ships. This company owns and operates many of those ships — and is the only Indian company with the scale, the fleet, and the government mandate to do it at this level.

Who pays them? IOC, HPCL, BPCL — India’s state oil refiners. ONGC for offshore logistics. The Ministry of Defence for strategic naval support. These are not customers who switch vendors. These are customers who cannot switch vendors easily.

Why is it sticky? Three reasons. First, cabotage laws give this company preferential rights on coastal cargo. Second, government entities have standing instructions to use Indian-flagged vessels where possible. Third, you cannot build a competing fleet in 12 months. Ships take years to order, build, and certify.

It is not a fast business. It is a durable business. And durable, right now, is being mispriced.

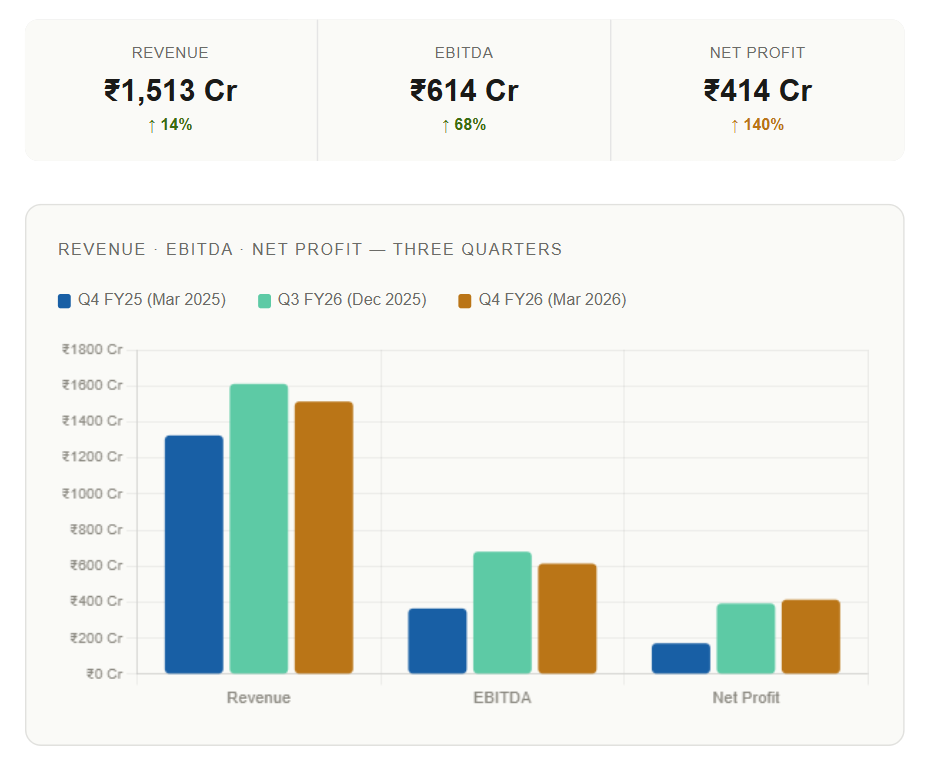

Section 04 — Financial Momentum

The Numbers Are Not Subtle

Look at this sequentially. Mar 2025, the company earned ₹172 Cr net profit on ₹1,325 Cr revenue. Nine months later, Dec 2025, it earned ₹393 Cr. Three months after that, ₹414 Cr.

Revenue is growing steadily. Costs are not keeping pace. The gap between top-line and bottom-line is widening in the right direction. This is the shape of margin expansion — gradual on the revenue side, explosive on the profit side.

📊 Growth Snapshot — Q4 FY26 vs Q4 FY25

This is not just a shipping business.

It is India's strategic maritime infrastructure.

The government cannot afford to let it fail.

That makes the downside asymmetric.

Section 05 — Key Triggers

What Moves This Stock From Here

1

Freight Rate Cycle — Sustained or Extended

Global shipping rates remain elevated. Every quarter they hold, the earnings beat consensus. Every quarter they beat, analysts scramble to revise upward.

2

Fleet Expansion Announcement

New ship orders signal long-term confidence. This company has been discussing fleet renewal for years. An announcement would re-rate the stock from “turnaround” to “growth story.”

3

Disinvestment / Strategic Sale

Government has flagged this as a disinvestment candidate. Even a partial stake sale to a strategic partner would unlock a valuation re-rating instantly.

4

India’s Energy Transition — LNG Fleet

India’s LNG imports are set to triple by 2035. This company is uniquely positioned to add LNG tankers. That is a 10-year tailwind hiding in plain sight.

5

Cabotage Policy — Coastal Cargo Expansion

Any policy move to expand Indian-flagged ship mandate for coastal cargo is pure earnings upside — no capital required, immediate revenue.

Section 06 — Smart Money Signal

What the Quiet Money Is Doing

Delivery-based buying has been consistently rising over recent quarters — a signal of conviction-based accumulation versus speculative trading.

FII stake has been creeping upward. Not dramatically — quietly. That is often how the smartest money enters: slowly, before the story breaks wide open.

The promoter — the Government of India — has not sold a single share despite holding 63%+. At these profit levels, they are either patient or they know something the street does not.

A stock with 140% profit growth and expanding margins that is still trading at a single-digit P/E is either a trap — or it is the opportunity. The business fundamentals here argue strongly for the latter.

Section 07 — Risks

What Can Go Wrong

R1

Freight Rate CollapseShipping is cyclical. If global freight rates normalise sharply, margins compress fast. The 40% EBITDA today could revert to 25-27% quickly. The 140% profit growth disappears.

R2

Aging Fleet — Rising CostsSeveral vessels in the fleet are old. Maintenance costs will rise. Insurance costs too. If revenue stays flat and costs rise, the margin story reverses painfully.

R3

PSU Decision-Making SpeedBureaucratic execution risk is real. Fleet expansion decisions that should take months take years. Capital allocation efficiency at PSUs is structurally poor.

R4

Disinvestment Delay or CancellationThe privatization story has been “imminent” for four years. If it gets shelved again, the re-rating catalyst disappears. Government plans change. Always.

R5

Global Trade SlowdownIf global trade volumes contract sharply — recession, geopolitical trade disruption — charter rates fall across all segments and this business takes a significant hit.

Section 08 — Final Verdict

Why You Should Be Tracking This

A business just doubled its profits. Its EBITDA margin expanded from 27% to 40% in twelve months. Its EPS went from ₹3.70 to ₹8.88.

And the market largely looked away.

That disconnect — between what the numbers say and what the price reflects — is where opportunity lives.

This is not a speculative bet on a startup. It is a cash-generating, strategically essential, government-backed infrastructure business that has just demonstrated it can dramatically improve profitability. That does not happen by accident.

The risks are real — freight cycles turn, PSUs move slowly, disinvestment timelines slip. Respect all of that. But the question you should be asking is: how many stocks do you know that just printed 140% profit growth with expanding margins and are still trading at distressed valuations?

Not many. That is precisely why this deserves a place on your watchlist — if not your portfolio.