126% Revenue Jump. Nobody's Noticed.

Sales nearly doubled year-on-year. EBITDA jumped 369%. EPS crossed ₹17.77 in a single quarter.

And yet — most retail investors have never heard the name. No TV anchor is shouting about it. No Telegram channel is pumping it.

This is a company that does one of the most difficult things in tech — and does it quietly. The kind of business that compounds in silence while the market chases noise.

Read this till the end. The reveal might change how you think about the sector.

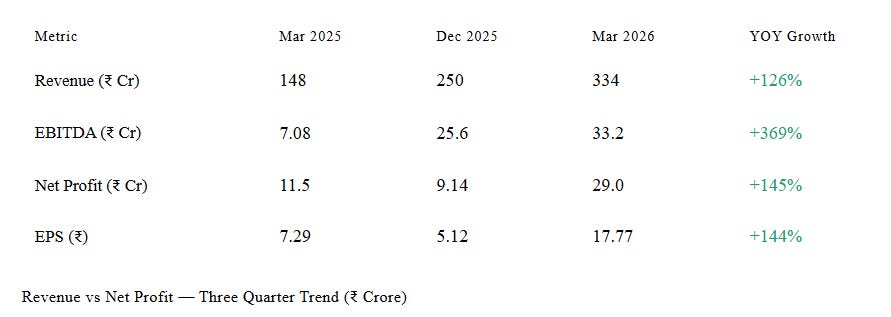

Section 1 — Quick Snapshot

This is a stock where the earnings acceleration has just started showing up in the numbers — the market often takes 2–3 quarters to reprice such re-ratings.

Section 2 — What the Market Is Missing

Here’s the paradox: this company operates in a space that everyone wants to invest in — semiconductors, automotive electronics, connected devices — but nobody thinks to look here.

Why? Because it’s not a product company. It doesn’t have a chip with its name on it. It doesn’t sell a consumer gadget. It lives deeper in the stack — at the layer where real engineering happens.

The market mistakes “invisible” for “irrelevant.” That’s the mispricing. The clients who depend on this company don’t switch vendors easily. The work is deeply technical, relationship-driven, and hard to replicate. This is embedded stickiness — the kind you can’t buy with a sales pitch.

And the numbers from March 2026? They’re not a one-quarter blip. They reflect a structural shift in deal sizes and client mix — something that takes years to build. The market just hasn’t connected the dots yet.

Youtube:

Section 3 — Business Simplified

What they do: They engineer the software brains inside chips, devices, and connected systems. Think automotive cockpits, wireless chipsets, semiconductor firmware, consumer electronics platforms. They are the silent engineers behind products you use every day — products that don’t carry their name anywhere.

Who pays them: Global semiconductor leaders, automotive OEMs, and device manufacturers — headquartered in the US, Europe, and Japan. Dollar-denominated contracts. Multi-year engagements.

Why it’s sticky: They don’t just write code — they embed themselves into a client’s product roadmap. Switching vendors means re-onboarding a new team to years of technical context. That’s painful. Most clients don’t even try. This is the definition of engineering lock-in.

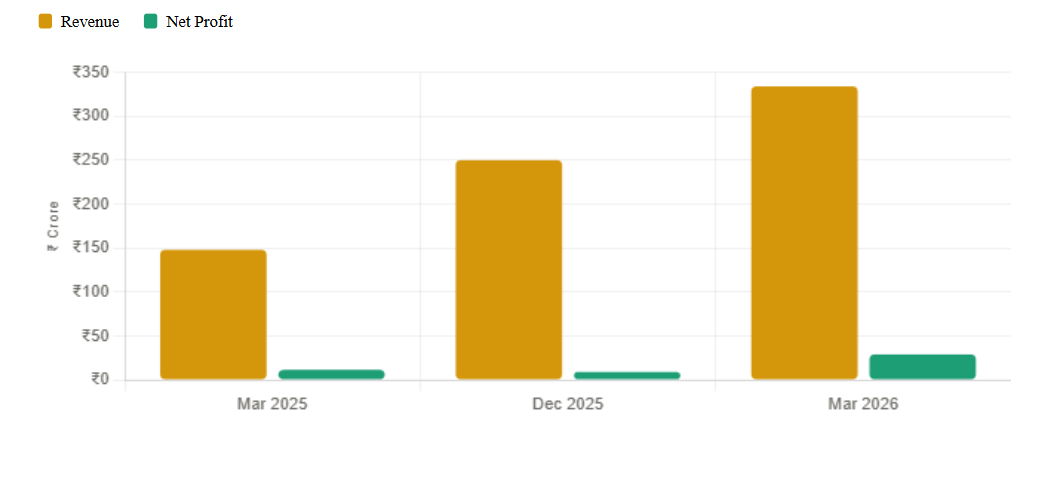

Section 4 — Financial Momentum

The numbers tell a story of genuine operating leverage kicking in. Revenue nearly doubled. But what’s more impressive — margins expanded sharply as scale kicked in. EBITDA didn’t just grow; it grew five times faster than revenue. That’s not luck. That’s fixed-cost absorption working in their favour.

Section 4.5 — Pattern Interrupt

This is not just a services business.

It’s a structural dependency business.

Their clients don’t pay for code. They pay for irreplaceability.

Section 5 — Key Triggers

1.Semiconductor supercycle: Global chip demand — driven by AI, EVs, and IoT — is expanding the engineering services TAM rapidly. Every new chip design needs embedded software. This company sits at that intersection.

2.Automotive electronics ramp: The shift to software-defined vehicles is creating enormous demand for embedded R&D. This is multi-year and sticky. A client win here compounds for 5–8 years of revenue.

3.Margin expansion continuation: EBITDA margin jumped from ~4.8% to ~9.9% in one year. If revenue sustains above ₹300 Cr per quarter, margins could push toward 12–15%. That’s a re-rating story.

4.Dollar tailwind: Revenue is largely dollar-denominated. Any INR depreciation directly lifts reported revenue and margins without doing any extra work.

5.Deal visibility: Large, multi-year deals in the pipeline — if even one converts, quarterly run-rate jumps structurally. Watch order book commentary in concalls.

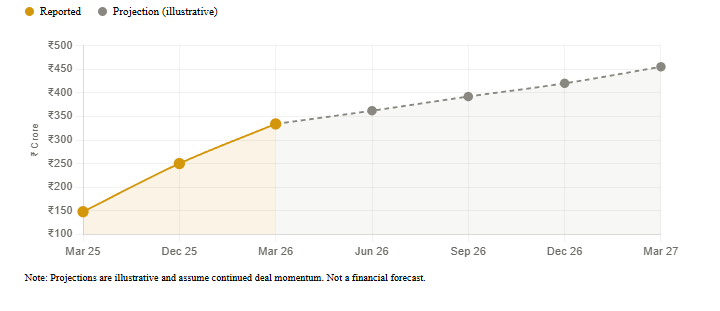

Indicative Revenue Projection — Next 4 Quarters (₹ Crore)

Note: Projections are illustrative and assume continued deal momentum. Not a financial forecast.

Section 6 — Smart Money Signal

Promoter confidencePromoter holding has remained stable — no dilution, no pledging. Skin in the game at the highest level.

Institutional interestGradual accumulation visible in institutional holdings — systematic buying, not momentum-chasing.

No retail euphoriaLow retail ownership means the re-rating potential is largely untapped. The story is early-stage in terms of market awareness.

Revenue qualityDollar-invoiced, milestone-based revenue — not lumpy project accounting. Indicates predictable, large-contract revenue recognition.

Section 7 — Risks

Client concentration: A significant chunk of revenue likely comes from a handful of global clients. Losing even one large account can materially dent quarterly numbers.

Rupee appreciation risk: Revenue is dollar-denominated. If INR strengthens sharply, reported revenue and margins compress — even if the business is doing fine.

Valuation re-rating can reverse: Once the market discovers this story, it can run ahead of fundamentals fast. Entering at peak euphoria is dangerous.

AI disruption to services: Generative AI is beginning to automate parts of embedded software development. Long-term, this could commoditise some of their offerings if they don’t evolve their value proposition.

Small float, low liquidity: This is a mid-cap. Exits can be painful if sentiment turns. The spread between intent and execution can widen fast in bad markets.

Section 8 — Final Verdict

Why should you track this?

Because 369% EBITDA growth in one year doesn’t happen by accident. Something structurally changed — either in the deal pipeline, the client mix, or the pricing power. And when something structural changes, it usually takes the market 6–12 months to fully price it in.

This is the gap. This is the window.

The business is not glamorous. There’s no viral product. No celebrity founder. No Twitter buzz. Just deeply technical work, done for global giants, in a space that is mission-critical to the next decade of technology — semiconductors, automotive intelligence, connected devices.

If the revenue run-rate sustains above ₹300 Cr per quarter and margins continue expanding, the re-rating math gets very interesting. This is the kind of business that looks obvious in hindsight — and ignored right now. That’s not a bug. That’s the opportunity.